From DTC Custody to On-Chain Collateral

DTCC is not a crypto product company. Its subsidiaries processed about $4.7 quadrillion in securities transactions in 2025 and held roughly $114 trillion in custody. July 15 sat on that base. DTC converted assets it already holds into tokenized representations ("digital twins") and pushed them through production workflows on Hyperledger Besu (DTCC's private network) and Canton (a public network). Legal ownership rights stayed the same as the traditional form. Participants could convert back.

BlackRock, Citadel Securities, J.P. Morgan, Goldman Sachs, Vanguard, BNP Paribas, CME Group, Nasdaq, NYSE, Circle, Ondo Finance, Blockdaemon, Fireblocks, Chainlink, and several dozen others ran the session. DTCC's Industry Working Group has grown past 100 members since the May update that listed 50+. The roster looks more like market infrastructure than a single-bank sandbox.

Workflows tested over several hours:

Collateral pledge and securities lending

CCP margin movements

U.S. Treasury / repo delivery-versus-payment (DvP)

Equity DvP and delivery-versus-delivery (DvD)

Equity token transfers

For DeFi readers, collateral mobility is the useful part, not another equity mint. Tokenized DTC-held Treasuries and equities that can pledge, lend, and post margin inside the regulated custody perimeter are a different animal from today's on-chain T-bill funds. Those funds already sit around $33 to $43 billion in tokenized RWA value excluding stablecoins (RWA.xyz near $33.5B in early July; Token Terminal above $43B on a wider definition). DTCC is pointing at the much larger book that never left traditional form.

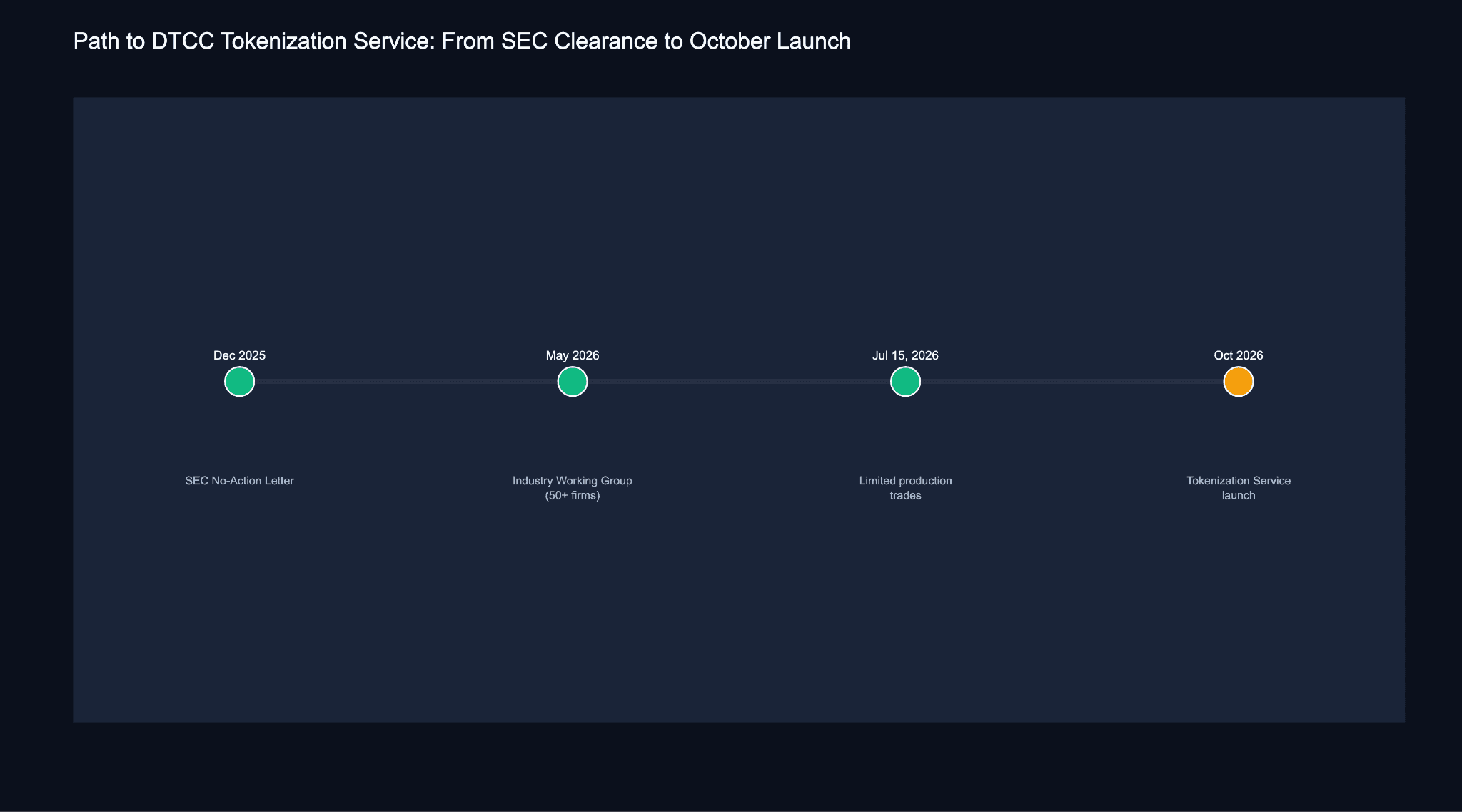

The regulatory path is already on paper. DTC got an SEC No-Action Letter in December 2025 for a defined tokenization service covering Russell 1000 constituents, major index ETFs, and U.S. Treasuries. July's limited production trades sit between that letter and the planned October 2026 commercial launch. Early coverage of the production window named Microsoft shares, Circle equity, Invesco QQQ (tokenized by J.P. Morgan from DTC holdings), State Street's SPY, and an iShares short-duration Treasury ETF. Those are a first cohort, not the full Russell 1000 floating on-chain.

DTC path to October launch

Brian Steele, DTCC's President of Clearing & Securities Services, talked about real-time collateral mobility and capital efficiency without dropping traditional investor protections. DeFi users already treat that as table stakes: if an asset can be collateral, it should not sit idle for days on settlement. Scale is still open. July 15 showed the plumbing works under institutional constraints. Whether continuous volume shows up on Besu and Canton after October is a separate question, and a harder one than getting a few hours of production trades to clear.

Asia's parallel: stablecoin cash for fund lifecycle

While DTCC worked on U.S. securities already in DTC, SBI Group, DigiFT, and Startale Group published a PoC on the cash side of a tokenized fund. On July 14 they reported two Ethereum testnet trials using a dedicated testnet token built to match JPYSC behavior. That token is not the regulated JPYSC issued in Japan. The release is careful about this: the PoC checks workflows meant for later JPYSC integration.

SBI Group and DigiFT are working toward tokenizing the SBI Japan High Dividend Equity Fund, managed by SBI Asset Management, with about ¥200 billion (~$1.3 billion) in AUM. DigiFT handles MAS- and SFC-regulated tokenization and distribution. Startale supplies chain infrastructure and the JPYSC stack (Startale and SBI launched JPYSC earlier in 2026 as Japan's first trust bank-backed yen stablecoin).

The trials covered two parts of the lifecycle. First, subscription settlement with near-instant finality instead of multi-day transfer-agent and banking cycles. Second, dividend distribution: once a payout amount and holder registry are set, smart contracts calculate and send yen-style tokens to eligible wallets. The dividend demo is structure-agnostic. The partners say it does not apply to the High Dividend Equity Fund itself. It is a cash-rail pattern for income-paying products.

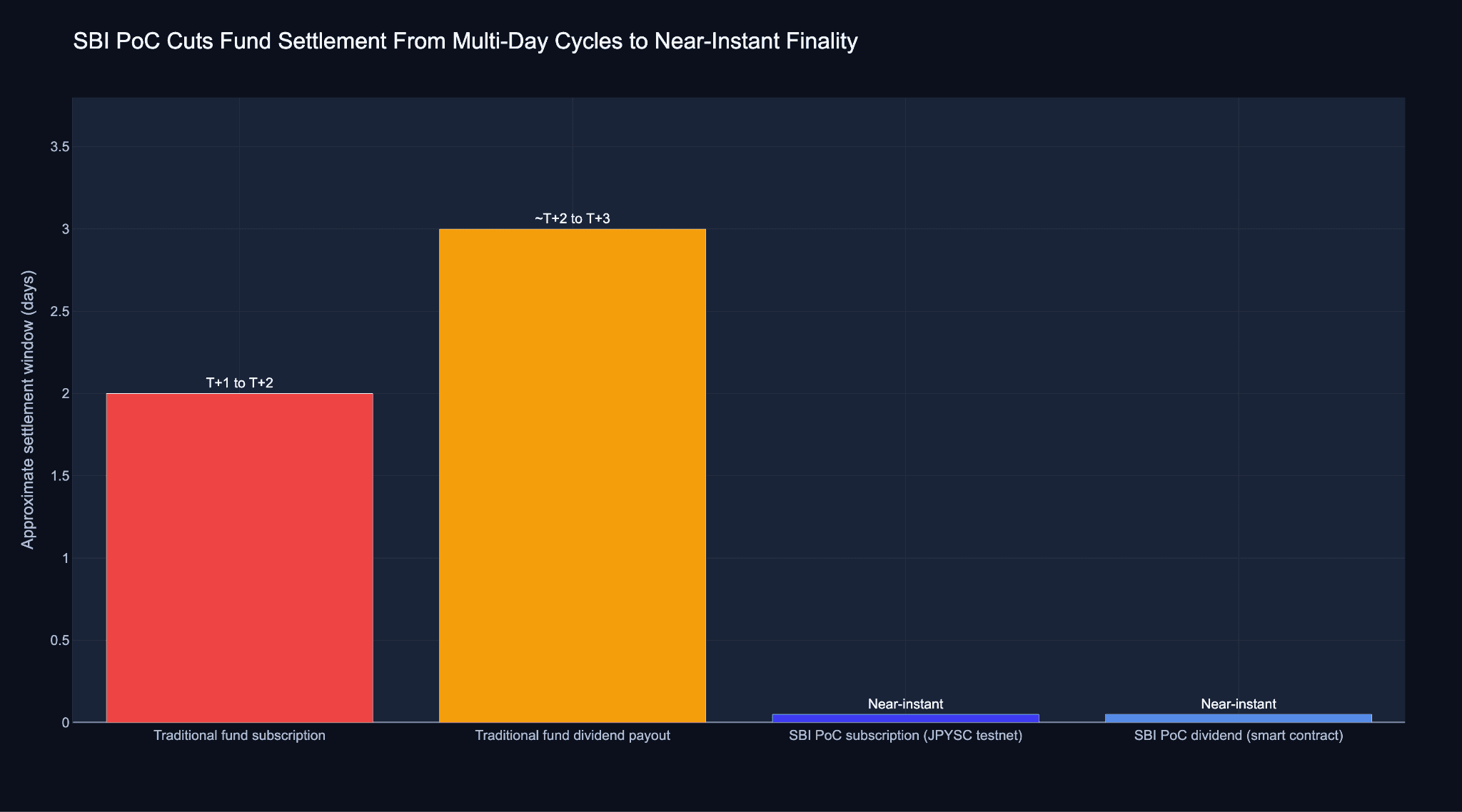

Settlement window comparison

The chart is directional. Traditional fund subscription and dividend windows often run T+1 to T+3, depending on jurisdiction and product. The PoC compresses both to near-instant finality in a test environment. On a billion-dollar equity fund, that mostly hits middle- and back-office cost: less settlement risk, less capital stuck in transit, and later the option to reinvest or convert yen cash programmatically once real JPYSC is in production.

Sota Watanabe (Startale) argued that capital markets need the full transaction lifecycle onchain, beyond minting asset tokens. DigiFT's Henry Zhang made a similar point for managers: regulated tokenization stalls if the settlement layer cannot interoperate. The three firms also say they want to test hooks into institutional DeFi venues such as Morpho and Gauntlet for lending and collateral use inside regulated wrappers. That remains a plan with no live TVL attached.

On-chain RWA value excluding stablecoins is still tiny next to DTC's $114 trillion custody book. The useful detail this week was the plumbing, not a new AUM print. DTCC is moving existing U.S. securities into token form while keeping legal protections. SBI's group is building yen cash settlement and income distribution so a tokenized fund does not have to wire dividends through ordinary banking rails.

Tokenized Treasuries and funds already compete on distribution and which venues take them as collateral. The tighter constraint now is post-trade and cash: pledge, repo, margin, subscribe, and pay income with institutional finality. July's DTCC session and the SBI PoC both target that layer. October's DTCC launch and any production JPYSC fund settlement matter more than the press headlines.