JPMorgan has officially bridged the gap between “Digital Gold” and “Wholesale Credit.” The activation of direct BTC and ETH collateralization allows institutional giants to finally turn their dormant holdings into immediate USD liquidity without selling a single satoshi. Operating through the Kinexys (formerly Onyx) digital financing platform, the bank now allows institutional clients like hedge funds and corporate treasuries to pledge BTC and ETH for USD-denominated liquidity. Unlike previous years where only ETF-wrapped products were supported, this move enables borrowers to leverage their direct on-chain holdings without triggering the capital gains taxes associated with liquidation.

The quantitative framework for these loans is defined by a rigorous risk-weighted haircut model. Under the current policy, JPMorgan applies a 30% to 50% haircut on BTC and ETH, effectively setting the maximum Loan-to-Value (LTV) ratio at 50% to 70% depending on 90-day volatility metrics. This structure is designed to buffer against the “cascade risk” inherent in crypto markets, where a 15% intraday drop could otherwise trigger systemic liquidations. By treating BTC and ETH as Tier-1 collateral, JPMorgan is effectively putting them on the same playing field as high-quality corporate bonds.

Tri-Party Custody: Assets are not held on the bank’s balance sheet but are secured via qualified third-party custodians like Coinbase Custody and Anchorage Digital. This ensures that the bank facilitates the credit while the assets remain in high-security, audit-ready vaults.

Atomic Settlement: By utilizing the Kinexys blockchain, JPMorgan has reduced the time to move collateral from T+2 days to under 120 seconds. This allows for real-time margin adjustments and prevents the “lag” that often causes over-collateralization in traditional banking.

Tax-Efficiency: Because the institution is borrowing against the asset rather than selling it, they avoid triggering capital gains taxes. This makes crypto-backed credit the most tax-efficient way for “whales” to access their wealth.

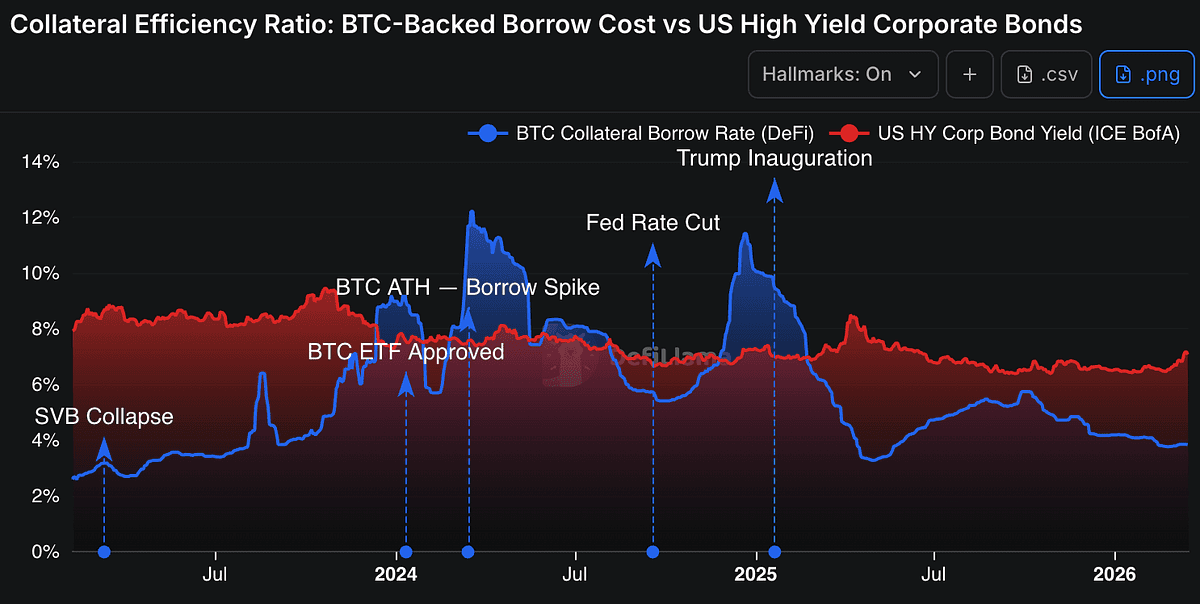

The chart clearly shows that BTC collateralized borrowing rates are consistently trending below US high-yield corporate bond yields, even though BTC remains a more volatile asset. While there are occasional spikes during periods of market stress, reflecting short-term liquidity demand and volatility shocks, the overall cost of borrowing against BTC remains structurally lower. This suggests that the market is increasingly valuing BTC’s deep liquidity and global trading nature over its volatility, allowing it to function as efficient collateral. JPMorgan’s activation reinforces the trend by enabling institutions to unlock USD liquidity against BTC and ETH at lower rates, improving capital efficiency while accepting manageable volatility driven fluctuations.

The broader implication for DeFi is the emergence of a hybrid credit market. By recognizing BTC and ETH as “pristine collateral” alongside gold and Treasuries, JPMorgan is effectively lowering the cost of capital across the system. This brings in significant liquidity, but it also concentrates risk, since these structures rely on a small set of regulated custodians to hold assets. More broadly, this marks a shift in how balance sheets are used. Assets are no longer just held for exposure, they are actively used to generate liquidity and improve capital efficiency.

Disclaimer: The information provided in this newsletter is for educational and informational purposes only and does not constitute financial, investment, or legal advice.

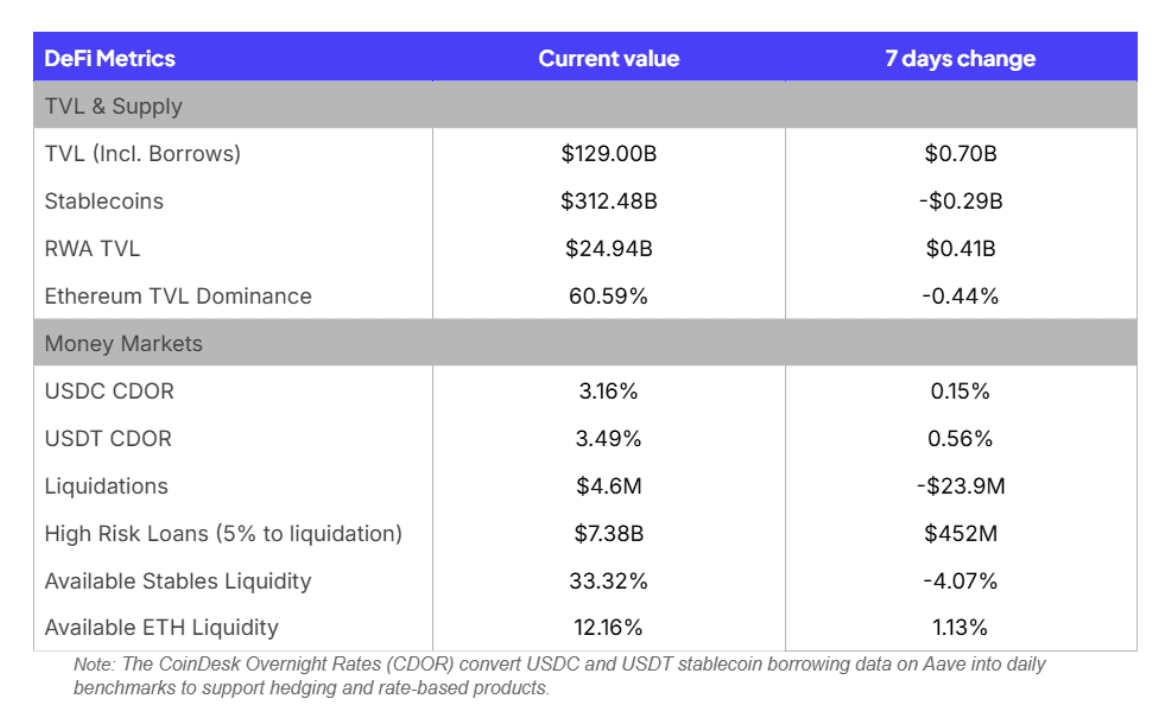

Key Weekly DeFi Metrics

Key takeaways for this week:

$2B+ increase in Stablecoin supply and market volatility have led to a low borrow rate environment

CDOR for both USDC and USDT have dropped substantially

Available ETH Liquidity is now near 11% and continues to grow, suggesting a stabilization of the ETH lending market

Beyond the APY: The “Know Your Vault” Framework

Current DeFi yields on blue-chip assets like ETH and USDC are compressing. This environment forces DeFi vaults into increasingly complex territory to maintain higher returns. Managers are moving up the risk curve. They employ strategies that appear market-neutral but remain structurally fragile. Success requires a precise understanding of the underlying portfolio and the liquidity profile of the traded assets.

An example of a structurally fragile trade is the LIT basis trade which has become a popular strategy for DeFi vaults looking to support higher yields. This strategy combines LIT staking, perpetual funding rates, and platform-specific boosts into a single carry trade. While the 16.7% aggregate yield is attractive, the portfolio composition reveals specific structural risks.

The LIT market currently has $70M in open interest against a circulating market cap of $300M. Since 23% of the liquid supply is tied up in derivatives and spot depth is thin, the strategy is could be exposed to liquidity manipulation. Furthermore, the 3-day unstaking period for LIT creates a hedge gap. If a short position is force-closed during a volatility spike, the vault’s trade can lose its delta-neutrality and be exposed to price risks.

Centralized exchanges and prime brokers act as the trust layer for millions of users. To provide stable returns, many entities are adopting a Know Your Vault (KYV) approach. This involves auditing logic and monitoring collateralization to ensure market-neutral positions do not become directionally exposed.

When evaluating the risk curve of any strategy, institutions should focus on these critical factors:

Capacity vs. Liquidity: Ensure vaults are actively monitoring their size and capacity constraints against the liquidity requirements to exit trades with low impact.

Operational Synchronicity: Verify that entry and exit mechanisms for all legs occur in the same timeframe to prevent unhedged risk windows.

Yield Attribution: Distinguish between organic fees and dilutive token incentives. Reliance on dilutive rewards increases the risk of rapid capital flight.