Circle’s cirBTC Bid to Expand Bitcoin’s Role Across Institutional DeFi

Circle unveiled cirBTC this week as a new tokenized Bitcoin product aimed at bringing BTC deeper into DeFi. On its product page, Circle says cirBTC will be 1:1 backed by native BTC, with reserves designed to be independently verifiable on-chain, and that the token will launch first on Ethereum and Arc, pending regulatory approvals.

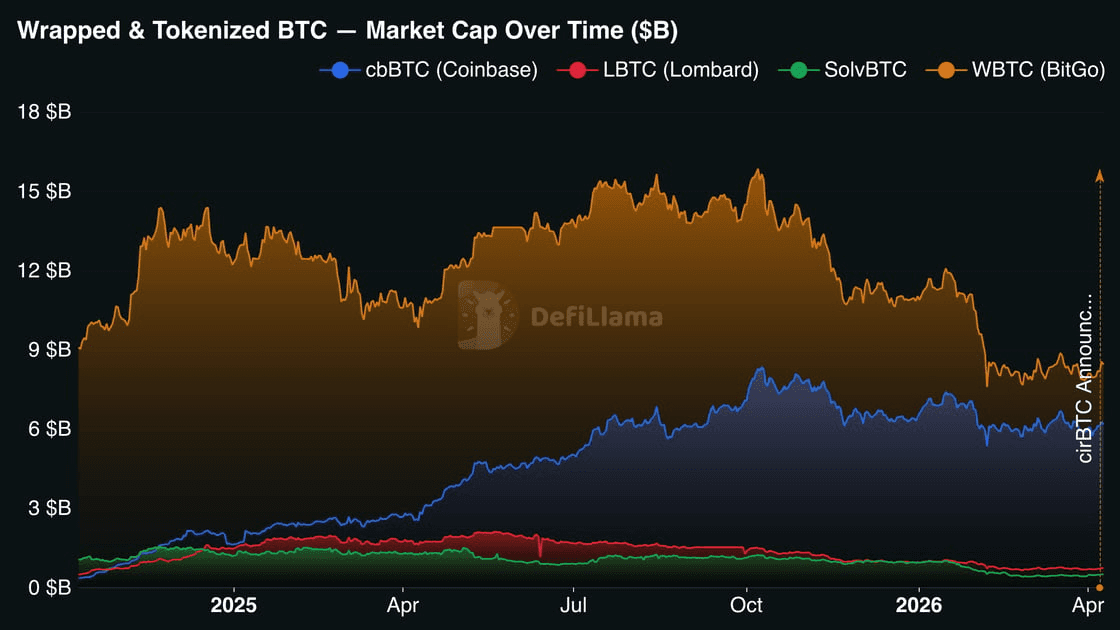

Circle is entering a market that already has clear incumbents. DefiLlama currently shows WBTC at about a $8.4B market cap, while cbBTC is around $6.2B. That means the wrapped BTC category already has meaningful scale, but it is still small relative to Bitcoin itself, which is valued at nearly $1.43T.

That gap is the opportunity Circle is targeting. Even the two biggest wrapped BTC products together represent only about 1% of Bitcoin’s total market cap, which means most BTC is still not actively usable across lending, liquidity, and collateral-based DeFi strategies. In other words, cirBTC is a bet that BTCfi can still grow if the wrapper becomes more trusted and more institutional.

Source: DefiLlama

On the infrastructure side, cirBTC is built to sit within Circle’s broader stack via USDC, Arc, and Circle Mint. Circle is positioning cirBTC as a secure, transparent, and institutionally usable wrapped BTC product, with 1:1 BTC backing, real-time on-chain reserve verification, and a design aimed at counterparties that need a neutral, high-performance tokenized Bitcoin.

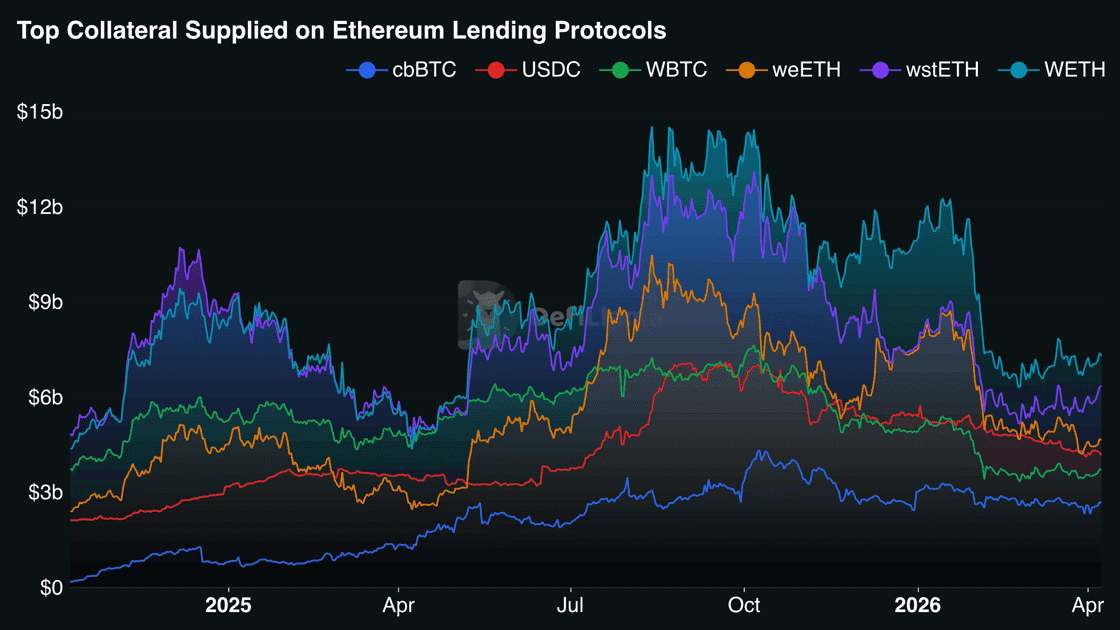

The most important use case to watch is cirBTC as DeFi collateral. Circle explicitly says the product is suited for OTC desks, market makers, and lending protocols, which strongly suggests cirBTC is being designed for environments where tokenized BTC needs to do more than sit passively in a wallet. In practice, that means potential use in borrowing against BTC, posting BTC in money markets, using it as inventory in liquidity pools, or pairing it with USDC in more capital-efficient trading and treasury strategies. Some of that is inference, but it follows directly from the types of counterparties Circle says it is targeting.

Source: DefiLlama

For cirBTC to win, Circle needs to outperform on four fronts:

Liquidity: institutional users do not care about wrappers in the abstract; they care about whether the asset clears efficiently across DEXs, RFQ venues, and lending markets. Existing competitors already have a multi-billion-dollar scale.

Integrations velocity: the faster cirBTC appears in major lending markets, collateral frameworks, vaults, and liquidity pools, the faster it can become operationally relevant rather than merely available. Circle is clearly designing for that by launching on Ethereum first and plugging into its existing stack.

Counterparty trust: Circle’s main narrative is that reserve verification and infrastructure familiarity reduce wrapper anxiety. That message will resonate only if the market treats those assurances as materially better than incumbent solutions.

Mint/redeem usability: institutional wrappers live or die by operational smoothness. A wrapper can be perfectly collateralized and still fail to scale if minting, redemption, onboarding, or legal access are too constrained.

Circle has a strong distribution and infrastructure advantage, but cirBTC still needs real post-launch traction in minted supply, pool depth, lending adoption, and collateral usage before it can be considered a serious incumbent challenger. Until then, the thesis is clear, but execution remains the test.

Disclaimer: The information provided in this newsletter is for educational and informational purposes only and does not constitute financial, investment, or legal advice.

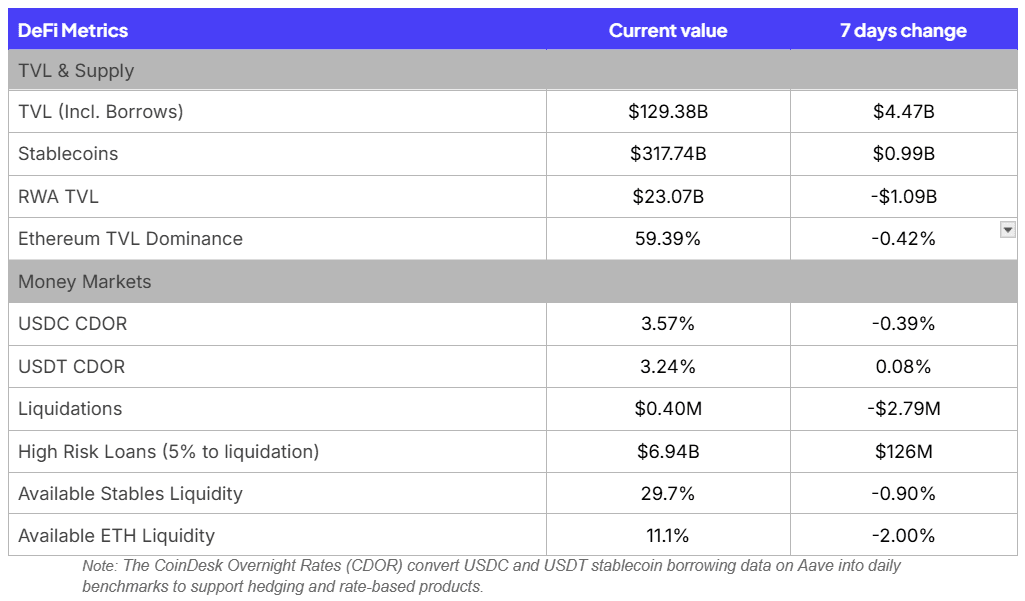

Key Weekly DeFi Metrics

Key takeaways for this week:

A ~$4.5B increase in TVL reverses last weeks drop

USDT and USDC CDOR are converging, suggesting users are trying to optimize for cheapest borrow rates

Large drop of 2% in ETH available liquidity can be largely attributed to increases in borrows on Aave due to specific LRT campaigns incentivizing leverage

Open Bad Debt: A New Way to Evaluate Market Health

The Sentora Risk Radar introduces Open Bad Debt as a primary indicator for assessing the solvency of lending protocols. Lending markets depend on liquidators to protect protocol health, but this mechanism relies on collateral maintaining enough value to cover outstanding loans. Open Bad Debt identifies positions where this threshold is crossed. By tracking loans where collateral is worth less than the debt, this metric highlights unrecovered losses before they are officially realized by the protocol.

Indicators Defined

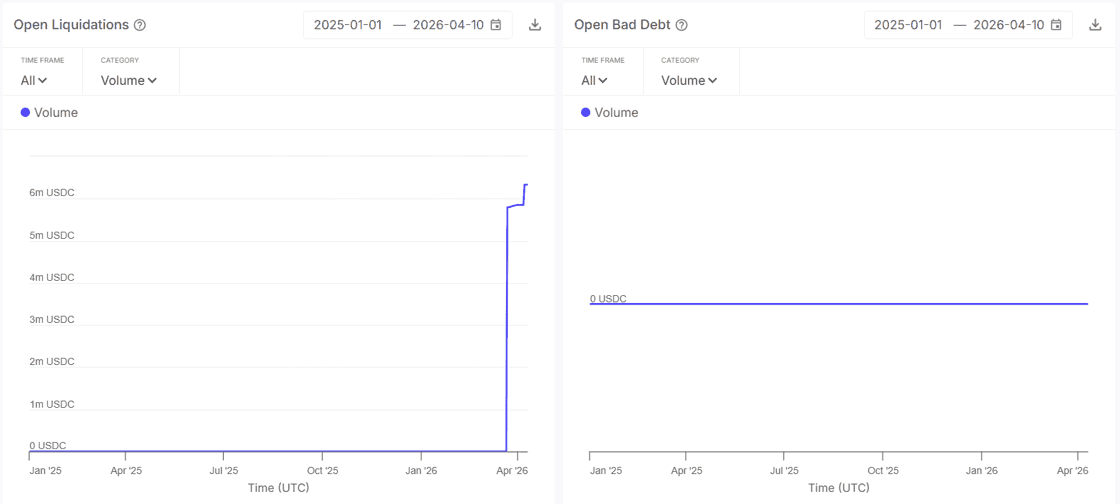

Open Bad Debt: Positions where collateral value is less than debt value that remain active on the balance sheet. This metric tracks positions with health factors below 0.9 as open bad debt.

Open Liquidations: Positions with health factors between 0.9 and 1.0. These remain pending for liquidation and still contain enough collateral to incentivize liquidators to close the position for a profit.

Lending protocols frequently carry small amounts of open bad debt. These dust positions remain after users close out the majority of their loans and often stay on the books because gas costs exceed the profit for liquidators. Risk becomes significant only when the volume shows sustained growth or sudden, sharp increases. For institutional lenders, these spikes suggest that the collateral is distressed and liquidators are actively avoiding the market.

Market stability relies on liquidators acting as the first line of defense. When open liquidations decrease but open bad debt increases, it suggests that the market is deteriorating. This trend indicates that liquidity has dried up and deposits may become trapped in an insolvent pool. Whales and institutional providers monitor this shift to ensure they can withdraw capital before the pool becomes illiquid.

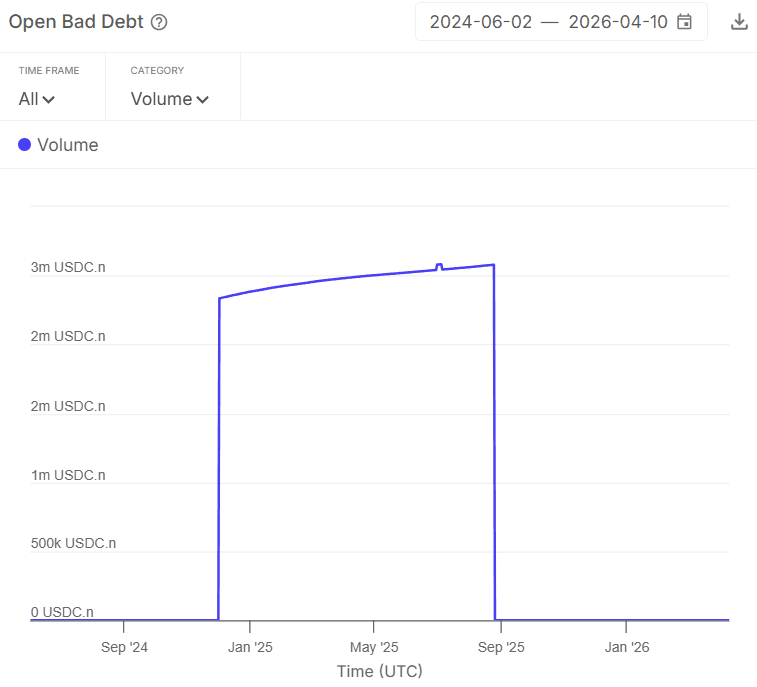

Historical data from the summer of 2025 illustrates this risk. A specific market carried a peak of approximately $2.58M in open bad debt for several weeks. An external address that wasn’t the address holding the debt eventually repaid, realizing the bad debt. This created a high risk in the market that had at the time ~$300M in supply. This type of scenario is where the open bad debt indicator can play an important role for potential suppliers to identify risks.

Source: Sentora Risk Radar

The wstUSR-USDC market provides a clear example for tracking the transition from open liquidations to open bad debt. Following a resolve exploit, an oracle price mismatch prevented liquidators from profitably closing positions despite low health factors. Users can observe open liquidations climbing to roughly $6.33M as of April 2026. As these stagnant positions see their health factors drop below 0.9, they will migrate into the open bad debt category.

Source: Sentora Risk Radar

Open bad debt provides transparency needed to evaluate protocol solvency in real-time. To explore this metric and track live market health across various protocols, visit the Sentora Risk Radar.