Stripe-backed Tempo integrates Morpho lending

This week’s key institutional DeFi story is Tempo integrating Morpho’s lending infrastructure. Tempo, the stablecoin-focused blockchain backed by Stripe and Paradigm, is adding access to Morpho’s roughly $7.5B DeFi lending marketplace, turning a payments-focused network into something closer to an onchain treasury and credit layer.

The core idea is simple: stablecoin payments create balances, and those balances do not always need to sit idle. With Morpho integrated, fintechs and enterprises building on Tempo can potentially lend, borrow, and earn yield on stablecoin balances without leaving the same ecosystem.

This matters because institutional stablecoin adoption is moving beyond basic transfers. Enterprises care about payments, but they also care about cash management, collateral efficiency, working capital, and yield on idle liquidity. Tempo brings the payments rail; Morpho brings the lending market.

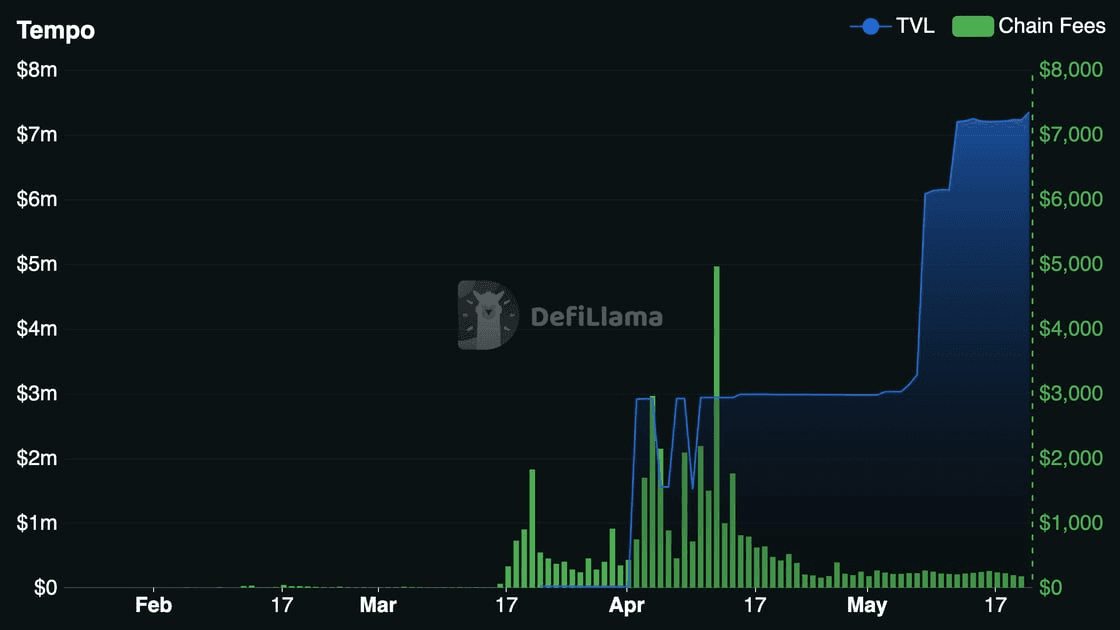

Source: DeFiLlama

The integration also includes curated markets from risk firms such as Sentora and Gauntlet, with RedStone expected to provide oracle infrastructure. That is important because institutional users usually do not want completely unmanaged DeFi exposure. They need clearer risk parameters, collateral rules, oracle reliability, and market-level controls.

From Morpho’s perspective, the strategic benefit is distribution. DeFi lending protocols usually compete for liquidity from crypto-native users. Tempo could open access to a different type of flow: fintech balances, payment float, merchant funds, and enterprise stablecoin liquidity.

For Tempo, this makes the chain more useful. A payments chain where balances only move in and out has limited stickiness. A payments chain where balances can also be lent, borrowed against, or used as collateral becomes more like a full financial operating system.

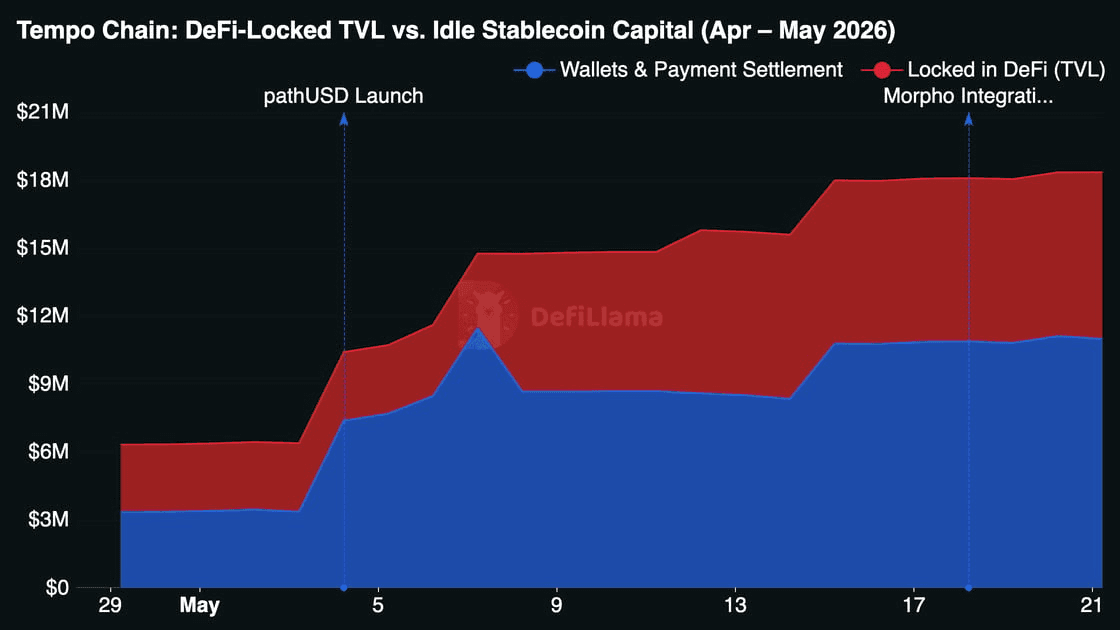

Source: DeFiLlama

Tempo's $18.3M in on-chain stablecoins tells two stories at once. $7.4M (40%) is locked in DeFi protocols which is captured in TVL. The remaining $10.9M (60%) sits in wallets or flows through payment settlement rails, never earning a basis point. That gap is precisely what the Morpho integration is built to close: curated lending vaults that let enterprises put idle stablecoin float to work without routing capital off-chain. The pathUSD launch on May 4 made the idle layer visible nearly doubling the undeployed balance overnight.

There are three main use cases to watch:

Yield on idle stablecoins: enterprise or fintech balances can potentially earn lending yield.

Borrowing and liquidity management: users may borrow against supported collateral instead of liquidating assets.

Embedded financial products: fintechs can build savings, credit, or treasury products using Morpho in the background.

However, this is not risk-free adoption. Lending markets introduce risks that payments alone do not: smart-contract risk, oracle risk, liquidation risk, collateral risk, curator risk, and liquidity risk. Curated markets can reduce some complexity, but they do not remove the need for due diligence.

The big question is whether this brings genuinely new liquidity into DeFi. If Tempo mostly attracts existing DeFi capital, the impact is smaller. But if fintechs and enterprises start routing real payment balances into Morpho markets, this becomes a meaningful expansion of DeFi’s addressable market.

The key takeaway: Tempo integrating Morpho shows that stablecoin payments and DeFi lending are converging. Payments may be the front door, but credit and yield are where deeper institutional use cases emerge. Users should still watch market parameters, collateral quality, oracle design, and whether early liquidity is organic or incentive-driven.

Mapping the Graph: A New Cohort of DeFi Risk Tools

DeFi risk monitoring is moving past the flat dashboard and past the static periodic risk check. Recent incidents have shown that economic alerts blur when the bulk of damage propagates as second and third order effects through dependencies, rather than landing at the point of original failure. A cohort of projects is responding by treating DeFi as a network problem rather than a list of TVL and APY readings, and treating risk as a continuous state rather than a snapshot. The shared thesis is straightforward: protocol composability creates dependency chains that simple metrics cannot resolve. A vault holds a wrapped token. The wrapper draws on a curator strategy. The strategy posts collateral into a market whose oracle topology is shared with three other protocols. When something breaks, the loss does not respect categories. Mapping the graph continuously is becoming as important as monitoring the numbers.

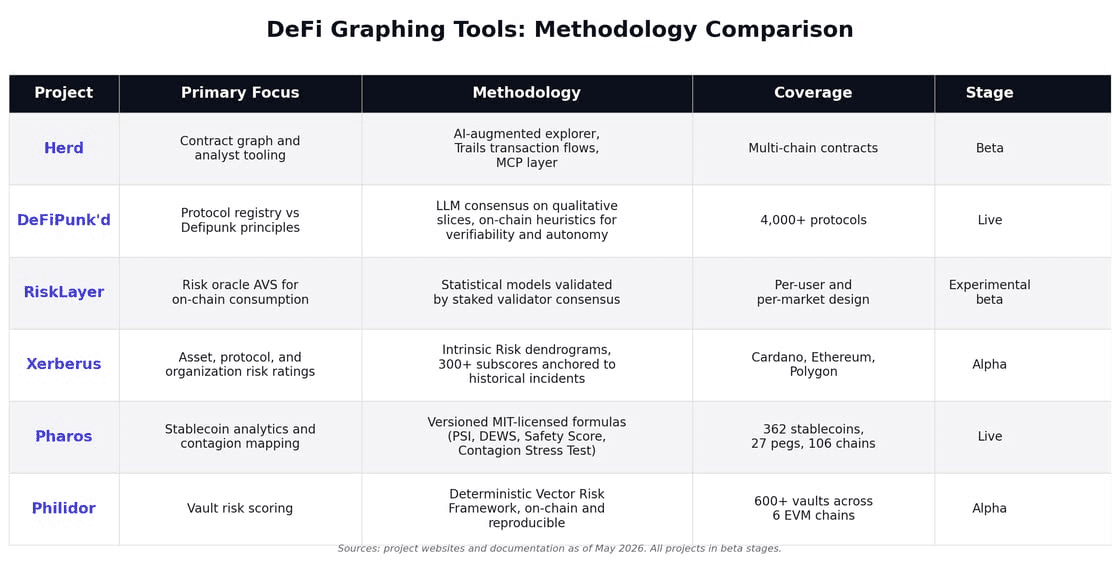

Six projects illustrate the range of approaches. Each takes a different angle on what to measure and how to surface it.

Herd: AI-augmented contract explorer with shareable transaction flows and an MCP layer for analyst agents.

DeFiPunk'd: open-source registry grading over 4,000 protocols against the Ethereum Foundation's Defipunk principles, using LLM consensus on qualitative slices and on-chain heuristics for verifiability and autonomy.

RiskLayer: EigenLayer-secured Risk Oracle AVS where staked validators score protocols. Beta site explicitly labeled experimental.

Xerberus: Intrinsic Risk dendrograms covering 300+ subscores across 85+ DeFi mechanisms, each anchored to a historical incident.

Pharos: stablecoin tracker covering 362 coins across 27 pegs and 106 chains via versioned, MIT-licensed formulas including PSI, DEWS, and a Contagion Stress Test.

Philidor: vault risk scorer covering 600+ vaults via a deterministic Vector Risk Framework that decomposes asset composition, platform security, and governance.

Source: DeFiLlama

The methodologies do not converge. Pharos, Philidor, and Xerberus produce formulaic, evidence-anchored, versioned scores. DeFiPunk'd is qualitative and consensus-driven. RiskLayer combines statistical models with reputation-weighted social validation. Herd does not publish a risk score at all. It surfaces the graph itself for downstream interpretation. Coverage differs as sharply as method. Pharos is stablecoin-only. Philidor is vault-only. Xerberus separates assets, protocols, and organizations into independent rating tracks. DeFiPunk'd is protocol-wide. RiskLayer targets per-user and per-market scoring. Herd indexes contracts.

A useful split runs through the cohort: tools that publish reproducible math against on-chain data and tools that rely on qualitative judgment or social consensus. Both carry signal. Quantitative scorers expose their weights, formulas, and incident anchors and can be checked independently. Qualitative registries surface posture, openness, and governance dimensions that resist clean quantification. Neither approach is finished work. All six projects remain in beta stages, coverage varies, and there is no shared standard for what a "risk score" means across them. A protocol rated A by one tool and flagged red by another is rarely a contradiction. The split usually reflects different definitions of risk, different weights on what matters, and different evidence bases.

The practical reality is that the heaviest users of these systems will not be retail allocators. Curators, risk teams, and technical institutions already operate their own internal frameworks for grading assets, vaults, and protocols. For them, a third-party rating is rarely the input they need. What matters is access to clean, reliable, on-chain data delivered in real time, surfaced in a form their own models can consume. Tools that produce opinionated scores will compete against well-developed in-house views. Tools that expose the underlying graph and the live state of the system stand to become infrastructure, regardless of which scoring framework eventually sits on top. Pairing that kind of structural data layer with economic risk monitoring, which quantifies parameter and market exposure block by block, gives the fullest view.

Sentora's economic-risk surface at defirisk.sentora.com sits on the latter side of that pairing.