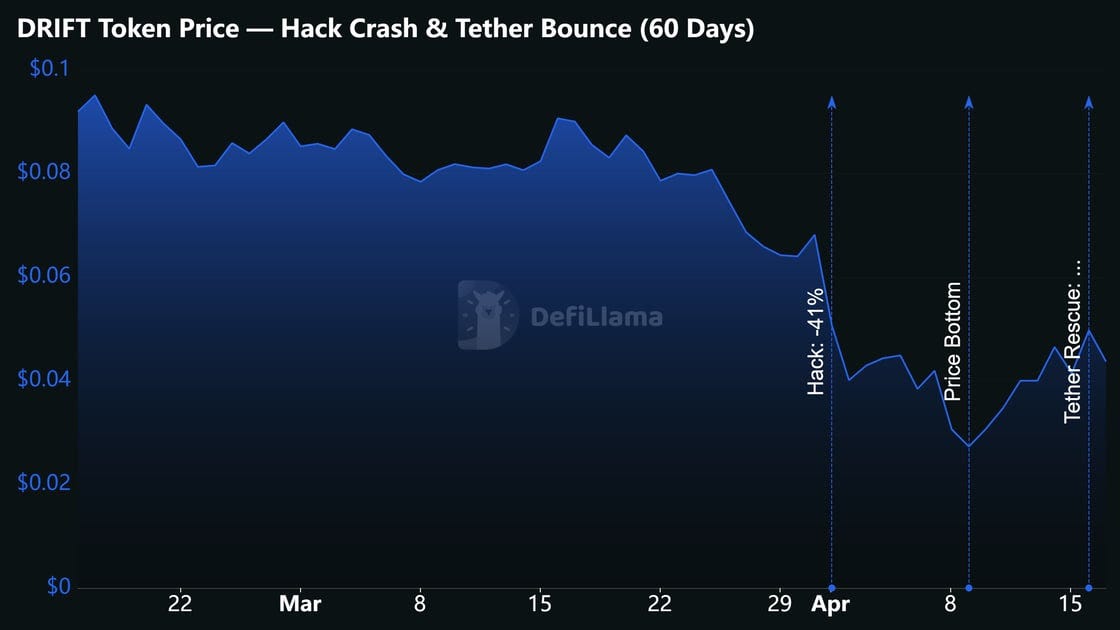

On April 1, hackers linked to a North Korea’s group drained $285 million from Drift in under 12 minutes. The attack was not a smart contract exploit but an operational security failure six months in the making. The attackers built false identities, met Drift contributors in person across multiple countries, and ultimately obtained approval signatures from two of Drift’s five Security Council members using Solana’s durable nonce feature.

On execution, they listed fraudulent tokens as valid collateral, raised withdrawal limits, and emptied the protocol across several transactions. The largest single component was $155.6 million in JLP tokens, followed by $60.4 million in USDC. Solana DeFi TVL fell 12% in the days after, from $8.1 billion to $5.7 billion, with downstream losses across at least 20 connected protocols exceeding $22 million.

Source: DefiLlama

The $147.5 million package announced April 16 breaks down as follows:

Tether is providing a $100 million revenue-linked credit facility and $27.5 million in direct support via an ecosystem grant and market maker loans.

Ecosystem partners contribute the remaining $20 million.

Affected users receive transferable recovery tokens representing a claim on a recovery pool, funded by ongoing Drift exchange revenue plus the committed capital.

Full repayment of the $285–295 million loss depends entirely on Drift generating sustained trading volume after relaunch. Users who lost deposits are not being made whole immediately, they are being given a revenue share instrument and told to wait.

Circle vs Tether

After the hack, attackers converted most of the stolen assets to USDC and moved $232 million across Circle’s CCTP bridge from Solana to Ethereum in more than 100 transactions over six hours. Circle did not freeze the funds. CEO Jeremy Allaire, speaking in Seoul on April 13, said the company freezes wallets only when directed by law enforcement or courts: “Circle follows the rule of law.” Blockchain investigator ZachXBT countered that Circle’s inaction across more than a dozen cases since 2022 has contributed to over $420 million in illicit funds escaping.

Tether has positioned itself as the opposite: proactive, willing to freeze funds without waiting for a court order, and publicly claiming to have recovered $800 million in stolen crypto through partnerships with 10 law enforcement agencies across 64 countries. Both models carry real trade-offs. Tether’s approach gives it discretion to act unilaterally while Circle’s gives it regulatory predictability. The practical consequence this week was that $232 million moved through USDC rails without interruption, and Tether is collecting Drift’s relaunch as a direct result.

The USDT pivot on Solana

The strategic dimension is hard to miss. Solana has been a USDC stronghold: USDC’s on-chain market cap on Solana sits at $8.1 billion against USDT’s $3.05 billion, a 2.65x advantage. Drift’s pre-hack TVL was $550 million, making it Solana’s eighth-largest protocol. Tether claims the relaunch will onboard more than 128,000 users and 35 ecosystem teams onto USDT-based markets on Solana. If Drift recovers meaningful volume, this is a material dent in USDC’s Solana dominance, achieved at the cost of a $127.5 million credit facility that is repaid through the exchange’s own future revenue.

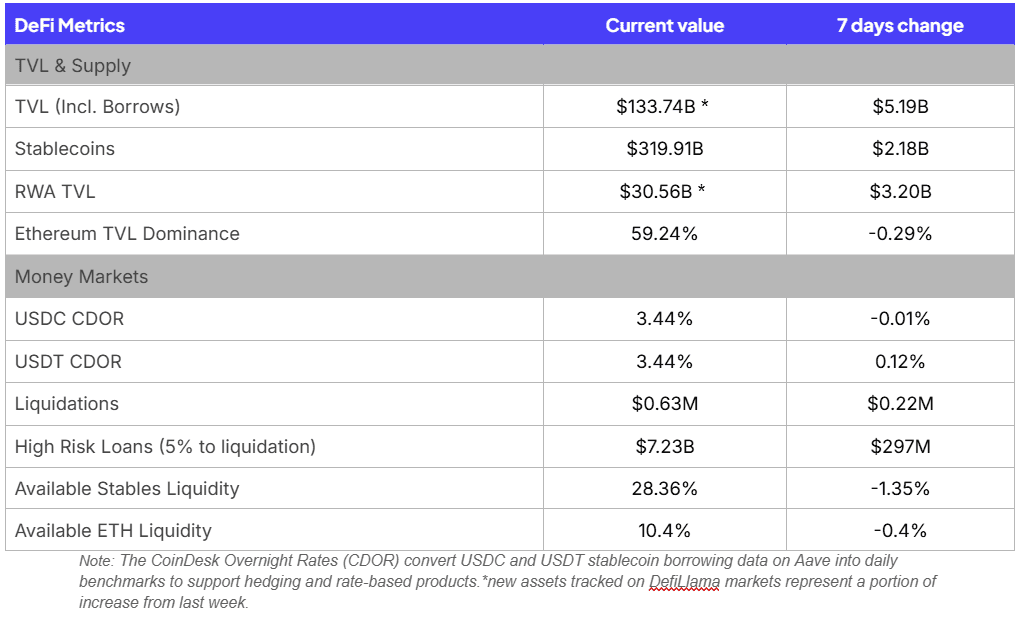

Key Weekly DeFi Metrics

Key takeaways for this week:

Most notable item is the convergence of CDOR rates. This signals that users are pricing the risks of the two stablecoins similarly compared to before.

Stablecoin availability has been dropping as users increase leverage expecting more favorable market conditions to come.

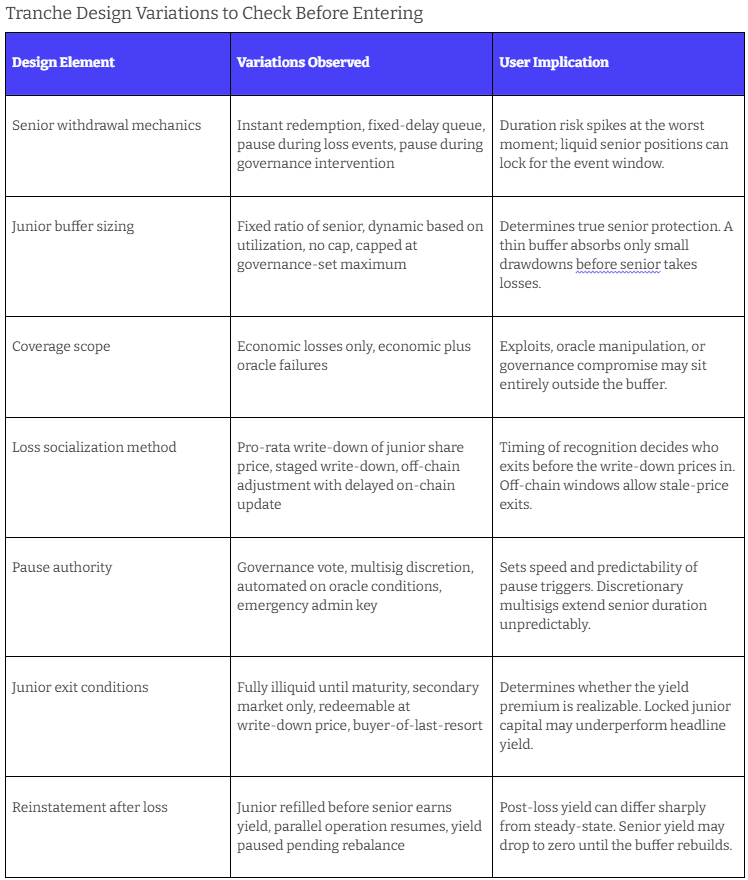

Tranched Yield Products: Mechanics Matter

A new class of DeFi protocols now offers tranching as a generalized primitive, splitting any yield-bearing asset into junior and senior tranches without requiring the asset issuer to build the structure itself. Junior tranches absorb first losses for boosted yield; senior tranches sit behind that buffer for a lower but structurally protected rate. The design mirrors traditional credit tranching, but because any asset can be wrapped this way, implementations vary sharply, and those differences determine what happens to user capital under stress.

The most common gap between expectation and reality is duration. Senior tranches are marketed as the lower-risk, more liquid option, but many designs include pause logic or redemption queues that activate precisely during loss events, governance interventions, or oracle freezes. A senior holder expecting same-day redemption can find their position locked for an assessment window, socialization process, or rebalancing cycle. Junior tranches are illiquid by construction, so that illiquidity is priced in; senior duration risk is often only visible in the withdrawal state machine.

The second consideration is coverage scope. Junior buffers are almost always sized against expected economic drawdowns (liquidation losses, basis slippage, depeg absorption, negative funding), not technical exploits, oracle manipulation, or governance compromise. The Resolv USR mint exploit illustrates the gap: RLP was designed to absorb economic drawdowns in the delta-neutral strategy backing USR, but a smart contract vulnerability damaged the peg directly, and how RLP’s mandate applies to a non-economic loss of that kind remains unclear. Senior holders relying on the buffer for safety should confirm what it covers and what happens when a loss falls outside that scope.

None of this argues against tranched products. Differentiating risk profiles on a shared collateral pool is a clear improvement over monolithic yield vaults and opens assets to users who would otherwise hold neither the unlevered nor the leveraged version. Tranching changes the shape of risk, it does not eliminate it, and that shape is defined by design choices that differ materially between protocols. Before entering a junior position, confirm the drawdown scenarios that trigger a write-down and whether it is pro-rata or staged. Before entering a senior position, confirm the pause and redemption conditions and the exact coverage scope of the buffer.

Stablecoins have become a core part of how institutions move and manage capital. But despite the rapid growth in stablecoin usage, a large portion of institutional balances still sit idle. Fireblocks Earn feature, announced this week, is designed to change that by making it easier for institutions to access onchain lending opportunities through a familiar operational environment. Sentora is a key partner for this new feature, acting as the curator for Morpho curated vaults.