The Window Is Open

Something shifted in 2025. The GENIUS Act was signed into law in July, giving the United States its first comprehensive federal framework for stablecoins. The Senate passed it 68 to 30. The House followed at 308 to 122. Bipartisan. Decisive. And for fintechs and neobanks, it changed the math on everything.

Stablecoins are no longer experimental. The total market cap crossed $310 billion at the start of 2026. Transaction volumes hit $33 trillion in 2025, up 72% year over year. That’s more than 20x PayPal’s annual volume, approaching Visa’s global throughput. Stablecoin issuers now collectively hold more U.S. Treasuries than most sovereign nations. This is not a crypto niche. This is financial infrastructure.

The regulatory rails are laid. The technology is institutional-grade. And the fintechs that move now have a window to build something that legacy banking simply cannot replicate.

What Traditional Rails Cannot Do

If you run a fintech today, you already know the constraints. Settlement takes days. Fee structures are opaque. Your product roadmap is bottlenecked by third-party infrastructure you don’t control. You plug into banks that own proprietary, closed-source financial plumbing, and every integration adds cost, latency, and dependency. The result is a business where the most innovative thing you can ship is a better interface on top of someone else’s system.

The yields you can offer reflect this. A typical high-yield savings product delivers somewhere around 4 to 5%. That’s competitive by legacy standards. But it’s also a ceiling, and it’s hard to break when your infrastructure is renting access to the same banking system every competitor uses.

On-chain financial infrastructure offers the opposite. Open. Programmable. Composable. Settlement in seconds, not days. DeFi has grown into a $100+ billion ecosystem spanning lending, liquidity provision, staking, and structured strategies across dozens of protocols and chains. Base lending yields on stablecoins already compete with treasuries. But the real opportunity is in what you can build on top of that base layer. Specialized players that run complex, multi-protocol strategies, combining lending, liquidity, staking, and risk hedging across primitives, are generating materially higher yields while maintaining institutional, and 24/7 automated risk controls. That’s the kind of return profile a fintech can surface to users and no savings account on legacy rails can compete with.

And because the infrastructure is open source, fintechs that build on it own more of their stack. The cost of operating on these rails is materially lower than traditional infrastructure, because public blockchains handle the heavy lifting on settlement, clearing, and transaction processing. For a fintech, that translates directly into better unit economics and more room to differentiate on product.

Your Users Don’t Need to Know It’s DeFi

Here’s the part most people get wrong. Adopting on-chain infrastructure does not mean asking your customers to download a crypto wallet or manage seed phrases. The most powerful implementations are invisible. Your users never see the blockchain. They see your product, your brand, your experience. The on-chain layer is just the engine underneath.

The pattern is already playing out across finance. Coinbase is originating hundreds of millions in on-chain loans through a familiar app interface. BlackRock and JPMorgan are tokenizing assets on public chains. Robinhood acquired WonderFi and is building crypto infrastructure into its core product. These are not experiments. These are strategic bets by some of the largest financial platforms in the world, and they all point in the same direction: on-chain infrastructure as the backend for consumer-facing financial products.

At Sentora, this is exactly the model we’ve been building. A consumer-facing platform handles the user relationship, the interface, and the regulatory wrapper. Sentora handles strategy, risk, and yield optimization behind the scenes. Both sides do what they do best. The user gets a seamless experience with no crypto complexity. The fintech gets better economics and a product its competitors can’t easily replicate.

Proof of Concept at Scale: Kraken Earn

In January 2026, Kraken launched DeFi Earn, the most ambitious on-chain yield integration ever shipped by a major exchange. Available across 48 U.S. states, Canada, and the European Economic Area, the product lets users earn up to 8% APY on stablecoins directly within the Kraken app. No wallet setup. No manual transaction signing. No bridging complexity. Users deposit, select a strategy, and start earning.

Sentora powers the yield intelligence and risk management layer. When a user deposits into a Kraken DeFi Earn vault, our Smart Yields platform dynamically allocates capital across established lending protocols based on real-time economic signals. Yields are derived from genuine borrower demand. Not token incentives. Not subsidies. Real economic activity.

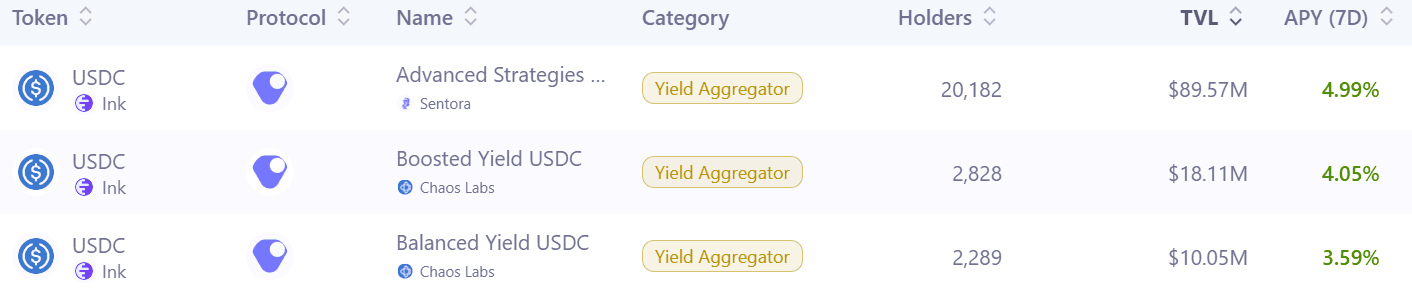

The architecture tells the story. Kraken provides the distribution and the millions of users. Veda Labs provides the vault infrastructure on Kraken’s Ink network. Sentora provides the strategy engine and risk controls. Each layer does what it does best, and the result is a product that delivers institutional-grade on-chain yield through an interface that feels like any other fintech feature. At the time of writing, the Kraken DeFi Earn feature has alroady surpassed $115 million in total deposits, from 25,000 unique users.

Kraken is crypto-native. But the architecture is entirely platform-agnostic. Any fintech with a user base and a product team can ship the exact same kind of Earn experience.

Why Neobanks Are the Next Frontier

The biggest emerging trend we’re tracking is neobanks building on stablecoin rails and on-chain yield to replace traditional banking supported by fiat and treasury yields. These are not crypto products for crypto people. These are financial products for everyone, powered by infrastructure that happens to run on-chain.

The business case is straightforward. A neobank that integrates on-chain yield can offer returns that beat any savings account on the market. It can do so with full control over the product experience, building on open infrastructure rather than renting closed rails. It can differentiate from every competitor still stuck on legacy systems. And the margins are better, because the cost structure of on-chain infrastructure is fundamentally different from the cost of maintaining correspondent banking relationships.

This is not speculation. At Sentora, we’re already in late-stage conversations with some of the largest consumer finance brands globally, including major payment platforms, leading neobanks, and fintechs with tens of millions of users. Projects with infrastructure partners like Fireblocks and Apollo have already launched. The question is no longer whether fintechs will adopt on-chain infrastructure for yield. It’s who moves first.

The Clock Is Ticking

Regulatory clarity arrived. Stablecoins are mainstream. On-chain yield products are live at consumer scale. The fintechs and neobanks that move now will ship products their competitors cannot match, on rails that give them a level of control no traditional banking partnership offers. The ones that wait will find the market has moved and the first movers have locked in the users.

This has happened before. The companies that moved early on mobile banking, on peer-to-peer payments, on embedded finance, they defined their categories. The same dynamic is playing out now with on-chain yield. The rails are ready. The question is whether you’ll build on them.

Sentora helps fintechs and neobanks integrate institutional-grade on-chain yield into their products. To explore what a pilot integration looks like, reach out here.