This week, the institutional DeFi story split into two complementary tracks: private, compliance-oriented infrastructure attracted more than $1.0B of disclosed capital, while Hyperliquid continued to show how public onchain venues can concentrate stablecoin liquidity at scale.

The connection is that institutional crypto market structure is starting to bifurcate between controlled environments for regulated balance sheets and high-velocity public venues where stablecoins, collateral, and execution live directly onchain.

Private Rails Get Funded

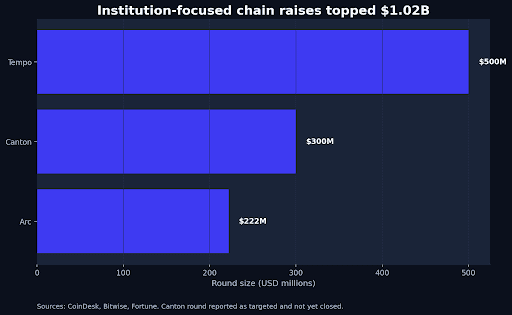

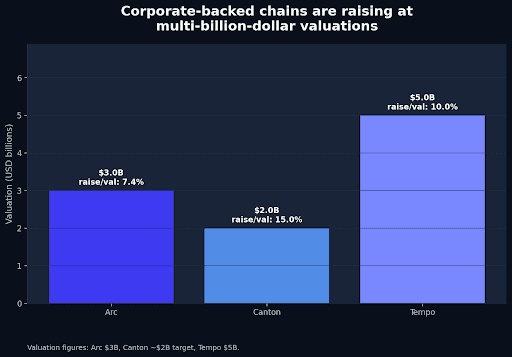

Arc, Canton, and Tempo are becoming a useful proxy for what institutional blockchain infrastructure buyers are willing to fund. Across the three networks, disclosed or reported raises total $1.022B, with combined valuations of roughly $10B. That is large enough to treat the week’s headlines as a capital-allocation signal, not just another round of L1 branding.

The funding mix matters because each project targets a slightly different version of the same institutional constraint: how to use tokenized assets and stablecoins without exposing every transaction, position, or workflow to a fully public mempool and block explorer.

Arc: Circle raised $222M for the ARC token at a $3B valuation, with investors including BlackRock, Apollo, a16z crypto, ARK Invest, Intercontinental Exchange, Standard Chartered Ventures, Haun Ventures, Bullish, and others. Arc is positioned around stablecoin-based capital markets, tokenized assets, cross-border settlement, and regulated onchain finance.

Canton: Digital Asset is reportedly seeking about $300M at a roughly $2B valuation, led by a16z crypto, with the final amount still subject to close. Canton’s pitch is narrower and more financial-market-native: privacy-enabled interoperability across permissioned applications used by banks, trading firms, custodians, and market infrastructure providers.

Tempo: Stripe and Paradigm-backed Tempo raised $500M at a $5B valuation late last year and remains part of this week’s discussion because it sits in the same payments-and-stablecoin design space. The strategic difference is distribution: Stripe brings merchant and developer reach that most crypto-native chains cannot replicate.

The shared design language is telling. These are not generalized “Ethereum killers” trying to win every developer category. They are purpose-built networks around stablecoins, tokenized assets, privacy, compliance, and predictable execution. For institutional investors, that is the practical framing: the market is funding controlled transaction environments because the transparency that makes public crypto auditable can also become a business leak.

Bitwise CIO Matt Hougan summarized the point directly: for a business, broadcasting every trade before completion or making payroll visible to a block explorer is a bug, not a feature. That does not invalidate public chains. It does explain why banks, asset managers, payment companies, and corporations are willing to back networks where selective disclosure, privacy, and workflow control are built into the base product rather than added later.

The regulatory backdrop is also doing work. After the U.S. stablecoin-focused Genius Act passed in 2025, large institutions have had a clearer path to underwrite infrastructure tied to stablecoins and tokenization. The next policy variable is the CLARITY Act: if market-structure legislation provides workable treatment for tokenized assets, DeFi interfaces, and network tokens, the institutional infrastructure opportunity could widen beyond payment chains into trading, collateral, and automated market operations.

For investors, the key read-through is not “privacy chains win.” It is more nuanced:

Institutional flows need discretion. Not every treasury movement, repo workflow, or customer payment should be public by default.

Public-chain liquidity still matters. Private or permissioned venues need bridges into wider settlement assets, collateral, and market depth.

Corporate distribution is now part of chain competition. Circle, Digital Asset, Stripe, and their partners can bring customers, compliance teams, and procurement channels that crypto-native protocols usually have to earn one integration at a time.

Valuation is already pricing execution risk. A combined $10B valuation base assumes these networks convert strategic backing into live usage, not just pilots.

That last point is important. The raises are not proof of product-market fit; they are proof that institutional buyers want a different privacy and control surface than the one offered by default public-chain infrastructure. The next observable metrics should be live transaction value, stablecoin circulation, tokenized collateral outstanding, active institutional counterparties, and whether applications built on these networks can interoperate with broader liquidity without creating new trust bottlenecks.

This is the bridge into Hyperliquid. If Arc, Canton, and Tempo represent the controlled side of the institutional stack, Hyperliquid represents the opposite pressure: traders continue to reward venues where liquidity, execution, and collateral are immediately usable. The institutional DeFi opportunity is likely to sit between those poles, with private workflows upstream and liquid public venues downstream.

Public Liquidity Gets Distribution

Coinbase’s Hyperliquid move is the other side of the same market-structure shift. According to CoinDesk, Coinbase will become the official treasury deployer of USDC on Hyperliquid under the network’s Aligned Quote Asset framework. The arrangement gives Coinbase a central role in managing stablecoin liquidity on one of the fastest-growing onchain trading networks, while USDH remains redeemable for USDC or fiat during a migration period before being phased out over time.

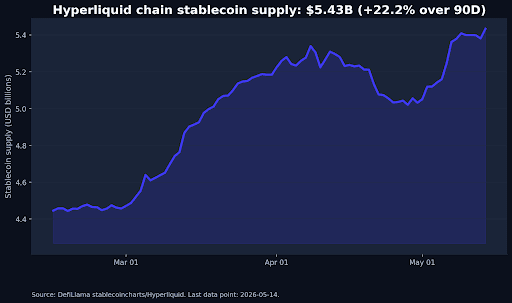

The quantitative context is already meaningful. DefiLlama’s Hyperliquid chain-level stablecoin series shows roughly $5.43B in stablecoin supply as of May 14, 2026, up about 14% over 90 days in the generated chart window. CoinDesk separately reported that USDC supply on Hyperliquid was nearing $5B, which is directionally consistent with the onchain stablecoin data.

Stablecoin liquidity is not a side-detail for a perps venue. It is the settlement asset, the collateral base, and the quote currency that defines how quickly traders can move between risk, cash, and leverage. If Coinbase can deepen USDC’s role inside Hyperliquid, it extends USDC beyond centralized exchanges and Ethereum into a venue where onchain traders already spend time and post collateral.

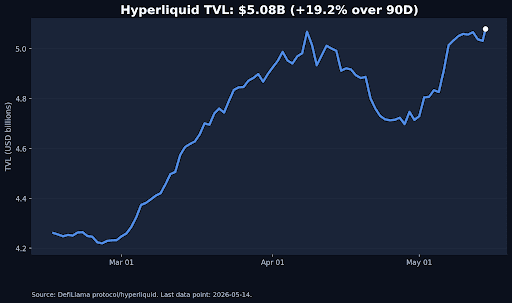

The second metric is TVL. DefiLlama shows Hyperliquid TVL near $5.08B as of May 14, after a strong 90-day expansion. TVL is not the same as volume, and it should not be treated as a perfect proxy for trading activity. But in this case it is still useful because it indicates that a large pool of user capital is staying inside the venue rather than only touching it for short-lived transactions.

The Coinbase angle changes the interpretation of that capital base. Hyperliquid was already competing on product quality: fast execution, low fees, deep perps liquidity, and a UX close enough to centralized exchanges to attract active traders. Coinbase brings a different asset: regulated U.S. brand trust, USDC distribution, fiat adjacency, and balance-sheet discipline around reserves and treasury deployment.

For DeFi power users, this creates several practical questions:

Who owns the settlement layer? If USDC becomes the dominant quote and collateral asset on Hyperliquid, Coinbase and Circle gain a stronger position inside public onchain derivatives infrastructure.

How much protocol revenue shifts to treasury design? The AQA framework reportedly shares reserve yield revenue with the protocol, making stablecoin deployment part of venue economics rather than a passive balance.

Does CeFi distribution strengthen or soften decentralization? A trusted treasury deployer may improve liquidity quality, but it also introduces concentration risk around stablecoin operations and issuer strategy.

What happens to native stablecoin experiments? USDH being sunset over time suggests that venue-native stablecoins face a high bar when large, regulated stablecoins can plug into the same demand.

Institutional infrastructure and public DeFi venues are both moving toward the same base asset: regulated dollar liquidity. Arc, Canton, and Tempo are trying to build environments where that dollar liquidity can support tokenized real-world workflows with privacy and compliance. Hyperliquid is showing that the same dollar liquidity is also the core lubricant for onchain speculation, hedging, and market-making.

The strategic implication is that stablecoins are becoming less like standalone products and more like embedded market infrastructure. In private networks, they serve as settlement and treasury rails. On Hyperliquid, they are collateral, quote asset, redemption path, and revenue-sharing substrate. That convergence is why Coinbase’s role matters: it is not just adding USDC to another chain, it is helping define who controls liquidity operations inside a major onchain venue.

There are still real risks. Hyperliquid’s growth concentrates liquidity in a venue with its own technical, governance, and market-structure assumptions. Stablecoin dominance can improve UX and collateral efficiency, but it can also concentrate redemption, issuer, regulatory, and counterparty risk. TVL and stablecoin supply can reverse quickly if market conditions, incentives, or trust assumptions change.

The key takeaway is that institutional DeFi is no longer one clean narrative. Capital is funding private, institution-ready networks while liquid public venues are absorbing billions in stablecoin collateral. The opportunity is in understanding how those layers connect: privacy and compliance upstream, liquidity and execution downstream.