This week's issue focuses on the largest infrastructure-driven capital injection in DeFi history: Morpho's record-breaking $175 million funding round. We cover the key numbers behind the protocol's $2 billion valuation, why modular isolated lending markets have birthed a new breed of professional on-chain Risk Curators, and what this influx of traditional credit giants means for DeFi power users navigating the transition from generalized shared liquidity to specialized, risk-ringfenced yield strategies.

Morpho Secures $175M in DeFi's Largest Raise

Morpho Association secured $175 million in a token-purchase round that values the protocol at approximately $2 billion. At the time of the announcement, the MORPHO governance token traded near $1.86, translating to a circulating market capitalization of $1.20 billion and a fully diluted valuation of $1.85 billion. This marks the protocol's fourth institutional fundraise since its inception in 2021, pushing its total capital raised to over $244 million. The quantitative footprint of this funding round establishes an interesting benchmark for decentralized lending protocols.

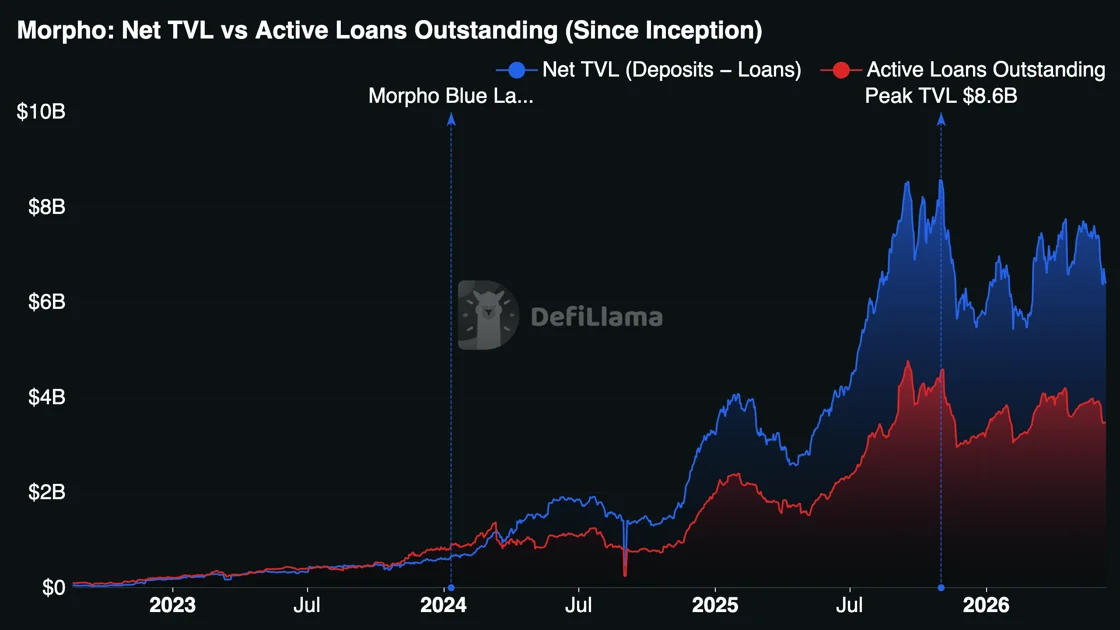

The protocol's current metrics indicate significant liquidity depth. Morpho commands $6.49 billion in total value locked (TVL) across its smart contracts, with lifetime deposits exceeding $11 billion and roughly $3.5 billion actively deployed as originated loans. These figures highlight the scale at which modern lending frameworks are operating as liquidity venues in the current market.

Valuation metrics: The $2 billion valuation reflects a premium backed by steady TVL growth and active loan origination over recent quarters.

Token dynamics: Lead investors, including a16z crypto, executed token purchases at open-market prices, signaling structural conviction in the token's long-term utility.

Supply distribution: Apollo Management's prior agreement to acquire up to 90 million MORPHO tokens over four years represents roughly 9% of the maximum supply, establishing a long-term institutional position.

The composition of the cap table includes a distinct mix of venture and institutional participants. The round was co-led by crypto-native firms Paradigm, a16z crypto, and Ribbit Capital.TradFi entities, including Apollo Funds, VanEck, SBI Group, and the French state-backed investment bank Bpifrance.

This participation from both crypto-native funds and alternative asset managers underscores an ongoing trend where traditional firms explore open-source DeFi infrastructure. Rather than relying entirely on proprietary or private permissioned ledgers, several large asset managers are testing how public blockchain rails can settle and manage credit strategies efficiently.

Source: DeFiLlama

To analyze the market positioning of this infrastructure, it is helpful to look at its specific architectural design. Traditional DeFi lending has historically relied on shared-pool designs pioneered and scaled successfully by protocols like Aave, where multiple assets are aggregated to maximize generalized capital efficiency and deep liquidity across a broad user base. Morpho Blue takes a different structural approach by focusing on a modular layer for isolated lending markets.

While isolated markets solve the contagion problem, they introduce a distinct friction point: liquidity fragmentation and complex user experiences. Expecting a retail user or a passive institutional treasurer to manually evaluate the liquidation thresholds and oracle quality of dozens of independent micro-markets is unscalable.

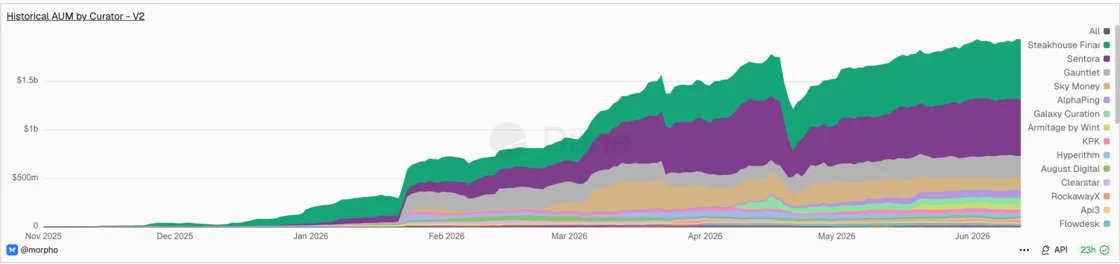

To bridge this gap, Morpho introduced the vault layer (MetaMorpho), which catalyzed an entirely new sub-sector in the decentralized credit stack: the Risk Curator.

The Curator Economy: Professional quantitative firms like Sentora, Gauntlet, Steakhouse Financial and many act as direct on-chain risk managers, protecting billions in user capital.

Incentive alignment: Curators do not work for Morpho; they are independent entities that earn performance fees on the yield the vaults generate. This strictly aligns their financial success with the safety and returns of their depositors.

Passive execution: For the end user, the experience mirrors a traditional shared pool: deposit and earn yield, while the backend benefits from active, professional oversight navigating isolated risk parameters.

Source: Dune

The ultimate distribution vector for this specialized infrastructure extends far beyond crypto-native yield farming. Apollo Management's agreement to acquire up to 9% of the MORPHO token supply signals that traditional asset managers intend to use public blockchain rails to settle real-world credit strategies.

When traditional finance firms tokenize RWAs such as Treasury bills, corporate debt, or structured insurance products, these instruments carry unique liquidity profiles and legal encumbrances. They cannot be safely aggregated into shared retail liquidity pools without introducing massive systemic risk. Modular, isolated markets managed by specialized institutional curators provide the exact ring-fenced environment these entities require to borrow against or lend out fiat-backed instruments.

Currently, protocols are fiercely competing to become the definitive backend plumbing for B2B integrations. Centralized exchanges and digital asset custodians are actively evaluating diverse lending infrastructures to power their client offerings. Coinbase, for example, has utilized Morpho's smart contracts to successfully originate over $2.17 billion in corporate USDC loans, while firms like Kraken and Bitwise are similarly integrating various DeFi protocols to construct non-custodial yield products.

The Admin Key Problem: When Governance Is the Vulnerability

For our weekly risk section, we're taking a closer look at the problem admin key management poses to security. For most of its history, DeFi treated the audit report as the primary safety signal. That framing misses a second, equally material risk layer. The Humanity Protocol incident on June 8-9 is a clear illustration. Auditors had reviewed the contracts. The code did exactly what it was supposed to do. The $36 million was lost not because anyone found a bug, but because an employee's laptop held backups of seven Gnosis Safe owner keys, a malware infection gave the attacker root access to that machine, and three compromised keys were enough to reach quorum on both the Ethereum and BNB Chain bridge multisigs simultaneously.

The attack proceeded in three stages. First, 6 million H tokens were drained from an Ethereum admin hot wallet whose key was on the same device. The attacker then used three of the six Ethereum Safe owner keys to seize ProxyAdmin ownership of the bridge contract, upgraded it to a malicious implementation, and cleared 141 million H in a single transaction. On BNB Chain, three of five compromised keys gave the attacker control of that ProxyAdmin as well, and three sequential mint transactions expanded the circulating supply from 141 million to 441 million H before the tokens were liquidated through decentralised exchanges. The protocol paused bridge activity after the fact.

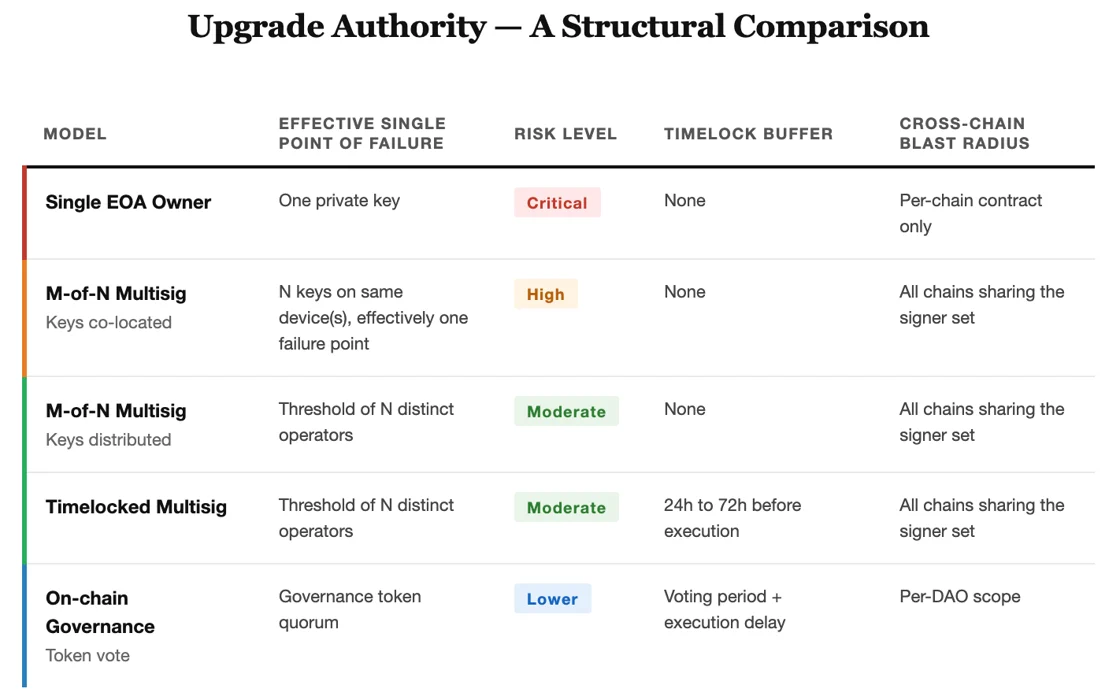

The underlying mechanic is not unique to Humanity. Most upgradeable protocols follow the same pattern: a Transparent or UUPS proxy points at an implementation contract, a ProxyAdmin owns the upgrade function, and a multisig owns the ProxyAdmin. That chain of authority is the protocol's actual governance perimeter. A successful attack on the ProxyAdmin owner produces arbitrary code execution: the attacker can replace the implementation with anything, including a contract that sends all funds to a specified address or enables unlimited minting. Whether the original implementation is formally verified is irrelevant at that point.

Allocators should evaluate governance infrastructure alongside smart contract risk, not instead of it. The practical checklist: does the protocol use an upgradeable proxy, and who owns the upgrade path; what is the multisig threshold and are the keys held by genuinely distinct entities with independent infrastructure; is there a timelock between a governance action and its execution, and is it long enough for users to exit; which chains share the same signer set, and what is the blast radius if threshold is reached. For cross-chain protocols, treat changes to multisig composition, key holder identity, or timelock duration as re-underwriting events. A distribution that looks secure at setup can collapse to a single point of failure if a key backup ends up on the wrong machine.