The aggregate market capitalization for tokenized commodities and equities has reached a record $7.32 billion, reflecting an 8.58% increase over the last 30 days. While the sector includes a diverse range of assets, the flight to quality is primarily anchored by gold-backed tokens. This trend is visually evident in the market growth since late 2025, where active addresses (54,639) and total holders (185.69K) have scaled alongside geopolitical friction.

The primary catalyst for this expansion is the “weaponization” of trade through aggressive U.S. tariff proposals. As tariffs introduce volatility into fiat currency pairs, DeFi power users are increasingly treating gold as a neutral settlement layer. Unlike traditional gold ETFs, tokenized gold offers 24/7 liquidity and instant composability, making it a superior hedge during high-stress news cycles that occur outside of banking hours.

Tether Gold (XAUt) leads the category with a market cap of approximately $2.7B, benefiting from deep integration with the USDt ecosystem.

Paxos Gold (PAXG) follows with roughly $2.5B, remaining the preferred choice for users prioritizing regulatory compliance and direct bar-level transparency.

Monthly Transfer Volume for the sector has exploded to $17.11 billion, suggesting these assets are being used for active rebalancing rather than passive holding.

The 62.96% monthly surge in volume highlights a shift toward productive gold. In the current lending environment, XAUt and PAXG are frequently used as low-risk collateral to draw stablecoin liquidity on platforms like Aave. This allows investors to maintain exposure to the “gold-basis” trade while participating in on-chain yield strategies, effectively eliminating the opportunity cost usually associated with holding physical metals.

Source: RWA.xyz

Beyond gold, the $7.32B total cap includes a growing “long tail” of tokenized assets like silver and equities, which are beginning to see similar adoption patterns. As the infrastructure for oracles and cross-chain bridging matures, the ability to move institutional-scale value into “hard assets” with a single transaction is becoming a standard feature of professional DeFi portfolios.

The parabolic growth in the number of holders signals a democratization of commodity access. Fractionalized ownership allows retail participants to hedge against local currency devaluation with the same efficiency as large-scale institutions. However, this growth also increases the importance of monitoring on-chain liquidity depth, as the high transfer volume ($17.11B) requires robust market-making to prevent slippage during market-wide panics.

Disclaimer: The information provided in this newsletter is for educational and informational purposes only and does not constitute financial, investment, or legal advice.

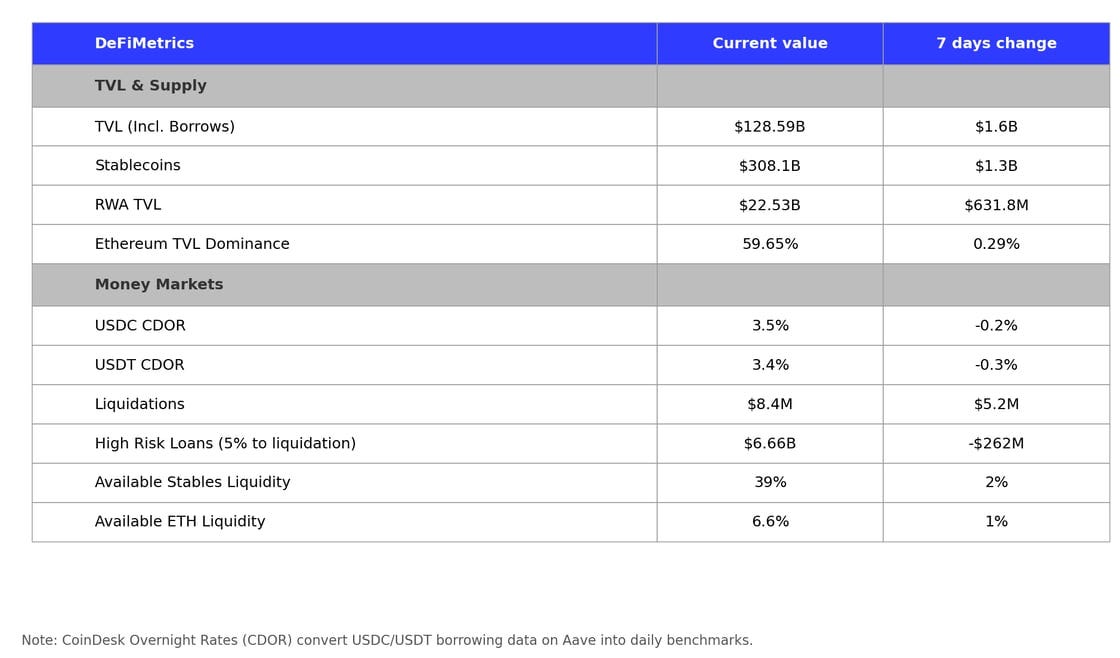

Key Weekly DeFi Metrics

Our key takeaways for this week are:

Liquidations Spiked: $5.2M in new liquidations suggest a volatile week for leveraged traders.

RWA Growth: Real World Assets added $631.8M, continuing their steady climb.

Deleveraging Trend: High-risk loans dropped by $262M while overall liquidity improved.

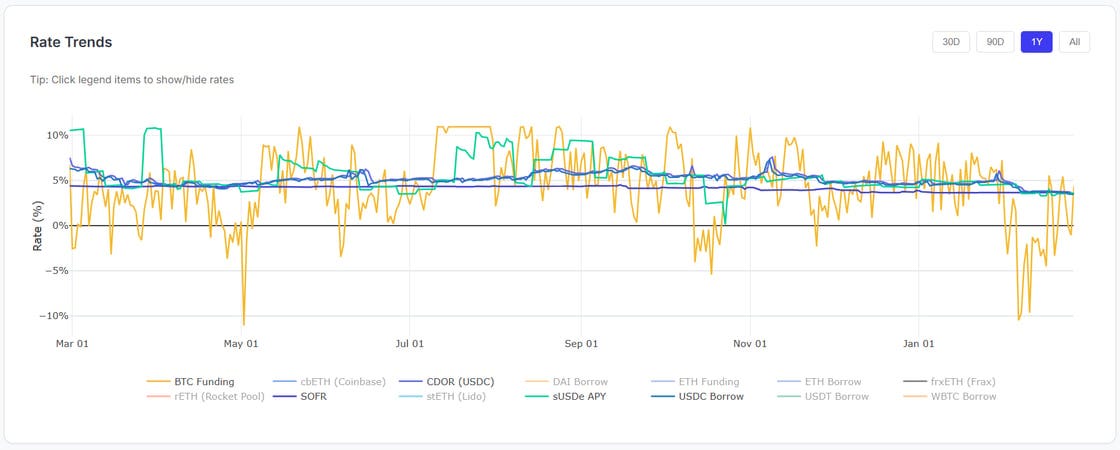

Stablecoin Yield Compression

USDC CDOR fell 20 bps to 3.5%; USDT CDOR fell 30 bps to 3.4%, both dropping below SOFR for the first time. Both are the largest single-week drops seen in the past month, and the mechanism is straightforward: when BTC funding rates turn negative, the incentive to borrow stablecoins to go leveraged long disappears. Borrow demand falls, utilisation rates drop, and protocol rates follow mechanically.

Available stablecoin liquidity on Aave rose 2 percentage points to 39%, confirming the reduced borrow demand picture. When leverage sentiment is constructive, that number compresses toward 20–25%. Its expansion to 39% is a signal that the leveraged-long cohort has stepped back.

Liquidations ticked up to 8.4M on the week, with the 5.2M week-on-week increase concentrated around BTC’s mid-week dip through 64,000. The good news: high-risk loans within 5% of liquidation price fell 262M. Some of that is deleveraging (positions closed voluntarily), and some is price recovery reducing the risk gap.

Either way, the tail risk in the active loan book is smaller going into next week.

TVL including borrows rose to $128.6B, healthy growth despite softer leverage conditions, driven largely by continued RWA inflows. Ethereum maintained its 59.65% TVL dominance share, up 29 basis points, as ETH-denominated collateral appreciated relative to the rest.

Source: Sentora

In summary, the longer BTC stays below the $100K mark while gold grinds to new records, the more clearly the divergence becomes a macro signal rather than a short-term trade. If the current trajectory holds, tokenized gold TVL could test $10B later this year, particularly if any major custodian or prime broker adds PAXG or XAUT to an approved collateral list.

Gold’s outperformance is also a proxy for something else: a rotation toward lower-volatility, non-yield-bearing stores of value at a moment when both crypto leverage and traditional fixed income carry have become less attractive.