Institutional allocators want staking yield, capital efficiency, and a reliable exit from the same ETH position. Liquid restaking tokens deliver the yield and efficiency by adding a reward layer on top of base staking, and they widen the risk surface, because the token now helps secure services beyond Ethereum. weETH sits at the center of that tradeoff. It is the largest liquid restaking token in DeFi, issued by EtherFi, and Sentora has worked alongside EtherFi for more than two years deploying capital into strategies built around it. This piece covers what weETH is, how EtherFi became a blue-chip issuer, and how Sentora uses the asset across its strategies and curated markets.

What weETH is

weETH is a liquid restaking token. It represents staked ETH that is also restaked through EigenLayer, held as a liquid, composable token that works across DeFi.

It differs from plain ETH and a traditional liquid staking token in one way. Plain ETH carries no yield. An LST such as stETH adds Ethereum staking yield. weETH goes further: its staked ETH is also restaked, helping secure additional services and accruing their rewards on top of base staking. That extra layer raises the yield weETH can generate and adds a matching layer of risk, since the token is now exposed to the services it secures and their slashing conditions. It is a higher-yielding, more complex sibling to a standard LST.

How EtherFi became a blue-chip LRT

EtherFi has built weETH into the reference asset for liquid restaking. Three components explain that position.

Yield generation. weETH captures two yield layers: Ethereum staking rewards and EigenLayer restaking rewards from the services its operators secure. That gives it a structurally higher yield than a single-layer LST, the core reason allocators hold it.

DeFi composability. weETH is integrated across the major money markets (Aave, Morpho, Euler, Spark), leading DEXs, and yield protocols, and runs on Ethereum mainnet alongside L2s including Arbitrum, Base, Optimism, Scroll, Linea, and Blast. That reach gives allocators deep composability and multiple venues to deploy and manage exposure.

Market adoption. EtherFi is the largest liquid restaking protocol, with combined TVL near $3.93B in mid-2026 (DefiLlama), and weETH leads the LRT category by market share.

EtherFi's standing also rests on its security foundations. The protocol is non-custodial, so stakers keep control of their withdrawal credentials. Its contracts carry a public audit history across firms including CertiK, Zellic, Nethermind, and Certora, backed by an active bug bounty. These are the structural checks an allocator runs before treating an asset as collateral.

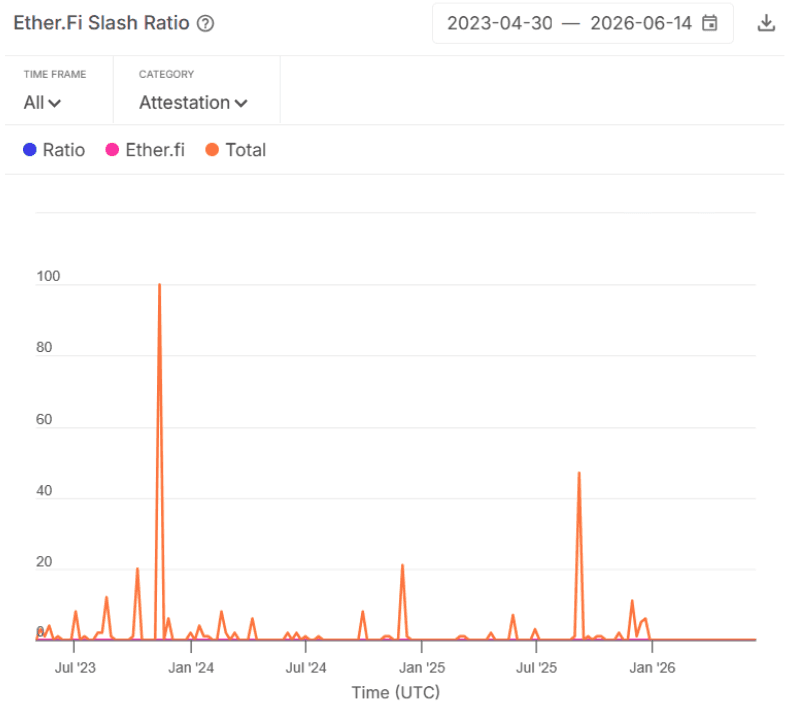

Validator quality is another important signal, and one of the few an allocator can measure directly. Slashing penalizes validators for faults such as missed or incorrect attestations, and on EigenLayer it became a live risk in April 2025. The record below tracks slashing across EtherFi's validator set against the broader network over more than three years.

Source: Sentora Risk Radar

EtherFi's validator set records no attestation slashing across the full period, even as the broader set spikes periodically. A clean record over multiple years reflects disciplined operator selection and node management, and it protects collateral directly, since slashing losses are socialized across depositors. That mix of scale, integration, and operational discipline earns weETH its blue-chip standing.

How Sentora uses weETH

Sentora works with weETH in two ways: inside the strategies it manages, and as collateral in the lending markets it curates.

In strategies

Sentora's relationship with EtherFi began more than two years ago, as strategy curator and deployer for the launch of EtherFi's liquid USD vault, designing the DeFi strategies and deploying capital through its risk-monitoring smart contracts from within the vault. Sentora has since taken similar roles for EtherFi's liquid ETH, BTC, and Katana ETH vaults, and has securely deployed over $1B of capital into DeFi strategies for EtherFi.

weETH features regularly in Sentora's ETH-based strategies. Its yield-bearing nature lifts a strategy's return without a separate position, because the asset generates staking and restaking yield while it works. Two examples show how.

Leverage restaking. Sentora supplies weETH as collateral, borrows ETH against it, converts the borrowed ETH into more weETH, and repeats the loop. This amplifies exposure to weETH's staking and restaking yield. It is productive when that yield exceeds the cost of borrowing ETH, and Sentora manages the leverage to keep the position inside safe bounds.

ETH-based supervised loans. A supervised loan posts blue-chip collateral, borrows a productive asset at a rate below the expected strategy yield, and deploys the borrow into a higher-yielding secondary strategy. In its ETH-based form, the borrow goes into weETH, so the position captures staking and restaking yield on top of the carry between borrow cost and strategy return. This puts idle or low-yielding holdings to work while keeping exposure to the underlying asset.

In both, Sentora sizes exposure and leverage so a plausible impairment cannot derail the strategy, and builds each position with predefined unwind paths and tested tolerances for slippage and latency.

As collateral in curated markets

Sentora also includes weETH as collateral in the markets it curates on Morpho and Euler, for three reasons.

First, weETH is a higher yield-bearing ETH asset than plain ETH or a traditional LST, which makes it attractive collateral for borrowers running ETH strategies and supports sustainable market activity.

Second, the long partnership with EtherFi gives Sentora a strong understanding of the protocol's operational execution and security practices, which informs how it sets collateral parameters and caps.

Third, Sentora runs economic-risk monitoring tools, including its Risk Radar, to track the additional risks weETH carries as a restaked asset, and prices it on fundamental value rather than DEX market price to prevent liquidations from transient secondary-market moves.

Monitoring the risks

weETH earns its place only when the risk controls hold. Sentora monitors it continuously across several dimensions.

Liquidity. Sentora tracks weETH liquidity on two fronts. DEX liquidity sets how much weETH can be sold in the secondary market without significant slippage. Buffer liquidity, the unbonded ETH EtherFi holds to fill redemptions immediately, sets how much can be redeemed on demand. Together they cap how quickly a position can be reduced.

Duration risk. When buffer liquidity is exhausted, redemptions queue validator exits and settle over time rather than instantly. Sentora treats this latency as duration risk and monitors the exit queue, since a longer queue extends how long a position stays exposed before it can be fully unwound.

Restaking exposure. Through EigenLayer, weETH carries service-specific slashing and operator risk. Sentora tracks the services EtherFi's restaked capital secures and favors lower-risk, fee-generating ones.

Carry conditions. Leveraged strategies depend on staking yield staying above the ETH borrow cost. Sentora monitors that spread and adjusts leverage as it moves, so positions are not held in unfavorable conditions.

These controls follow a single principle that governs every Sentora allocation: return of capital comes before return on capital.

Where this goes

Restaking is maturing from an incentive-driven phase into a fee-bearing market, with weETH at the center. As the services securing restaked capital multiply and their slashing terms diverge, the gap between disciplined and undisciplined exposure will widen. weETH rewards allocators who price it on fundamentals, size it to real liquidity, and monitor the validator and restaking layers continuously. That framework, built over more than two years alongside EtherFi, is why weETH remains core to how Sentora allocates onchain capital.