TL;DR:

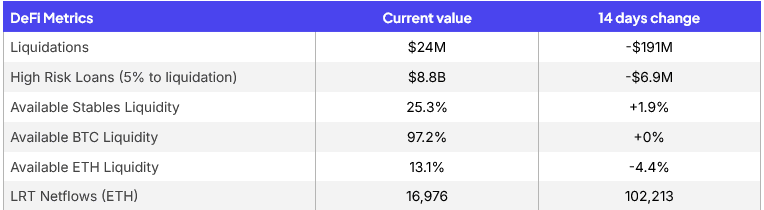

Liquidations over the past 14 days totaled $24M, a reversion to the mean after the liquidation spike post flash crash

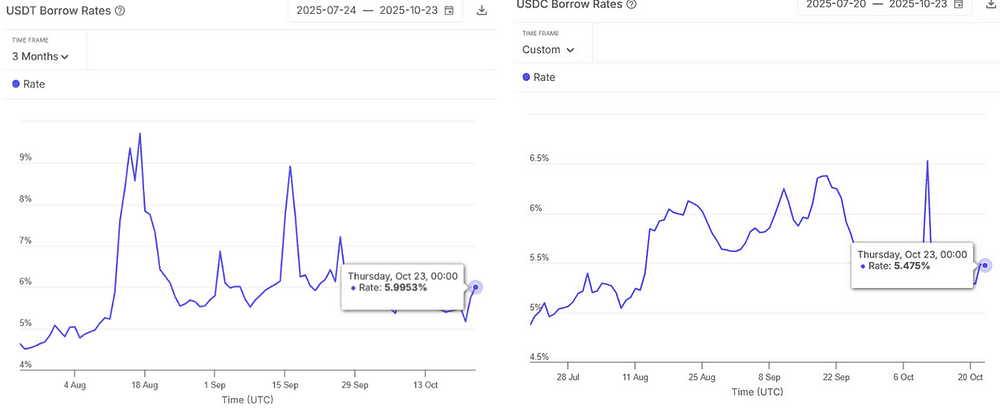

On Aave, USDT/USDC borrow rates exceed sUSDe yield by ~2.0%/1.5%, making carry negative.

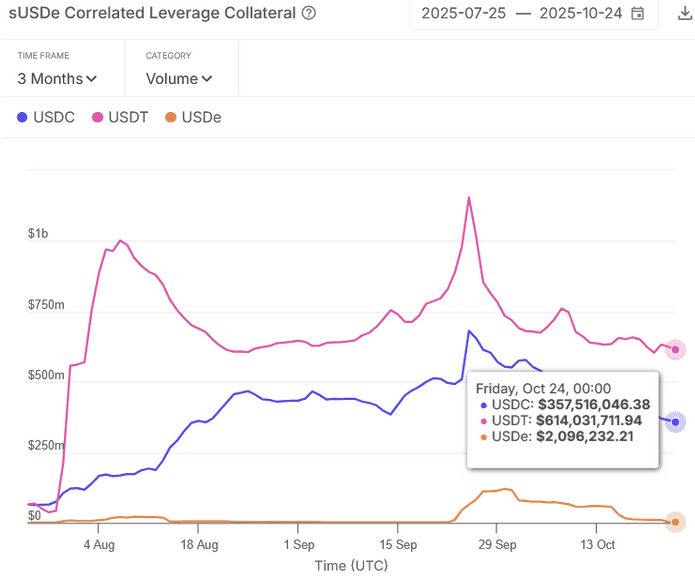

About $1B in sUSDe‑linked leverage may de-lever if negative carry persists.

ETHZilla will fund a $40M buyback by selling ETH (~0.085% of supply), signaling possible DAT selling.

Featured metric: Aave v3 Correlated Leverage shows where correlated collateral and borrows concentrate.

Note: Rapid shifts in available liquidity can push markets past interest‑rate kinks, amplifying rate moves.

Risk Pulse and Radar Highlights

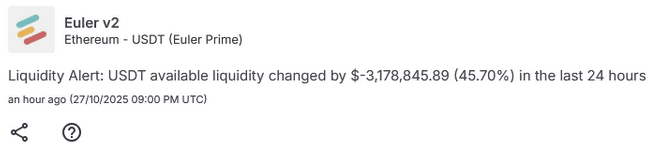

Source: Euler v2 Pulse

A ~$4M whale withdrawal on Euler caused the drop in available liquidity.

With just under $3M remaining, further large flows could push the IRM above its kink, steepening borrow costs.

Source: Spark Pulse

Heavy borrowing against wstETH / weETH collateral reduced USDT liquidity on Spark by ~45%

Utilization climbed to ~90%, lifting the borrow rate by ~50 bps.

Current IRM kink for the market is at 95% utilization.

Current Event Risks

Negative-Carry sUSDe Loops

Lower funding rates, post the October 10 flash crash, have cut yields for basis‑trade strategies. On Aave v3 Core, USDT/USDC borrow rates sit ~2.0% / ~1.5% above the sUSDe yield, turning the carry negative for users borrowing stables to lever sUSDe.

Source: Aave Risk Radar

As the spread stays below zero, looped positions that rely on borrowing stables to buy sUSDe begin to bleed.

Source: Aave Risk Radar

Why it matters

Scale: Roughly $1B of positions are exposed in Aave v3 core alone.

Systemic unwind risk: Negative carry → collateral sales or deleveraging → thinner liquidity in the same venues providing the leverage.

What to watch

Spread gating: Aave borrow APY minus sUSDe yield staying < 0.

Utilization jumps: Especially in USDT markets where hitting the kink spikes rates.

Liquidation bands: Rising share of looped accounts within 5% of liquidation.

ETH DATs start Selling

Source: Defillama

ETHZilla DAT announced a $40M share buyback funded by selling ETH. Although the fund holds only ~0.085% of ETH supply, this may signal pressure on smaller DATs:

Flat ETH prices limit the ability to lever holdings for new ETH purchases, while public‑company overhead remains.

If more DATs sell, additional spot sell pressure could spill into DeFi, especially strategies reliant on funding‑rate based yields.

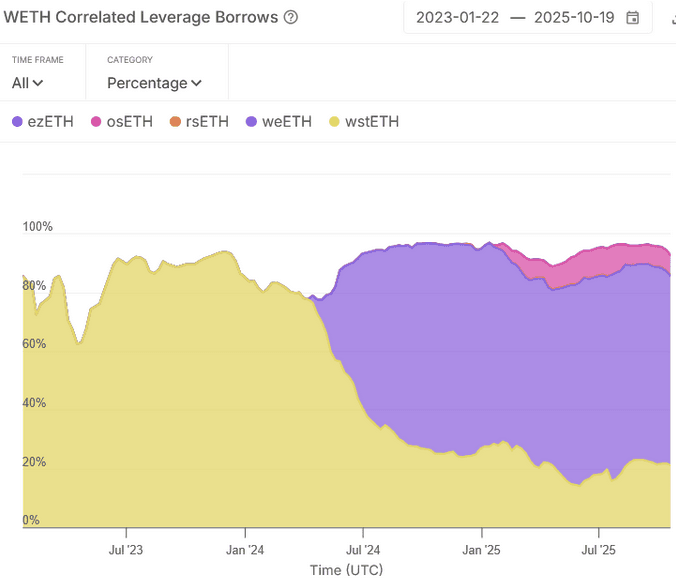

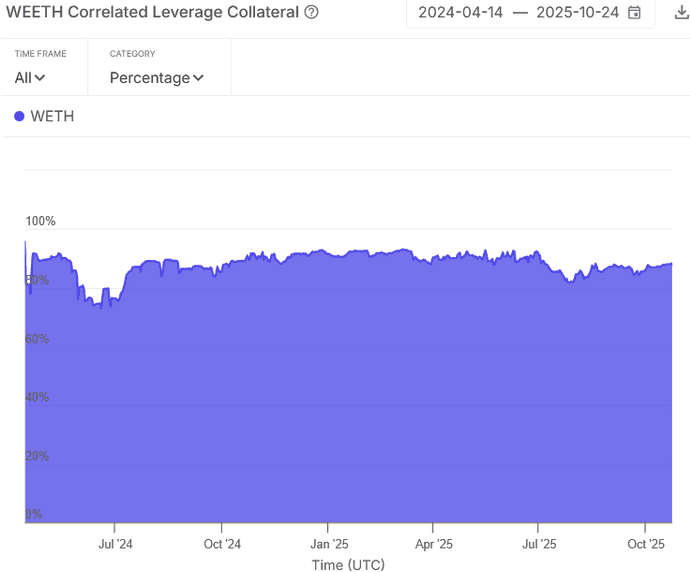

Feature Metrics: Aave v3 Correlated Leverage

Sentora’s new metric tracks both collateral and borrows to surface where leverage is concentrated across correlated assets (e.g., LSTs/LRTs with WETH).

Source: Aave Risk Radar

Source: Aave Risk Radar

What the charts show

A large share of WETH borrows on Aave is used by LSTs/LRTs to loop for higher yields.

Almost 90% of weETH collateral backs WETH borrows, reinforcing the loop.

Why it matters

If WETH borrow rates spike or exit queues for unstaking ETH lengthen, loop strategies can flip to negative carry and face forced de‑risking.

Stay informed, manage risks wisely, and stay liquid

Disclaimer: This newsletter is for informational purposes only and should not be considered financial advice.