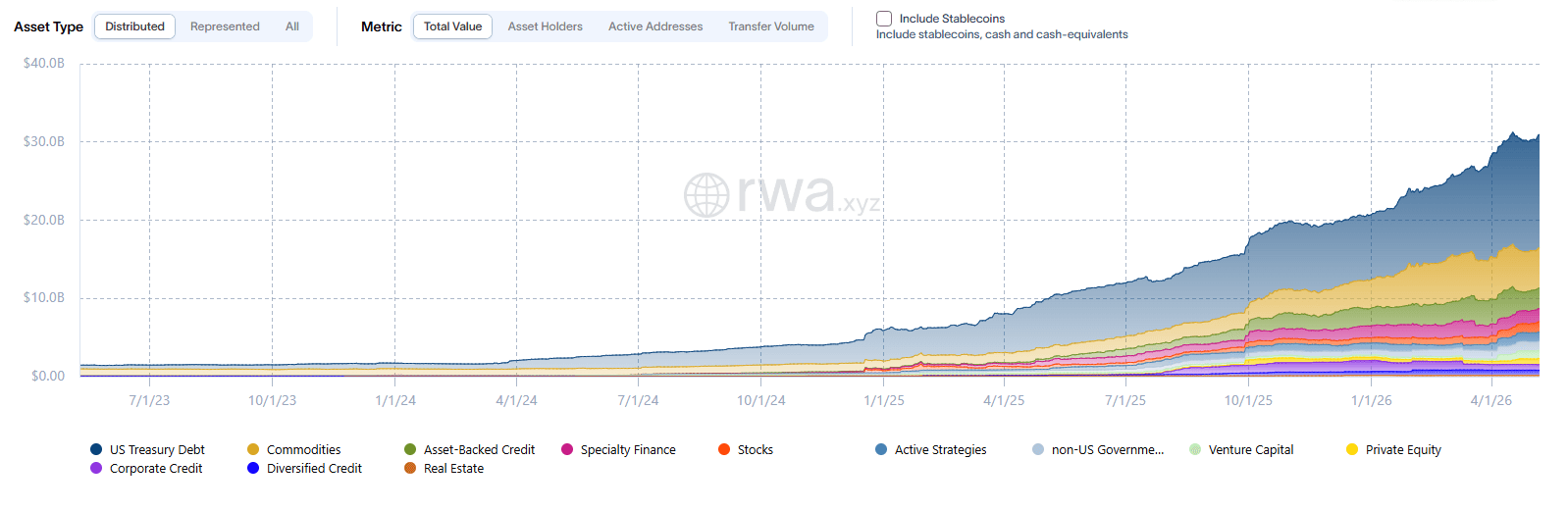

Solana's real-world asset ecosystem crossed $2.5 billion in total value locked this week, up from $215 million a year ago, as the Solana Accelerate conference on May 5 produced a set of institutional product launches: State Street and Galaxy's SWEEP tokenized liquidity fund, Anchorage Digital's cashless stablecoin reserve model with J.P. Morgan, and Western Union's USDPT stablecoin issued on Solana.

The network now accounts for 58% of deposits in dedicated RWA lending platforms, with $1.59 billion of that total in tokenized Treasuries.

In this issue, we examine the composition of Solana's RWA stack, the mechanics of the Accelerate launches, and what the institutional convergence means for the network's role in institutional finance.

Solana at $2.5b in RWA

Solana's RWA TVL reached $2.5 billion as of late April/early May, a 10x increase from $215 million one year ago. The composition matters: this is not a single product or a Treasury-only story.

The largest single asset is Hastra PRIME ($322M TVL), a stablecoin-like token backed by tokenized home equity credit lines. Holders earn up to 8% APY from a HELOC pool with over $1 billion in monthly originations, making it one of the clearest current examples of real mortgage-adjacent cash flows being packaged into a blockchain asset. BlackRock's BUIDL holds $231M on Solana, providing institutional Treasury exposure with 24/7 settlement. Ondo USDY contributes $179M in Treasury-backed yield. OnRe's ONyc ($165M) is the only tokenized reinsurance product in the top ten, giving on-chain investors exposure to insurance risk premiums. Maple Finance's syrupUSDC ($164M) targets private credit yield from institutional borrowers.

Tokenized equities are also live: xStocks' TSLAx ($53M), CRCLx ($44M), MSTRx ($27M), and SPYx ($24M) offer on-chain access to U.S. listings, alongside Ondo Global Markets' 200+ tokenized stocks and ETFs launched on Solana in January 2026.

One metric that stands out is DeFi utilization: 43.7% of Solana's active RWA market cap is deployed in DeFi lending, versus 6.1% on Ethereum. RWAs on Solana are being used as productive collateral. Treasuries make up 60% of the total ($1.59B), reflecting an institutional preference for yield-bearing, low-risk instruments over speculative exposure.

Source: rwa.xyz

The Accelerate Announcements

The Solana Accelerate conference on May 5 in Miami produced three distinct institutional product launches worth separating.

Western Union’s USDPT Stablecoin: Western Union officially entered the on-chain settlement space by launching USDPT, a U.S. dollar-denominated payment stablecoin, on the Solana blockchain. Issued by Anchorage Digital Bank (the first federally regulated crypto bank in the U.S.) and supported by Fireblocks infrastructure, USDPT is designed to replace slow, traditional correspondent banking rails with 24/7 "always-on" settlement. The rollout began in Bolivia and the Philippines, with a planned expansion to over 40 countries by the end of 2026 through a consumer-facing product called "Stable by Western Union."

State Street and Galaxy: SWEEP. State Street Investment Management and Galaxy Digital launched the State Street Galaxy Onchain Liquidity Sweep Fund. SWEEP gives qualified institutional investors a way to move stablecoins into a yield-bearing, onchain cash management product, targeting the idle-cash problem that affects institutions operating across market-hour limits and T+1 settlement windows. The fund launches on Solana, with Ethereum and Stellar support planned.

Anchorage Digital and J.P. Morgan Asset Management: cashless reserves. Anchorage announced plans for a "Cashless Reserves" model for stablecoin issuers, in which reserves are held in yield-bearing tokenized instruments on Solana rather than static cash buffers. J.P. Morgan Asset Management is engaged as the potential tokenized instrument provider. The structure uses just-in-time liquidity for redemptions, meaning issuers earn yield on reserves that would otherwise sit idle.

SoFi. SoFi, a regulated U.S. bank, announced plans to expand SoFiUSD to Solana and confirmed it is the first nationally chartered U.S. bank to accept direct Solana network deposits, allowing its 13.7 million members to transfer SOL from external wallets into the app.

Taken together, the Accelerate launches represent a distinct shift in where institutional product development is happening. Tokenized cash management, stablecoin reserve infrastructure, and bank-grade custody are all converging on the same network. The practical reason is the same across all three: Solana's throughput and sub-second finality make continuous settlement feasible in a way that Ethereum mainnet, with its higher latency and cost, does not.

Know the Bridge Before the Asset

Bridges have absorbed more loss than any other category of DeFi infrastructure. The largest exploits on record have, with very few exceptions, been bridge failures. Anyone holding an asset on a chain other than its native one is, by definition, exposed to the bridge that issued the wrapped or transferred form. The first question worth asking before any allocation is whether the asset in hand is native to the chain it sits on, or bridged onto it.

That question is rarely surfaced in user interfaces. USDC on Ethereum is native. USDC.e on Arbitrum is bridged through Arbitrum's canonical rollup bridge. USDC on Solana via Wormhole is wrapped through a different trust model entirely. The three trade under similar names, but the security of holding each depends on a distinct set of validators, contracts, or solvers. The token symbol does not tell you who can mint it, who can pause it, or who would have authority over the asset if the bridge were compromised.

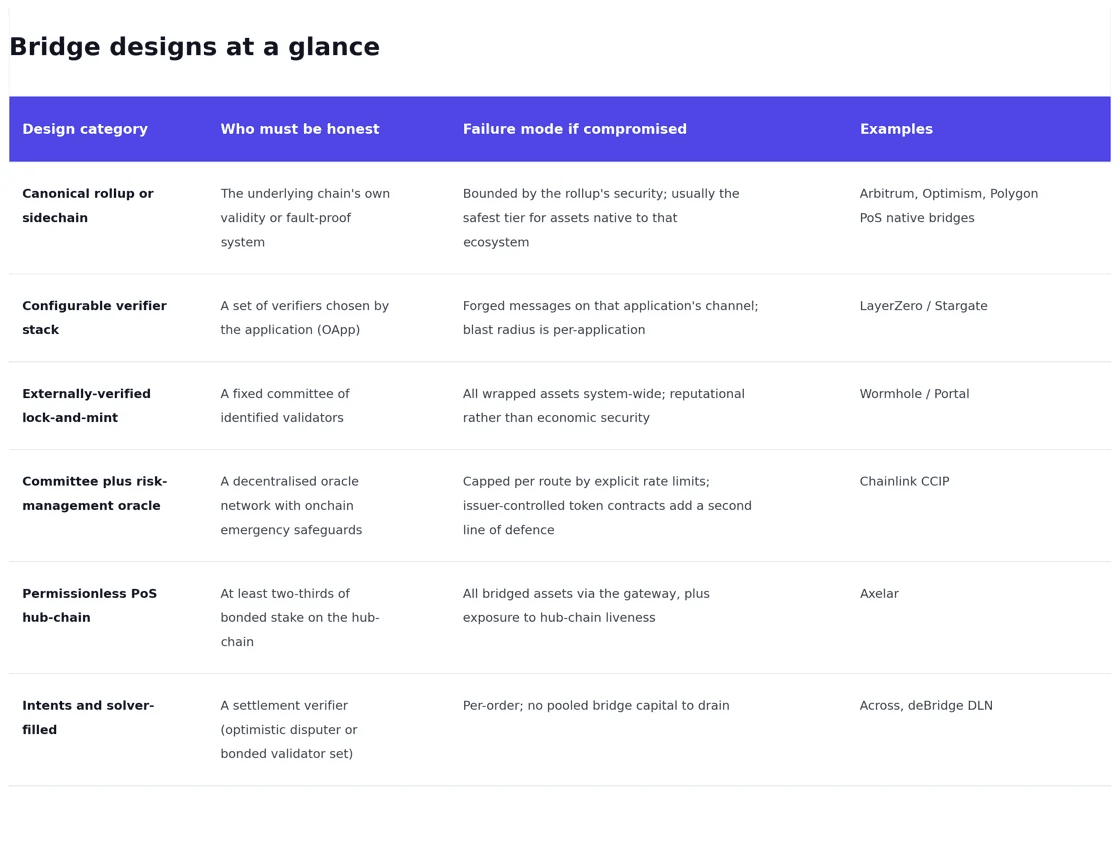

Every bridge has the same basic shape. An action on the source chain (a deposit, a burn, a signed intent) is observed and attested to by some verifier, and that attestation authorises a corresponding action on the destination chain (a mint, a release, a fill). The verifier is the load-bearing component. The categories below differ in who plays that role and what backs their attestation:

Canonical rollup or sidechain bridges: inherit verification from the underlying chain's own validity or fault-proof system.

Configurable verifier stacks delegate the choice of attesters to the application itself, which selects an independent set of verifiers and a signing threshold.

Externally-verified lock-and-mint bridges rely on a fixed committee of identified validators who sign a portable attestation accepted across all connected chains.

Committee plus risk-management designs combine a decentralised oracle network with onchain emergency safeguards and per-route rate limits.

Permissionless proof-of-stake hub-chains route cross-chain messages through validators bonded by economic stake, with threshold signatures controlling the gateway contracts.

Intents and solver-filled designs remove pooled bridge capital entirely, with solvers fronting funds on the destination chain and reclaiming through a dispute or attestation layer.

The historical pattern is consistent. The largest bridge failures (Ronin at $625M, Multichain at over $130M, Harmony Horizon at $100M, Orbit Chain at $82M) have all involved small fixed key-holder sets where a handful of compromised signers controlled hundreds of millions in assets. Designs that distribute trust across larger sets, that bond verifiers economically, or that avoid pooled bridge capital altogether have a cleaner track record, though some have shorter operating histories. The lesson is that the design determines the failure mode. No category is universally safe.

Identifying whether an asset is native to the chain or bridged onto it is a prerequisite for understanding its risk profile. A wrapped or bridged token carries the trust assumptions, blast radius, and governance of the bridge that issued it, regardless of how the symbol displays. The design category determines who must be honest, who can halt the bridge, and the size of a potential failure. Each model concentrates these properties differently, and the choice of bridge is therefore part of the asset's risk rather than separate from it.