The Setup Nobody Saw Coming

On May 27, 2026, the Depository Trust & Clearing Corporation (DTCC), the post-trade infrastructure company that clears and settles virtually every U.S. securities transaction, announced it will bring DTC-custodied assets onto the Stellar network. Russell 1000 stocks, Major ETFs, U.S. Treasuries by first half of 2027.

To most of crypto, it came out of nowhere. To anyone tracking Stellar's institutional track record for the past five years, it read less like a headline and more like a confirmation. Stellar has been quietly doing the unglamorous work of institutional financial infrastructure since 2015. While the rest of DeFi was launching governance tokens and liquidity mining programs, Stellar was building cross-border payment corridors in Southeast Asia, partnering with MoneyGram, and hosting the world's first U.S.-registered tokenized money market fund. None of it was trending on X. All of it was compounding.

This is the story of how that compounding becomes quantifiable.

What Is Stellar, and Why Is It Different?

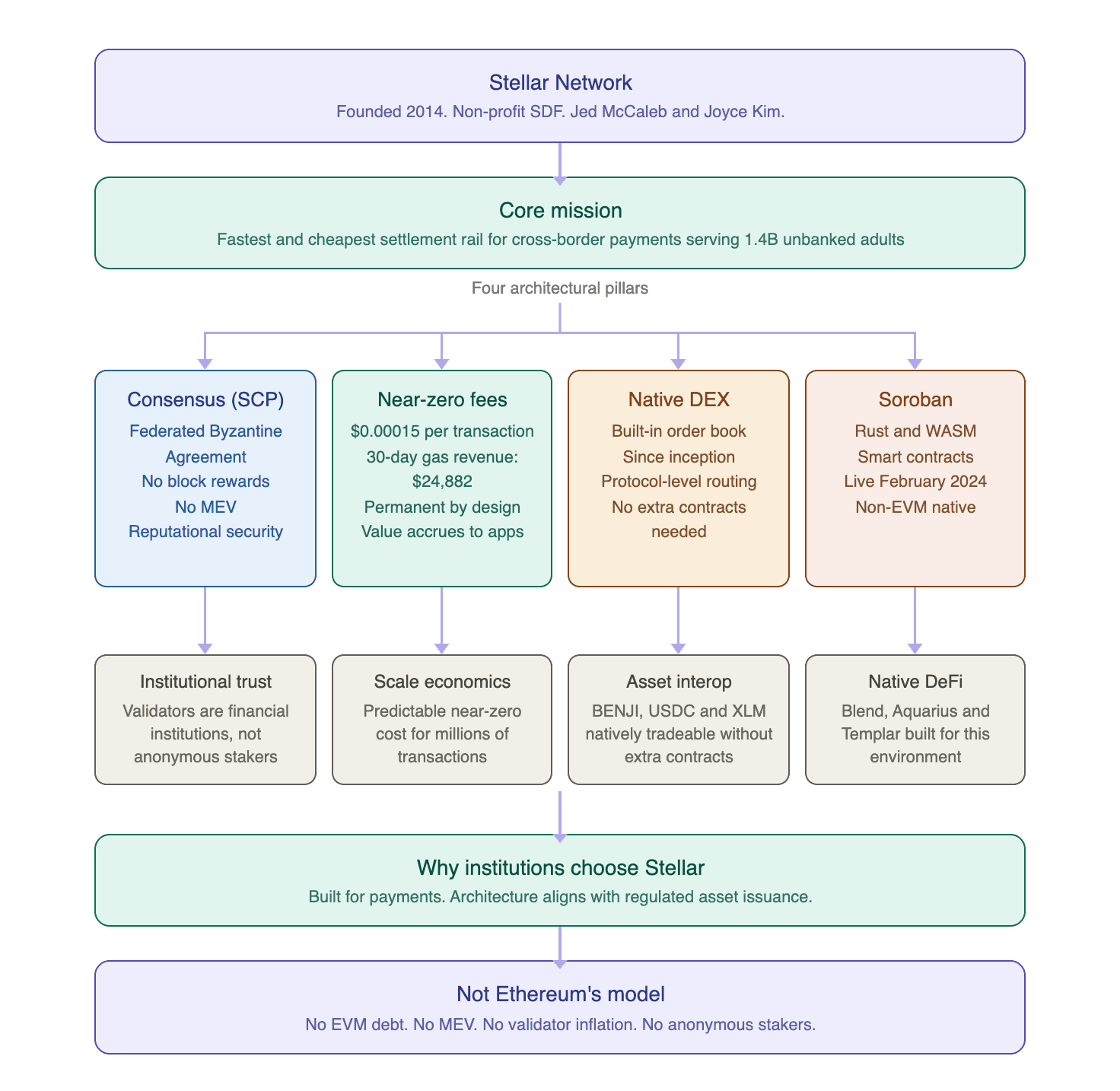

Stellar was founded in 2014 by Jed McCaleband Joyce Kim, governed by the non-profit Stellar Development Foundation. Its design brief was deliberately narrow: build the fastest, cheapest, and most interoperable settlement rail for cross-border money movement. A payment network built for the 1.4 billion adults who still have no bank account and no reliable way to move money across borders.

That brief produced an architecture that looks nothing like Ethereum or its descendants, across four dimensions that matter for understanding why institutions chose it.

Consensus without economic incentives: Stellar runs the Stellar Consensus Protocol (SCP), a form of Federated Byzantine Agreement. Validators, which include financial institutions, exchanges, and the SDF, reach consensus through overlapping quorum sets rather than staked capital. There is no block reward, no validator inflation, no MEV. Validators run the network because they have institutional interest in its reliability. This is a reputational-and-relational security model with different failure modes than proof-of-stake. For a regulated financial institution evaluating which blockchain to use for a securities product, "our validator set is composed of other financial institutions" is a materially different pitch than "our validators are anonymous stakers chasing yield."

Fees built for throughput: The average Stellar transaction costs $0.00015. The entire chain's 30-day gas revenue totalled $24,882, a number that fits inside a single busy Ethereum block. This is not a temporary subsidy; it is permanent by design. The base layer earns nothing. Value accrues to applications. When you are processing remittances for unbanked populations or clearing institutional securities at scale, fee predictability at near-zero cost is a product requirement, not a nice-to-have.

A native DEX baked into the protocol: Stellar has had a built-in central limit order book since inception, before "DeFi" was even coined. Every asset issued on Stellar can be traded against any other asset through path payment routing at the protocol level. This is not a bolted-on AMM; it is infrastructure. When Franklin Templeton issues BENJI tokens on Stellar, those tokens are natively tradable against USDC, XLM, or any other Stellar asset without deploying a single additional smart contract.

Soroban: programmability without EVM debt. For its first decade, Stellar had no general-purpose smart contract layer. That changed in February 2024 with Soroban, a Rust/WebAssembly smart contract environment designed from scratch. Soroban is not EVM-compatible, which means zero portability from Ethereum's existing protocol codebase, but also zero inheritance of EVM's well-documented attack surface and technical debt. Blend, Templar, Aquarius and all the DeFi infrastructure appearing on Stellar in 2025 and 2026 are native Soroban applications built specifically for this environment.

These choices were built for payments. It turns out they also happen to be exactly what institutional asset issuers need.

Why Now? Five Years of Compounding

For most of its first decade, Stellar's value proposition was straightforward: cheap, fast payments. In 2025, payment volume reached $55.6B, up 52% year over year. By Q1 2026, quarterly stablecoin payment volume had hit a record $5.5B, while onchain RWAs crossed $2B. Monthly transfer activity surged 30x in early 2026 . Latin America drove the majority of it: over $730B in crypto moved across the region in 2025 (+60% YoY), much of it through Stellar payment corridors serving practical demand for stable value and FX access .

But the inflection point was not payments. It was tokenization.

When Franklin Templeton launched BENJI, the first U.S.-registered tokenized money market fund, on Stellar in 2021, most of DeFi ignored it. Four years later, BENJI has expanded to 8 blockchains and has a market cap of $741.45M. The number that matters: ~68% of the fund's entire user base, are still on Stellar . The chain did not just incubate the world's first tokenized MMF; it retained its holder base through every competing chain's emergence. That kind of stickiness is not replicated anywhere else. Network effects alone do not explain it. The real explanation is the product experience of a near-zero-cost, near-instant settlement environment that regulated issuers can actually control.

Spiko then built the deepest multi-currency RWA stack on any public blockchain. Ondo added yield-bearing dollar instruments. WisdomTree, Etherfuse, and Mercado Bitcoin followed. By the time DTCC made its announcement yesterday, Stellar was not pitching for institutional business. It was demonstrating a five-year track record of executing it.

Chain Fundamentals: The Data Underneath the Narrative

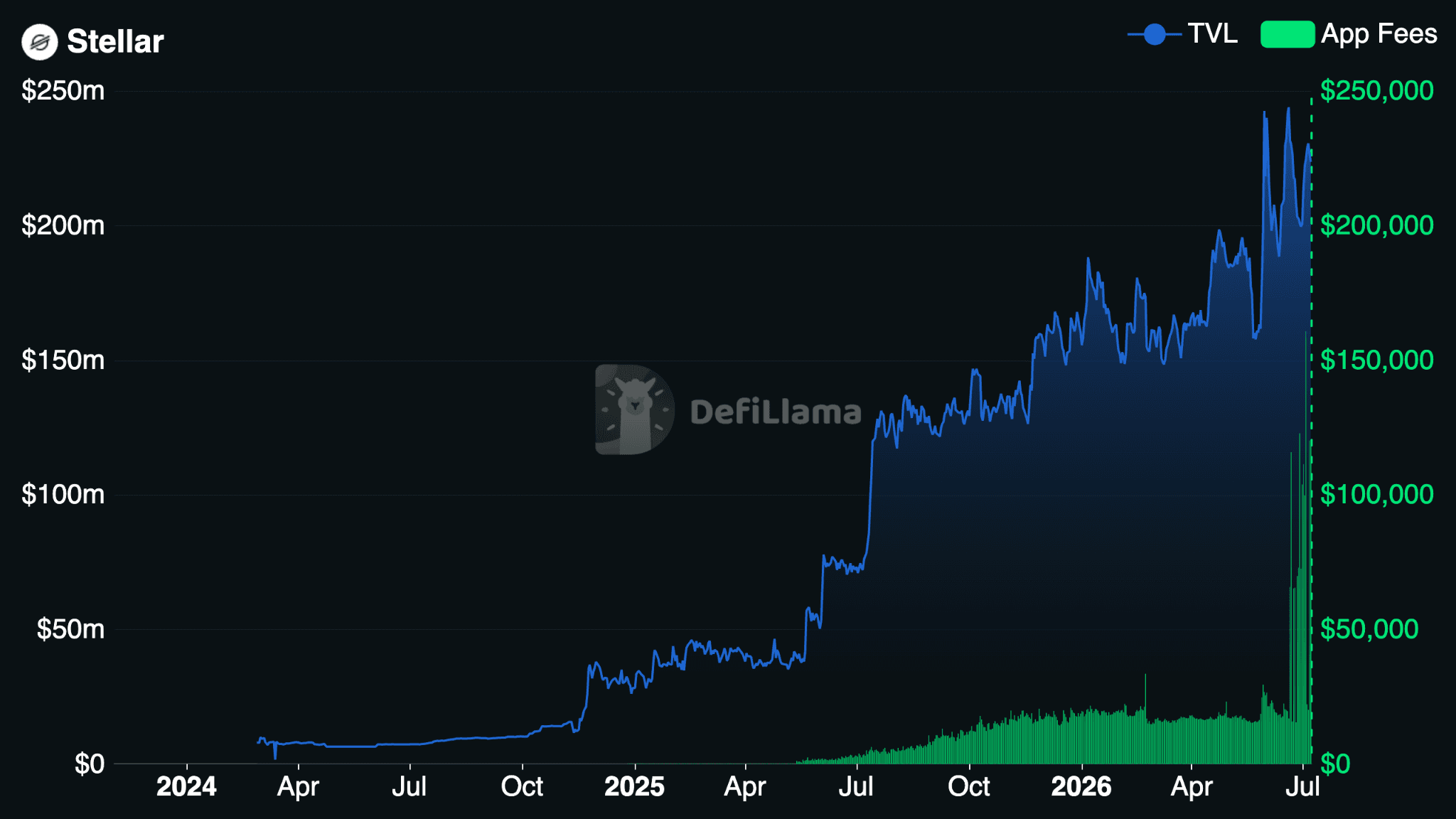

Source: DefiLlama

Stellar’s DeFi TVL reached a new all-time high on the 18th of June, 2026, surpassing $240 million.. The DTCC announcement on May 27 catalysed a +27.5% move in seven days and a +9.2% gain over 30 days, reversing what was a brief consolidation phase. The 90-day trend sits at +35.8%, and the year-over-year figure is +214.1%. Beneath the headline DeFi TVL, a much larger on-chain economy has assembled:

Tokenized RWA active market cap (ex-stablecoins): $2.92B across 13 assets

Stablecoin circulating supply: $842.8M across five currency pegs (USYC dominance with 62.3%)

Combined on-chain value: approximately $3.77B, over 16× the raw DeFi TVL figure

App-level protocol fees for the past 30 days totalled $546,269, annualizing to $6.56M. DEX volume over 30 days reached $75.0M, with a single-day spike to $6.75M on June 15, roughly 2.7× the 30-day daily average of $2.50M

The above chart tells a clean structural story: TVL was essentially flat through early 2026 in a post-ATH consolidation phase, broke decisively upward in the final week of May as institutional narrative catalysts compounded into on-chain capital flows, and set a new ATH on 18th of June.

The $2.92B RWA Stack: Primary Issuance, Not Wrappers

Source: RWA.xyz

The RWA layer is where Stellar's institutional moat becomes fully quantifiable. $2.92B in active tokenized real-world asset market cap sits on-chain across dozens of instruments. These are primary-issued, regulated products from licensed financial entities. Not ERC-20 wrappers of off-chain assets, not DeFi-native yield tokens, but actual securities and investment products whose on-chain representation is the canonical record. The ecosystem concentrates around two dominant issuers.

Spiko: $1.214B (36.3% share). The Paris-based regulated investment platform has built the most comprehensive multi-currency RWA stack on any public blockchain. Its Stellar positions include EUTBL (EU Treasury Bills, $506.8M, the second-largest single RWA on Stellar after BENJI), eurSAFO (EUR short-duration bonds, $538.0M, now the largest single Spiko position, ahead of EUTBL), SAFO (USD equivalent, $71.9M), USTBL (U.S. T-Bills, $49.1M), plus UK T-Bills ($18.6M) and Cash & Carry instruments (about $2.4M combined). Six products, four currencies, one primary chain.

Franklin Templeton: $603.6M (18.3% share). BENJI holds $515.8M active on Stellar as of today. Beyond BENJI, Franklin has deployed the first tokenized UCITS fund in Luxembourg (2024, on Stellar) and the first retail tokenized fund in Singapore (2025, on Stellar). Stellar is not a strategic side deployment for Franklin. It is their primary tokenization infrastructure across retail, institutional, and international channels.

The quarterly growth trajectory remains notable. Q4 2025 ended at $796M. Q1 2026 ended at $1.52B, a +91.4% QoQ jump. Q2 2026 closed at $2.92B, a continuation of the strong growth with ~86%.. The institutional pipeline behind this is unusually named: U.S. Bank, Amundi, Société Générale, AllUnity, and Malaysia's Kenanga Investment Bank all advanced activity in Q1. Mercado Bitcoin committed to a $200M RWA issuance program covering Latin American fixed income and equities in September 2025.

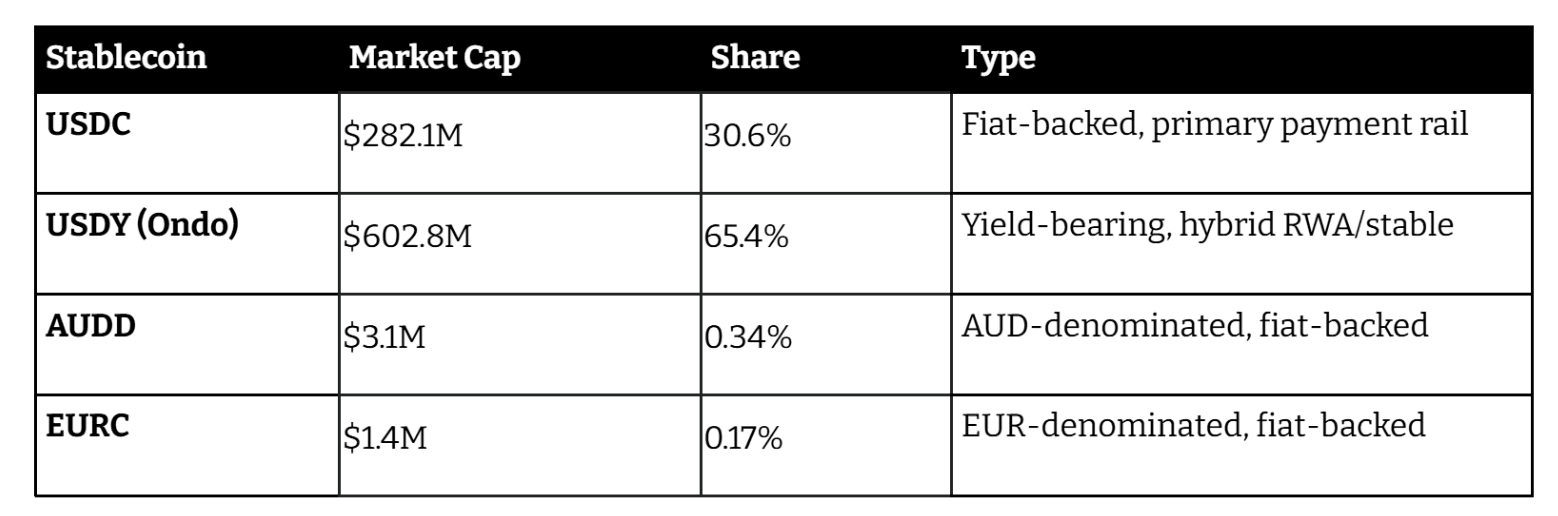

Stablecoin Infrastructure: The Settlement Substrate

Stellar's $842.5M stablecoin base provides the settlement layer that both the RWA stack and native DeFi depend on:

Source: DefiLlama

The 97.4% USD concentration maps directly to LATAM payment demand. In Q1 2025, $3.4B in RWA payment volume ran through the network; full-year 2024 was $32B total. The USDY position ($124.4M) is structurally meaningful: a large portion of Stellar's stablecoin float is yield-generating by default. Passive holders earn Treasury returns without taking additional DeFi risk. No other chain of comparable size has this property at this scale.

Native DeFi: Where the Institutional Base Gets Activated

A tokenized Treasury bill sitting in a wallet earns its off-chain yield. That same asset posted as collateral in a lending protocol earns its off-chain yield and unlocks on-chain liquidity at the same time. The entire Stellar DeFi thesis rests on closing that gap, and the evidence from the past 12 months is that it is closing.

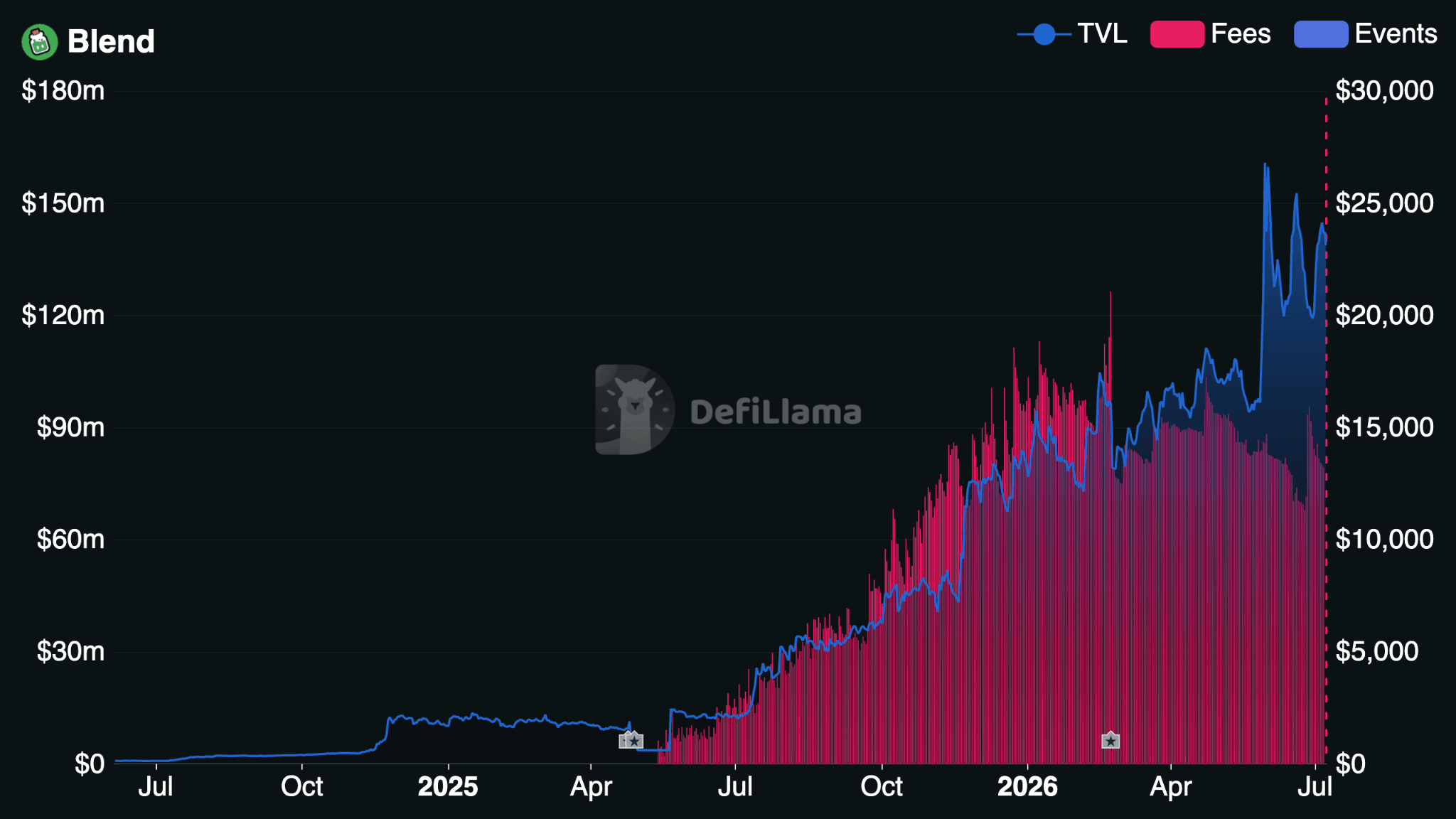

Blend is the primary engine. Launched June 5, 2024 on Soroban with $868K in TVL, it holds $138.7M today, a +15,871% growth from inception, with +14.9% in the past seven days. Over the past 30 days, Blend generated $396,632 in fees ($13,222 in the past 24 hours alone as TVL accelerated), annualizing to $4.76M, all of which flows to lenders by design with zero protocol revenue extraction. Blend's isolated pool architecture was stress-tested in February 2026 when YieldBlox, a separate Stellar-based lending protocol, suffered a $10.2M oracle manipulation exploit. Blend was unaffected. The $7.2M recovery via validator freeze demonstrated how SCP's institutional validator set can act as an emergency backstop that no permissionless chain could replicate.

Source: DefiLlama

Templar launched lending and borrowing markets for six freely transferable RWA assets on April 1, 2026, including Centrifuge and Etherfuse instruments. It has grown to $22.99M TVL (+7.5% in the past seven days). For the first time, holders of EUTBL or SAFO can post those positions as on-chain collateral and borrow stablecoins against them. The composability loop that has existed in theory since 2022 is now partially live in production.

Aquarius ($45.37M TVL, $141,694 in 30-day fees, $99,251 in 30-day protocol revenue) provides the AMM infrastructure for USDC, USDY, XLM, and RWA token pairs. Alongside the native Stellar DEX ($14.67M TVL) and Stellar AMM ($8.86M TVL), the chain's full DEX layer holds $68.9M in TVL and handled $75.0M in volume over the past 30 days, with $6.75M transacting on June 15 alone. As the RWA base deepens and more assets become freely transferable, these pools are the natural venue for secondary market price discovery.

The Next Stage

Stellar's story is the slowest-burning compound trade in crypto. A decade of payments infrastructure and quiet institutional relationship-building, culminating in the world's first tokenized money market fund, built up while the market chased liquidity mining and meme coins.

The next test is activation: can the $2B+ in RWA capital on Stellar become a functioning capital market of collateralized lending, yield-bearing settlement, and composable rate discovery? Sentora is now part of that answer. We’re collaborating with the Stellar Development Foundation and Stellar DeFi Hub to launch a first generation of Stellar-native vaults, built on Aquarius' liquidity infrastructure and backed by the same curation and risk framework behind our vault ecosystem. The initial vault is now open for XLM, with USDC, and PYUSD deposits anf active strategies across Blend, Templar, and Aquarius to follow in the near future.

This new vault infrastructure could become one of the most important pieces of Stellar ecosystem’s path toward productive capital. You can access the vaults here: https://stellardefihub.com/vaults

Not financial advice. DeFi positions carry smart contract, liquidity, issuer credit, and regulatory risk. RWA tokenization is subject to redemption policy changes, issuer credit risk, and custodian risk. Past TVL growth does not guarantee future performance.