This borrowing mechanism not only preserves upside potential in the underlying stocks but also presents a compelling use case for debt management. With approximately 55% of U.S. individuals holding more than $10,000 in equities still carrying credit card or student loan debt, this strategy offers a smarter way to tackle outstanding obligations. Let's break down why borrowing at 4-5% against tokenized shares is attractive compared to prevailing debt rates and how it can be used to pay down high-interest liabilities effectively.

The Rise of Tokenized Equities and Low-Cost Borrowing

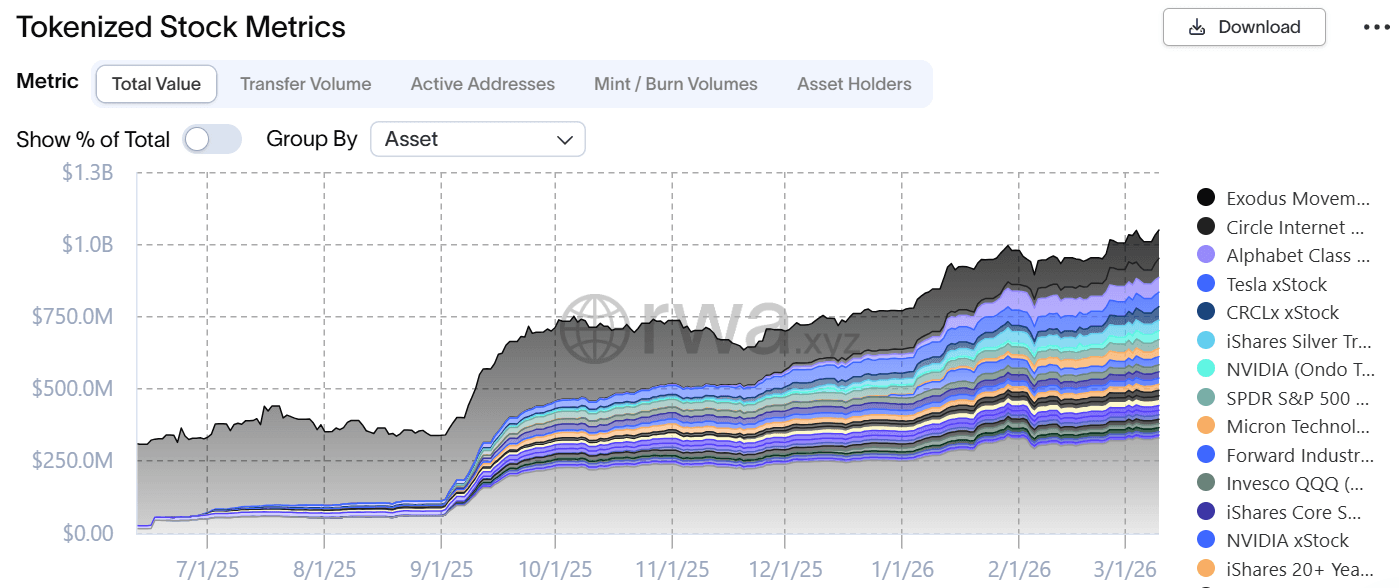

Tokenized equities represent real-world stocks wrapped in blockchain tokens, enabling seamless integration with decentralized finance (DeFi) ecosystems. As of March 2026, this market has ballooned to over $1 billion in value, marking a 271% year-over-year surge driven by institutional platforms like Ondo Finance and Securitize. The game-changer here is scaled borrowing against these assets.

Source: RWA.XYZ

Through solutions like STEY, users can deposit tokenized stocks as collateral and borrow stablecoins (such as PayPal's PYUSD) at loan-to-value (LTV) ratios up to 50%. For instance, if you hold $100,000 in tokenized NVDA shares, you could borrow up to $50,000 at an interest rate of 4-5%. This rate is derived from DeFi market dynamics, where borrowing costs are often lower than traditional loans due to efficient, automated protocols and competition among lenders. Unlike margin loans from brokers, which can carry rates of 7-12% or higher, DeFi borrowing leverages on-chain liquidity and hybrid liquidation mechanisms, bridging DeFi with traditional exchanges like NYSE for stability during market dips.

This low borrowing cost stands in stark contrast to common U.S. debt burdens. Credit card debt averages a punishing 22.3% interest rate, while student loans hover around 6.5%. For the millions of Americans juggling these debts alongside equity investments, tokenized borrowing isn't just convenient, it's a financial arbitrage opportunity.

The Core Use Case: Arbitrage Against Outstanding Debt

The primary appeal of borrowing against tokenized equities at 4-5% lies in its superiority over high-interest debt. Consider the average American investor. Data from the 2022 Survey of Consumer Finances reveals that over half of those with significant equity holdings (more than $10,000) still owe on credit cards or student loans. These debts erode wealth through compounding interest, often outpacing stock market returns. Tokenized borrowing flips the script by providing cheap capital to refinance or eliminate these liabilities.

Here's why it's attractive:

Interest Rate Savings: Borrowing at 4-5% to pay off 22.3% credit card debt creates an immediate 17-18% annual savings on the borrowed amount. For a $20,000 credit card balance, that's potentially $3,400-$3,600 in avoided interest per year. Even against student loans at 6.5%, the spread (1.5-2.5%) adds up over time, especially for larger balances.

Asset Retention and Upside Preservation: Selling stocks to pay debt triggers capital gains taxes (up to 20% federally, plus state taxes) and forfeits future growth. Tokenized borrowing lets you keep your shares, maintaining exposure to potential rallies. If your TSLA holdings appreciate 20% annually, you're effectively earning that return while using borrowed funds elsewhere, without the tax hit from sales.

Capital Efficiency for Retail Investors: Traditionally, borrowing against securities is a perk for high-net-worth individuals via prime brokerage accounts. Tokenized equities democratize this, offering self-custody and DeFi accessibility. Platforms like STEY abstract complexities, handling risk management and automation, so even non-experts can participate.

Tax-Efficient Pathways: As outlined in Sentora's vision, future enhancements could allow converting appreciated physical shares to tokenized versions without immediate capital gains taxes. Once tokenized, they become collateral for borrowing, amplifying liquidity without IRS penalties.

This use case is particularly timely amid rising DeFi adoption. With tokenized equities now collateral on protocols like Euler and Morpho, users gain access to vast stablecoin pools, turning illiquid stocks into dynamic financial tools.

How Borrowing Against Equity to Pay Down Debt Makes Sense: A Step-by-Step Rationale

Borrowing against tokenized equities to settle debt isn't about increasing leverage recklessly, it's about strategic refinancing. Here's how it works and why it pencils out:

Assess Your Debt Profile: Start with high-interest debts first. If you have $15,000 in credit card debt at 22.3%, the monthly interest alone could exceed $275. Student loans at 6.5% are less urgent but still burdensome, especially if variable rates rise.

Tokenize and Borrow: Convert or acquire tokenized versions of your stocks (e.g., via Ondo). Deposit them into a STEY vault on Euler. At a 50% LTV, $50,000 in tokenized TSLA yields $25,000 in PYUSD borrowable at 4-5%. The interest on this loan is roughly $83-$104 monthly, far below credit card costs.

Pay Down Debt: Use the borrowed stablecoins to immediately clear or reduce your outstanding balances. This halts high-interest accrual, freeing up cash flow. For example, paying off $25,000 in credit card debt saves over $4,500 in annual interest, while your loan costs just $1,000-$1,250.

Manage Risks and Repay: Monitor collateral health. Equity drops could trigger liquidations, but hybrid mechanisms (on-chain/off-chain sales) mitigate this. Repay the loan over time using income or yields from other investments. Future STEY vaults could even generate 3-5% APY on your collateralized stocks, offsetting borrow costs and turning the setup into a near-net-zero expense.

The math is clear. The interest differential creates a positive carry trade. You're essentially borrowing cheap to eliminate expensive debt, all while your equities continue to work for you. This mirrors institutional strategies but is now accessible to retail holders, potentially reshaping personal finance for the 55% of equity owners saddled with debt.

Of course, this isn't risk-free. Market volatility, liquidation thresholds, and stablecoin stability must be considered. Users should start small, diversify collateral, and consult financial advisors. Yet for those with stable income and growth-oriented portfolios, it's a powerful tool.

A Path to Financial Freedom

Tokenized equities are bridging TradFi and DeFi, unlocking trillions in potential value. By enabling borrowing at 4-5% against shares, platforms like Sentora's STEY empower investors to tackle debt head-on without sacrificing assets. In a world where credit card and student loan rates drain wealth, this use case offers tangible savings, tax advantages, and portfolio efficiency. As the market matures, with yield vaults and tax-efficient conversions on the horizon, borrowing against tokenized equities could become a staple strategy, democratizing liquidity and redefining how we manage debt and investments. For retail investors, the future isn't just tokenized, it's liberated.

~ADM