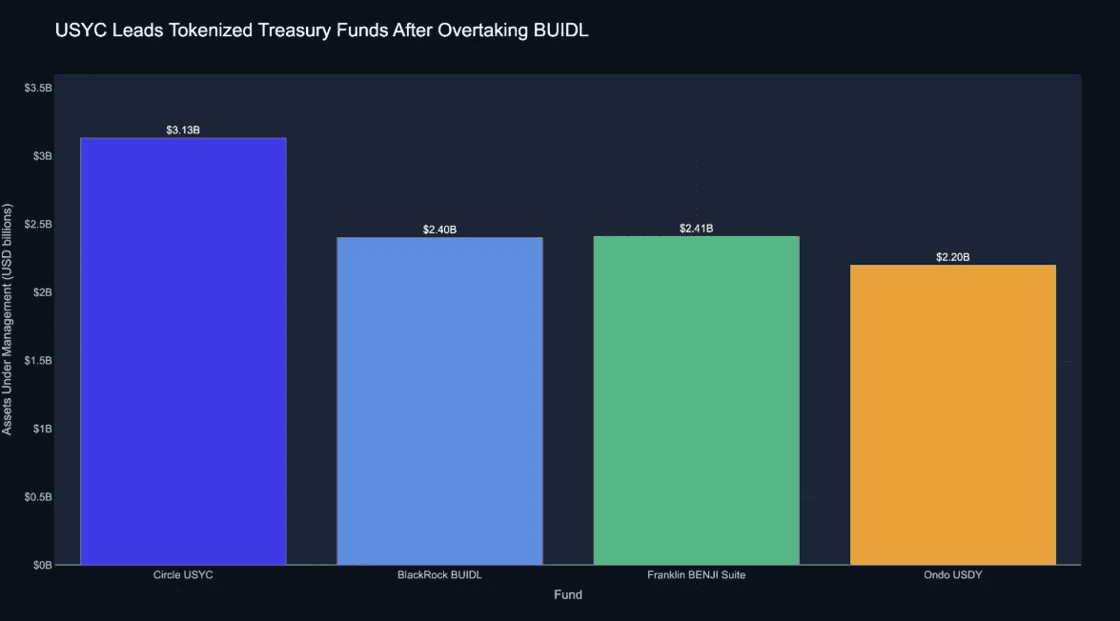

Per RWA.xyz data as of June 25, Circle USYC holds about $3.13 billion in assets, the largest single tokenized U.S. Treasury product. BlackRock's BUIDL is at $2.40 billion. The combined Franklin Templeton BENJI suite (iBENJI + BENJI) is roughly $2.41 billion across nine blockchains. USYC leads BUIDL by about $730 million. When BUIDL launched in March 2024 and quickly became the category benchmark, that gap would have been hard to picture.

This is not mainly a product-quality story. USYC and BUIDL both hold short-duration U.S. government exposure, run through institutional custody, and print 7-day APYs in the 3.1% to 3.4% range. The split is distribution and collateral plumbing. USYC picked up speed after Binance listed it as off-exchange collateral for institutional derivatives on BNB Chain. RWA.xyz shows roughly 86% of USYC supply sitting there now. BUIDL was built for qualified purchasers with a $5 million minimum subscription and daily wire settlement through Securitize. That fits balance-sheet buyers. It is a worse fit for fast collateral rotation.

CryptoSlate and TokenPost both describe the flip as net creations into USYC while BUIDL saw net redemptions over similar windows, not a sudden loss of faith in BlackRock's fund. BUIDL is still on eight networks (Ethereum, Solana, Avalanche, Aptos, BNB Chain, Optimism, Arbitrum, Polygon). USYC's weight on BNB Chain collateral rails is a use case BUIDL has not matched at the same scale. Franklin's BENJI suite plays a third game: a registered 1940 Act fund, retail access, and nine chains (Stellar, Ethereum, Arbitrum, Base, Solana, BNB Chain, and others).

Franklin Templeton has treated chain breadth as a liquidity bet, not a checkbox. Its April 2026 release put BENJI suite AUM at $1.98 billion as of April 29, with investor count up more than 140% since April 2024 and cumulative P2P transfer volume above $211 million. RWA.xyz's combined figure near $2.41 billion points to continued inflows even as BUIDL's 30-day supply fell about 3.4%. Tokenized Treasuries are no longer a one-issuer market. Liquidity now splits by issuer, chain, eligibility tier, and whether a venue will take the token as margin.

Tokenized U.S. Treasuries on public chains total about $15 billion, per 21shares' mid-year report, with average 7-day yields near 3.35%. The composability piece matters: the same exposure can sit in lending, perps, or structured yield without waiting for banking hours. Aave, Pendle, and similar venues have started treating on-chain T-bills as productive collateral rather than idle cash equivalents.

On June 25, Antier rolled its RWA tokenization work into one delivery model: legal structuring, platform engineering, token launch, and post-launch support under a single vendor. Circle, BlackRock, and Franklin Templeton are competing on distribution. The vendor layer below them is moving from stitched-together multi-party builds toward full-stack deployment for real estate, gold, private credit, and fund tokenization. One accountable team does not remove smart-contract or compliance risk. It does cut coordination drag, which has been one of the main reasons RWA pilots stall.

Institutional Resilience

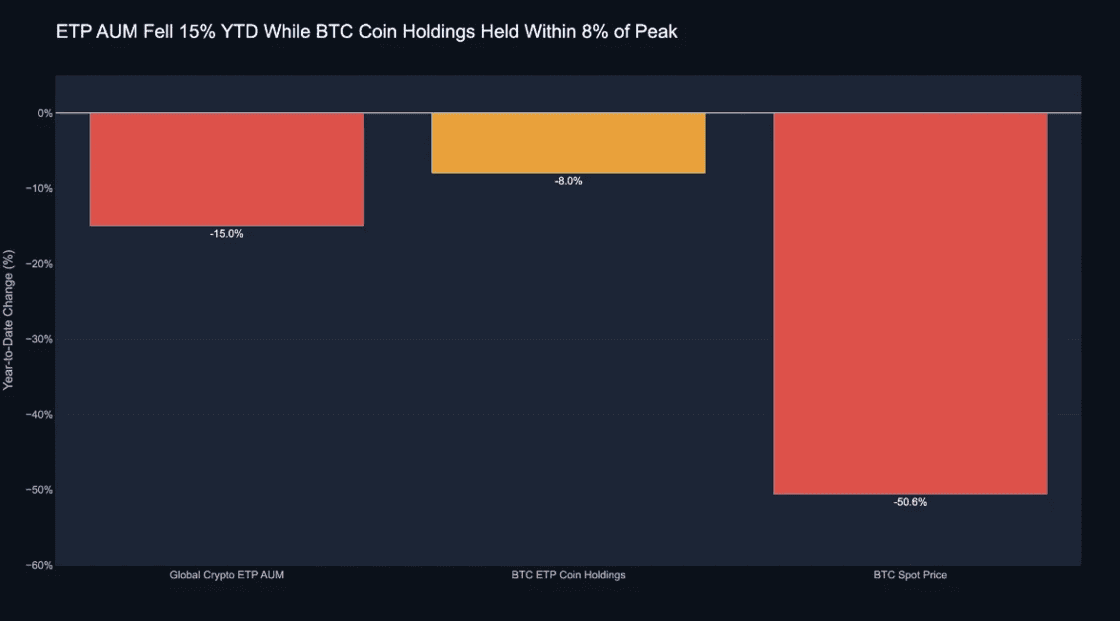

Tokenized yield kept scaling while spot crypto stayed under pressure. Institutional exposure through regulated wrappers has held up better than headline AUM would suggest. On June 24, 21shares published its State of Crypto 2026: Mid-Year Update, checking ten December 2025 forecasts against six months of data. Global crypto ETP AUM is $140 billion, down about 15% year-to-date. Net underlying BTC holdings in ETP structures are 1.25 million coins, within 8% of all-time highs.

USD AUM and coin-denominated holdings are telling different stories. Bitcoin peaked near $126,000 in October 2025 and traded around $62,300 in the report, a drawdown of about 50% from peak. If ETP AUM moved only with price, the dollar figure would have fallen in line with spot. Coin holdings are down only about 8% from peak. Most of the AUM drop looks mark-to-market, not mass liquidation. Adrian Fritz, 21shares' Chief Investment Strategist, put it plainly: "Allocators are holding through volatility."

A few numbers worth keeping:

BTC ETPs account for roughly $110 billion of the $140 billion global complex, per coverage of the report. Bitcoin wrappers are still the main institutional on-ramp.

U.S. spot BTC ETFs have seen about $3 billion in net outflows year-to-date, yet BTC-denominated holdings stay near record levels. That reads more like tactical USD trimming than a structural exit.

The current drawdown is milder than the 80%+ corrections of prior cycles. Bitcoin has held above an aggregate investor cost basis near $54,000.

Hyperliquid ETFs in the U.S. raised $150 million in their opening month, a sign that allocators will still buy new wrappers when the underlying has verifiable on-chain revenue.

The May-June ETF outflow streak was real and it moved spot liquidity. The 21shares audit still suggests the stock of institutional BTC exposure has not unwound in proportion to price. Daily flow prints are marginal USD activity. Coin-denominated holdings are the stock. With 1.25 million BTC in ETP structures, there is a large base of capital that does not need to sell into every dip. That does not mean flows have turned positive. It means the holder base has not reset the way spot prices have. 21shares keeps a $100,000 year-end base case for Bitcoin, tied to post-halving rhythm and structural maturity. That is a forecast, not a promise.

Tokenized Treasury products are scaling and competing on where they plug into collateral and chain liquidity. ETP capital, measured in coins rather than mark-to-market dollars, has been stickier than spot prices imply. USYC passing BUIDL is a reminder that collateral integration and chain-level liquidity can beat issuer brand. 1.25 million BTC in ETP wrappers, within 8% of peak, fits allocators treating the drawdown as cyclical. For DeFi users, the practical tilt is toward yield-bearing collateral and hedged structures, not naked directional beta. NFA. Tokenized Treasury products carry issuer, custody, smart-contract, bridge, eligibility, and redemption-timing risk. ETP holdings data is a snapshot. Flows can turn if macro conditions worsen.

Disclaimer: The information provided in this newsletter is for educational and informational purposes only and does not constitute financial, investment, or legal advice.