An estimated $124 trillion will transfer from the Baby Boomer and Silent generations to Millennials and Gen Z by 2048, with $38.3 trillion moving in the next decade alone, according to Cerulli Associates. The key question is not where this money will go, but what recipients will expect it to do while it remains unspent.

They will not open a savings account.

The Tax Nobody Talks About

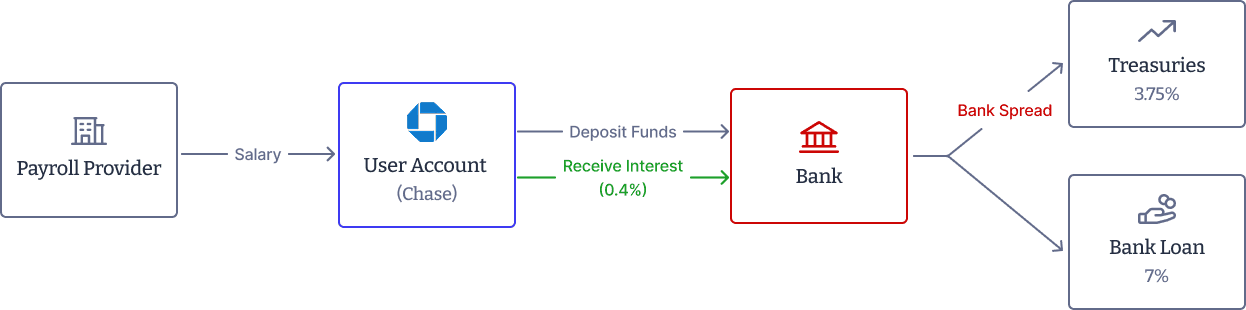

Checking Account - Current Model

User deposits funds from payroll provider into a traditional checking account

User receives a small fraction of the treasury rate (~0.4%)

The bank lends user funds to earn a large spread (Net Interest Margin)

Access to money is on a delayed timeline, though protected by FDIC insurance

Checking Account - Proposed Model

Self-Custody: Deposits from Payroll flow into a self-custodied stablecoin wallet.

Maximized Yield: User earns 90% of generated yield (compared to 10% in current model).

Instant Access: Funds are available instantaneously with flexible risk-managed Earn options.

Assurance: Optional insured vaults are available for a lower, protected yield.

The average US savings account paid 0.4% APY in 2025. The Federal funds rate sat at 4.25-4.50%. The Federal Reserve paid banks $176 billion in interest on reserves that year, money generated by household deposits, redirected to institutions. A 27-year-old with $20,000 in a savings account earned $80. The same $20,000 in a yield-bearing stablecoin strategy, deploying reserves into short-term US Treasuries and returning the proceeds to the holder, returned $800 to $1,600 at the 4-8% rates available in 2025 and 2026.

This is not a crypto argument; it is a matter of arithmetic. A stablecoin is a digital dollar that maintains its value and is not subject to speculation. It simply earns the yield that should have accrued to the dollar, rather than transferring it to the bank.

The market already knows this. Stablecoin market capitalization exceeded $315 billion in 2026. Transaction volume reached $33 trillion in 2025, up 72% year-over-year. Visa's stablecoin-linked card spend hit a $3.5 billion annualized run rate in Q4 2025, up 460% yoy. Stripe, Siemens, and Fifth Third Bank are routing treasury operations on-chain. Institutional stablecoin strategies grew from $9.5 billion to over $20 billion in assets during 2025 alone.

The shift from bank deposits to on-chain dollars is already underway.

The Paycheck That Shouldn't Wait

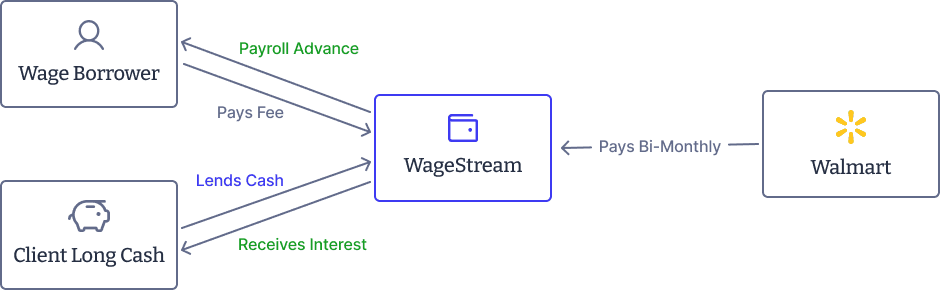

Earned Wage Access - Current Model

Critical Inefficiency: Bank fees are charged to both parties, primarily benefiting the financial institution.

Earned Wage Access - Proposed Model

Borrowing Costs: WageStream reduces costs by 30–40% by bypassing traditional banking layers.

Yield Product: Increases user retention and creates a new income stream from the borrowing/lending spread.

Direct Value: Interest flows directly from the platform to the Client instead of staying with the bank.

For 78% of Americans living paycheck to paycheck, the two-week payroll cycle is not merely a scheduling convention; it is a structural gap that the payday lending industry exploits. In 2022,

this industry collected $2.4 billion in fees from borrowers seeking access to wages they had already earned. The average annualized rate is 391%, and in states without caps, it exceeds 600%.

On-chain stablecoin payroll addresses this gap. Settlement occurs in under three seconds. Transferring $144, which represents a typical eight-hour shift at $18 per hour, costs only a fraction of a cent. There is no batch queue, no ACH processing window, and no bank earning float on another person's wages.

A key engineering challenge is that employers cannot immediately restructure payroll cycles. The solution is a short-duration on-chain bridge: a lending protocol advances earned wages to the worker's wallet, uses the employer's bi-weekly payroll as the repayment mechanism, and charges a small access fee. For the worker, this process is indistinguishable from real-time payment. For the employer, the payroll cycle remains unchanged.

The Virtual Credit Union

Onchain Credit Union - Stage 1

Direct Peer-to-Peer Value

By cutting out the bank, the real borrow rate is passed directly to the lender. Both parties benefit: lenders earn higher yields while borrowers enjoy reduced costs.

Onchain Credit Union - Stage 2

Blockchain Visibility: A credit risk profile can be created since all income and payments are visible on-chain.

Credit Scoring: Over time, this data provides a credit score for individuals, opening the path to unsecured credit.

Financial Inclusion: Allows lower-income users to access financial products they are currently excluded from.

The bridge loan that funds the payroll advance does not need to originate from a bank. It can come from other members of the same network—individuals with excess savings who prefer to earn 4 to 5% by funding real needs rather than 0.4% in a savings account.

This is the credit union model: members deposit funds for member lending, and surplus returns to members instead of bank shareholders. The on-chain version operates similarly on programmable infrastructure. Users deposit stablecoins into an earn vault, which deploys them as short-duration advances to workers accessing earned wages early. Workers pay an access fee, and the protocol returns most of that fee to vault depositors as yield.

The risk profile is structurally attractive. Wages are among the most reliable repayment sources in consumer finance. The bi-weekly payroll cycle provides a fixed settlement date, making loan duration predictable and default rates low. As on-chain credit histories accumulate through consistent repayment, this payroll bridge product can serve as the foundation for broader consumer credit, with rates reflecting a much lower cost base compared to traditional lenders.

There is precedent for this model. Morpho, integrated into Coinbase's Bitcoin lending platform in 2025 and embedded in the World App for over two million users, demonstrates on-chain member-funded lending at scale. The EWA vault is a simpler, more focused, lower-risk application of the same architecture, anchored in real wages, repaid through payroll, and governed by transparent smart contracts instead of institutional discretion.

The Fintech Balance Sheet Problem

There is a less visible aspect of this structural problem, which affects the companies aiming to serve these individuals.

Every major payment provider, remittance company, and neobank maintains an operational balance sheet. Prefunding accounts, settlement reserves, and liquidity buffers are essential working capital for the modern financial system, but they are costly. For example, a payment company borrowing $100 million at SOFR plus 150 basis points, a typical spread for an investment-grade fintech on a revolving credit facility, paid approximately 6.9 to 7.2% annually in 2025 and 2026 just to maintain necessary liquidity. This is not a cost of growth; it is a cost of doing business.

The impact is clear: only 15% of neobanks were profitable in 2026. Fintech valuations stabilized around 4.2 times revenue in Q4 2025, with lending and balance-sheet-heavy companies at 2.5 times, while capital-light platforms reached 17 times. The difference between a fintech that borrows from banks and one that does not is significant; it determines whether a company can raise its next funding round. For early-stage startups, the challenge is greater: a seed-stage payments company cannot access institutional revolving credit, limiting its scale to what its equity can support. As a result, it grows more slowly than better-capitalized competitors, even if its product is superior.

A user Earn vault addresses this challenge and benefits all parties involved.

A remittance company borrowing $50 million from a bank at 6.9% pays $3.45 million per year in interest. If it instead funds the same $50 million through a stablecoin earn vault, paying depositors 4.5% APY, it pays $2.25 million per year, saving $1.2 million annually. This approach also provides users with a yield product that banks do not offer. Net interest expense decreases, user retention improves, and the bank earns nothing. If the vault is structured as an off-balance-sheet special purpose vehicle using standard securitization architecture applied to stablecoins, the fintech's formal debt obligations decrease, compressing leverage ratios and improving equity valuation at any revenue multiple.

For a startup unable to access a credit facility, the earn vault is not merely a balance sheet optimization; it becomes the balance sheet. It is funded by users who already trust the platform, pays yield that would otherwise go to the bank, and is governed by on-chain rules instead of a traditional lending agreement.

The Neobank That Does All of This - Built on Sentora

Each of the products described above the yield-bearing savings account, real-time payroll advance, community earn vault, and corporate treasury alternative-represents a standalone innovation. Together, they form a single product: a stablecoin-native neobank that offers all the services of a traditional bank at a lower cost, with economic benefits flowing to members instead of shareholders.

This bank does not need to be built from the ground up. Sentora has already developed the infrastructure stack required to make it possible.

Sentora's platform operates over 1,000 risk models across more than 40 DeFi protocols and 12 blockchains, with over $3 billion in capital deployed. Its Advanced Strategy Vault, which powered Kraken's DeFi earn program for 30,000 participants and $110 million in assets, serves as the yield engine. The platform's risk and collateral monitoring infrastructure provides the compliance layer, making each product auditable and suitable for board reporting. Firelight.finance, incubated by Sentora, is the insurance protocol that backstops covered vault failures. This is the final component that has previously limited institutional adoption of on-chain earn products at scale.

A neobank built on Sentora's stack can offer, from day one:

Yield on deposits

User stablecoin balances are deployed into Sentora yield vaults, earning 4 to 8% APY instead of 0.4% in a bank account. No new infrastructure is required; this is Sentora's core product.

Real-time earned wage access

On-chain payroll advances bridge the worker's earned wages to the employer's bi-weekly settlement cycle, with fees annualizing below 36%, which is five times less than the average payday loan. The Earn Vault funds the advance, risk models determine pricing, and Firelight covers tail risk.

Community lending

Users with excess balances lend to others needing short-term liquidity through the same vault infrastructure, earning yield that previously went to the bank. This is the credit union model on-chain.

Treasury vaults for fintech partners

Payment companies, remittance firms, and neobanks can borrow operational liquidity from the platform's user base instead of bank revolving credit facilities, paying 4 to 5% to depositors rather than 6 to 9% to institutional lenders. This reduces on-balance-sheet debt and improves equity valuation.

Firelight insurance

Every product in the stack is covered by a programmable, capital-backed insurance protocol, which has undergone three independent security audits including OpenZeppelin. This ensures that institutions, employers, and individual users can deploy capital with confidence that covered-event losses are backstopped.

The GENIUS Act provides the regulatory framework, and the necessary infrastructure is in place. The only remaining requirement is an operator with the relationships, risk expertise, and platform to integrate these components.

Sentora was designed to fulfill this role.

The one who created the sword got rich. Those who learned to use the sword built an empire.

- ADM

Sentora is the risk infrastructure layer for institutional DeFi. Founded in 2025, Sentora operates 1,000+ risk models across 40+ DeFi protocols and 12 blockchains, with over $3B in capital deployed through its platform technology. Firelight.finance, incubated by Sentora, provides the first model-driven, programmable insurance protocol for DeFi vaults and strategies. Learn more at sentora.com and firelight.finance.