The launch, which occurred on March 12, 2026, saw the fund debut with $107 million in assets and $15.5 million in first-day trading volume. While this volume lagged behind some of the more aggressive Solana-based staking products seen last year, market analysts have characterized the start as very solid for an institutional-grade product targeting a more conservative, long-term investor base. The $15M traded in the first day put them in the second spot for the most traded ETH ETF yesterday, and its over $100M inflows are above the weekly inflows of all other ETH ETFs combined.

Source: SoSoValue

To understand the mechanics, it is important to distinguish ETHB from existing spot products like ETHA:

Staking Ratio: The fund mandates that between 70% and 95% of its ETH holdings are staked at any given time.

Liquidity Management: The remaining 5% — 30% of ETH is held as a liquid buffer to accommodate daily redemptions without triggering the multi-day unstaking latency inherent to the Ethereum protocol.

Fee Structure: BlackRock has implemented a 0.25% sponsor fee, aggressively undercut to 0.12% for the first $2.5 billion in assets.

The core value proposition of ETHB is the distribution of monthly cash rewards, a departure from some other providers who prefer to reinvest rewards into the underlying asset. By passing 82% of gross staking rewards to shareholders, the fund creates a synthetic income-generating asset within a tax-advantaged (or at least brokerage-accessible) wrapper. The remaining 18% of rewards covers the service costs, including validator management by institutional-grade providers like Figment, Galaxy Digital, and Attestant, as well as custody via Coinbase.

From a quantitative perspective, the effective net yield for investors is the primary metric to monitor. With the current Ethereum network staking yield at approximately 2.5%, and after accounting for the fund’s 82% reward distribution policy and applicable sponsor fees, investors can expect a net annualized yield of roughly 1.75% to 1.95%. While this yield trails the 2.5% available via direct, permissionless on-chain staking, the institutional convenience, which removes the operational overhead of validator maintenance, private key management, and slashing liability, is the clear “convenience premium” being priced in by the market.

Disclaimer: The information provided in this newsletter is for educational and informational purposes only and does not constitute financial, investment, or legal advice.

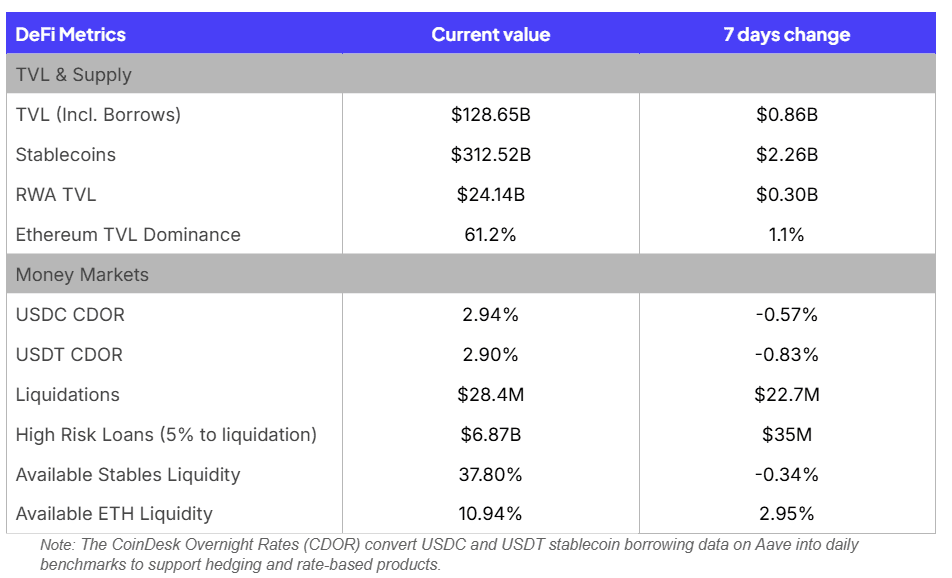

Key Weekly DeFi Metrics

Key takeaways for this week:

$2B+ increase in Stablecoin supply and market volatility have led to a low borrow rate environment

CDOR for both USDC and USDT have dropped substantially

Available ETH Liquidity is now near 11% and continues to grow, suggesting a stabilization of the ETH lending market

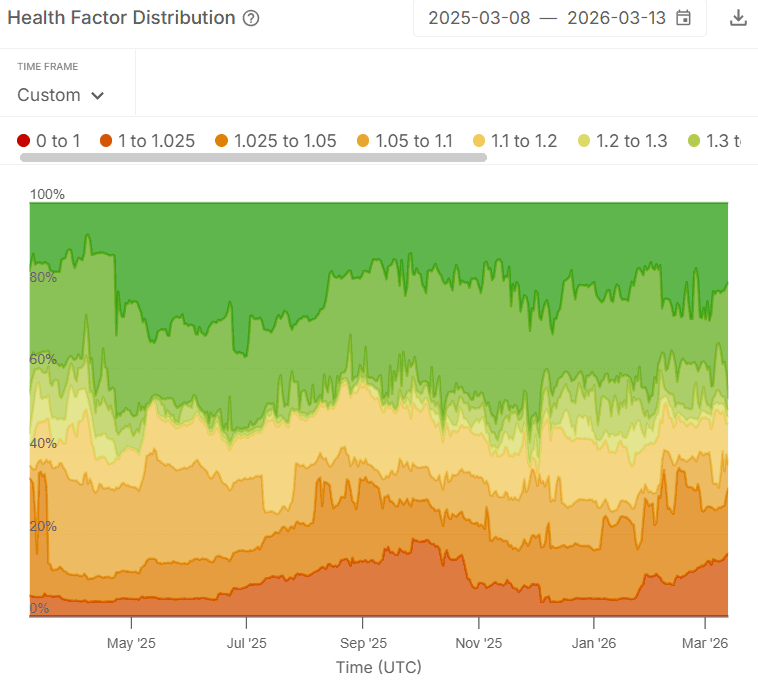

Borrower Risk Guide: Understanding On-chain Liquidations

Borrowers in decentralized finance must manage risk through the Liquidation Loan-to-Value (LLTV) threshold. This limit defines the exact point where a protocol seizes collateral to repay debt. A Health Factor monitors this safety margin in real time. If the value drops below 1.0, the borrower loses control of their assets.

Source: Sentora Risk Radar

The Health Factor serves as a numerical representation of position safety. It is functionally defined by the following ratio:

The LLTV is a protocol-defined constant that reflects the specific risk profile of a market pair. High-liquidity assets like ETH or BTC typically permit higher LLTVs, whereas more volatile or “long-tail” assets require lower thresholds to protect lenders. By incorporating the LLTV directly into the numerator, the Health Factor acts as a normalized safety metric across different markets. A value of 1.0 always represents the critical threshold for liquidation regardless of the underlying asset’s specific volatility settings.

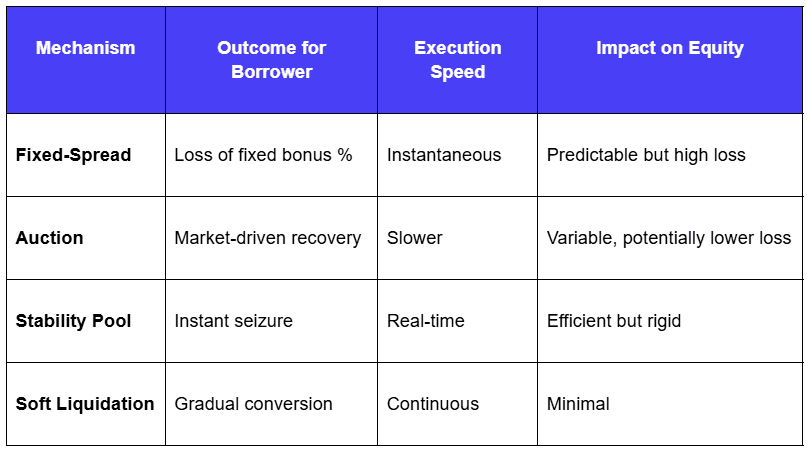

Liquidations incur costs through the Liquidation Incentive Factor (LIF), a bonus paid to third-party liquidators directly from the borrower’s equity. While higher incentives ensure protocol solvency, they increase the borrower’s realized loss. The protocol architecture, using mechanisms like fixed-spread models, competitive auctions, or gradual soft liquidations, determines how much equity is preserved during this process.

Liquidations can occur within the same block that a position becomes eligible. This speed leaves no room for manual intervention after a breach. Users with high leverage must monitor their positions constantly. A private margin call system or automated alert is essential to avoid permanent loss.

Prudent position management begins with a rigorous audit of protocol parameters. Borrowers must look beyond simple yield rates to understand the mechanical risks of their debt. High-quality data prevents unexpected losses during market turbulence.

Verify oracle resilience and the historical frequency of price spikes.

Review the close factor to understand if the protocol liquidates the entire debt or just a portion.

Calculate the effective liquidation price after accounting for the bonus and potential slippage.

Maintain a liquidation buffer large enough to withstand transient market volatility.