SoFi Technologies launched SoFiUSD on May 27, making it available to all 14.7 million members inside the SoFi banking app. The product is redeemable 1:1 for dollars from SoFi Bank, backed by cash held at the Federal Reserve, and verified through regular CPA attestations. It runs on Ethereum and Solana at launch, with additional networks planned. SoFi first launched SoFiUSD in December 2025 for enterprise clients, but this week's rollout is the consumer phase.

The "first U.S. national bank" framing holds up under scrutiny. JPMorgan's JPM Coin is a private, permissioned token restricted to institutional clients. Societe Generale's euro-pegged stablecoin is issued by a French bank. SoFiUSD is the first stablecoin issued by an OCC-chartered insured depository institution and made available inside a consumer banking interface on a public, permissionless blockchain.

The Mastercard and Galileo Angles

The consumer launch is one layer of a larger distribution story. In March 2026, SoFi extended its Mastercard partnership to allow SoFiUSD to function as a settlement currency across Mastercard's global payments network. Under that agreement, SoFi Bank will settle its own credit and debit card transactions in SoFiUSD. More significant for scale: Galileo, SoFi's B2B technology platform with over 160 million accounts, is expected to offer other issuing banks the option to settle card transactions using SoFiUSD. That would put the stablecoin inside the rails of banks and fintechs that have no SoFi relationship with end consumers.

SoFiUSD vs. USDC and USDT

SoFi's positioning against crypto-native issuers rests on regulatory standing: a nationally chartered bank, FDIC-insured deposits (on the bank side), OCC oversight, and 1:1 cash reserves rather than mixed reserve baskets. "SoFiUSD competes by offering what crypto-native issuers cannot: the trust, security and oversight that comes with being a nationally chartered bank," SoFi said in its announcement. USDT and USDC dwarf SoFiUSD in market cap and DeFi liquidity by orders of magnitude; the bet is that regulated institutions will prefer a bank-issued token over crypto-native ones.

The near-term roadmap includes tokenized deposits convertible to FDIC-insured accounts, 24/7 cross-border transfers, and a listing on Bullish for institutional trading. Full consumer rollout is expected by early June as members update the app.

Not financial advice. DeFi and digital asset markets involve significant risk.

Wrapped Bitcoin: Beyond the Single-Wrapper Era

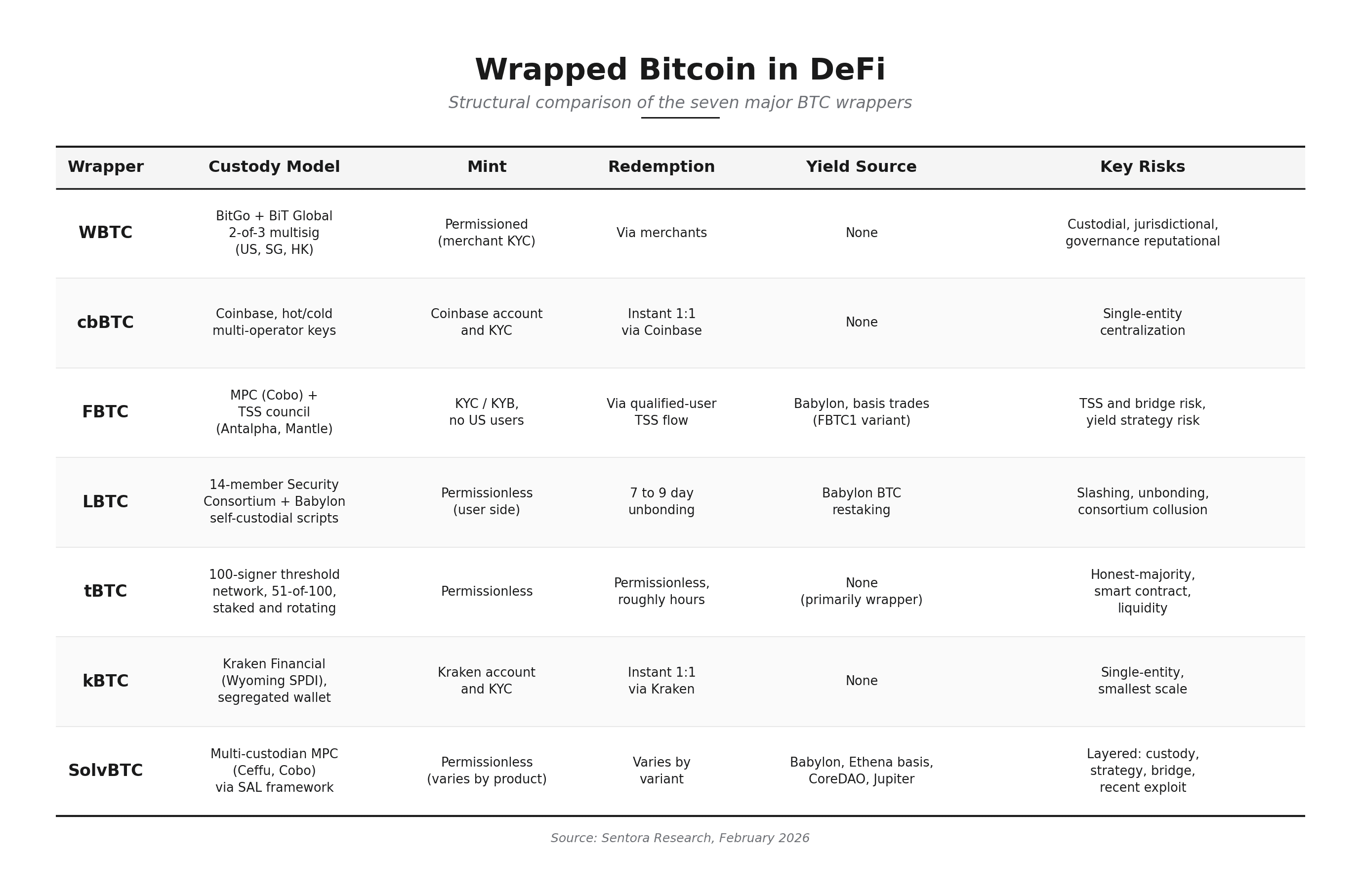

For five years, holding Bitcoin in DeFi meant holding WBTC. That has changed. The wrapped BTC market has fragmented into a competitive set of custodial tokens, exchange-issued wrappers, decentralized threshold-signature bridges, and yield-bearing liquid-staking derivatives. WBTC remains the largest by supply, but its dominance has eroded as governance concerns around its 2024 custody restructuring pushed allocators toward alternatives. The deeper point is that not every wrapper is built the same way, and the mechanics determine the risks.

The dominant new trend is centralized exchanges issuing their own wrappers. Coinbase's cbBTC scaled to roughly $6B by mid-2026, growing 160% over 2025. Kraken followed with kBTC. Mechanically these wrappers are simple. A user deposits BTC into their exchange account and receives a 1:1 wrapped token on Ethereum, Base, or Solana. Redemption reverses the flow instantly through the exchange. There is no merchant layer, no signing consortium, no on-chain logic beyond a basic mint and burn contract. The risk surface concentrates entirely in a single regulated entity. The trade-off is direct: simplicity, deep liquidity, and tight exchange integration in exchange for full counterparty exposure to one custodian.

Other wrappers distribute that custodian role. FBTC uses a multi-party MPC custody model with a TSS signing council across Antalpha, Cobo, and Mantle, gated by KYC/KYB and closed to US users. tBTC removes custodians entirely. Each tBTC wallet is secured by 100 randomly selected, staked, slashable signers, with any 51 of 100 able to authorize a Bitcoin transaction. No single party ever holds the full private key, and wallets rotate roughly every two weeks. Mint and redemption are permissionless. The trade-off is smaller liquidity (around $0.5B) and an honest-majority assumption that the signer set will not collude.

LBTC and SolvBTC introduce a different category: yield-bearing tokens backed by active strategies. LBTC stakes BTC through Babylon, which uses self-custodial Taproot scripts and Bitcoin-native slashing. Redemption is gated by a 7 to 9 day unbonding queue. A 14-member institutional consortium handles signing. SolvBTC aggregates multiple yield sources through its Staking Abstraction Layer, with variants targeting Babylon restaking, Ethena's delta-neutral basis trade, CoreDAO validator delegation, and Jupiter's JLP pool. Each variant carries its own strategy risk, slashing exposure, or basis-trade unwind risk. A March 2026 exploit drained roughly $2.7M from a SolvBTC product vault, illustrating how the structured-yield layer expands the attack surface beyond a simple wrap.

Wrapped BTC is no longer a single asset class. A pure wrapper's worst case is custodian failure. A distributed-signer wrapper adds collusion and bridge risk. A liquid-staked wrapper adds slashing and a multi-day unbonding queue. A strategy-backed wrapper adds market and execution risk on top of that. Users should classify each token before allocating, match the wrapper to the use case, and treat changes in custody, governance, or proof-of-reserves as re-underwriting events. The choice of which BTC to hold in DeFi now matters as much as the choice of which protocol to deploy it in.