TL;DR

· Flows steady the tape: US spot BTC ETFs flipped back to net inflows, helping stabilize BTC/ETH after the Oct 10 drawdown.

· Policy unlock: Hong Kong approved the first Solana spot ETF, creating a regulated APAC on-ramp for SOL exposure.

· DeFi ↔ TradFi bridge: Aave will onboard Maple’s institutional yield assets; an AAVE programmatic buyback is on the table.

· On-chain state: TVL pulled back, but stablecoin supply keeps grinding higher, underpinning liquidity and basis trades.

· Next week to watch: Day-one SOL ETF creations/redemptions, sentiment on AAVE’s buyback ARFC, and whether ETF inflows string together multi-session momentum.

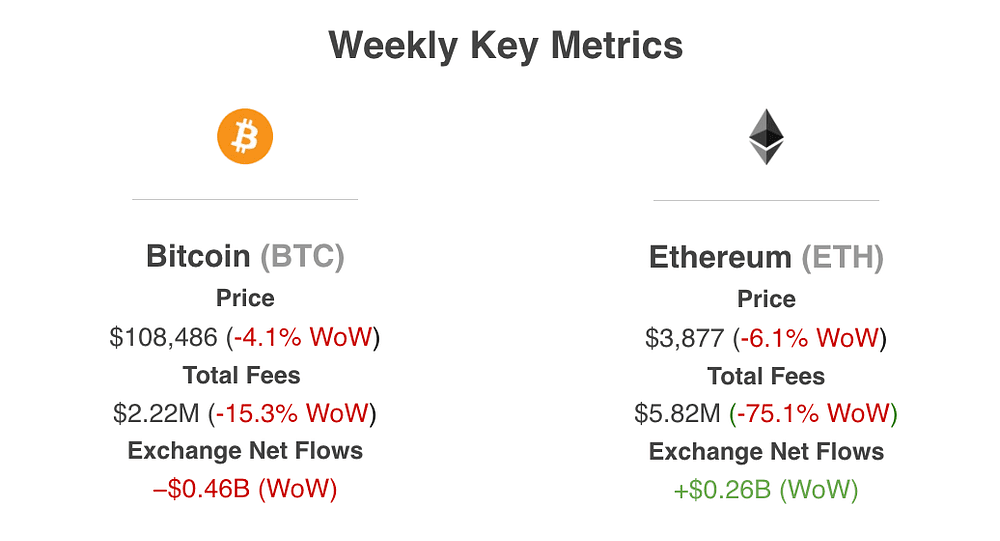

Weekly Key Metrics

Network Fees

Bitcoin: ~$2.22M (−60.5% w/w; the post-cascade spike faded and activity cooled, still muted vs. pre-halving peaks).

Ethereum L1: ~$5.82M (−75.1% w/w; traffic leaned back to L2s and L1 congestion eased).

Exchange Netflows (negative = outflows)

BTC: ≈ −$0.46B (ongoing exchange balance drawdown; outflow magnitude much smaller than last week’s ~−$3.7B).

ETH: ≈ +$0.26B (a mild net inflow after last week’s outflow; reflects some inventory rotating back onto exchanges).

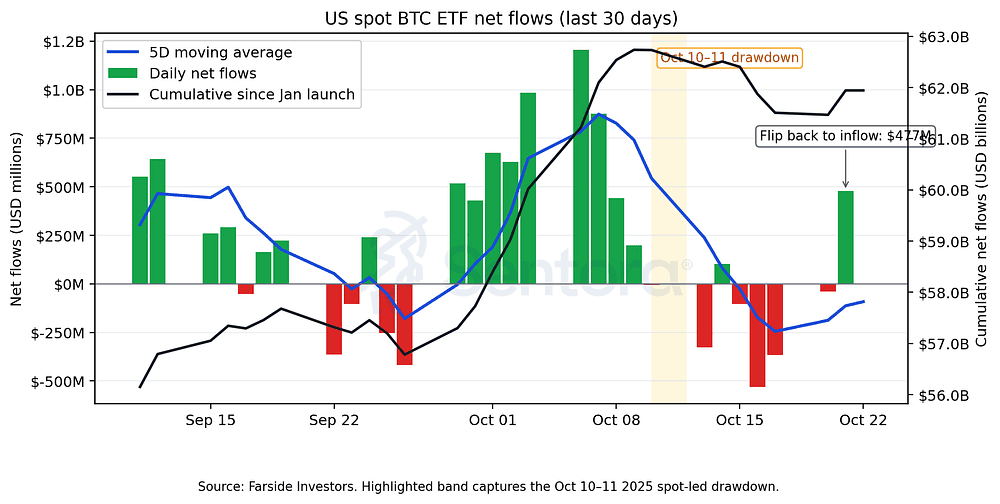

1) Market: flows stabilize the tape

US spot BTC ETF netflows

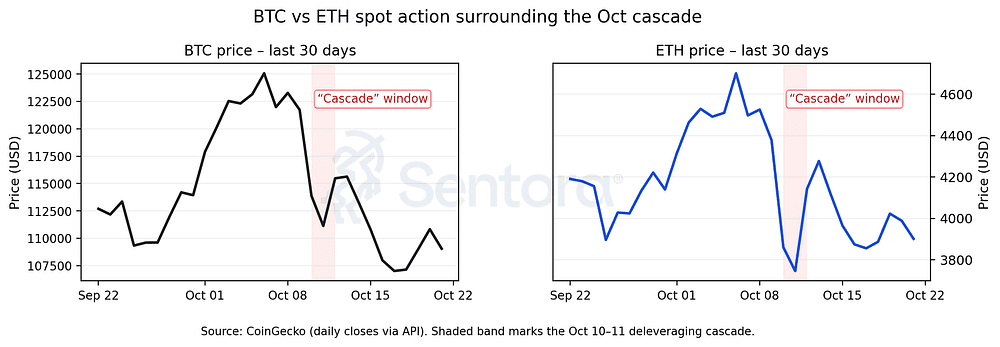

BTC vs. ETH Spot Price — Last 30 Days

After the Oct 10 liquidation cascade, BTC and ETH are ranging near $108k and $3.8k. The tone improved Monday as US spot BTC ETFs flipped back to +$477M net inflows, helping defend the range. Still, global ETP flows last week were –$513M as US products saw redemptions, while ETH, SOL drew non-US dip-buyers. The takeaway: flows are fragile but responsive, and ETF demand remains a key shock-absorber.

Microstructure watch: The Oct 10 move exposed thin resting depth across majors — order books “appeared empty” for minutes on top BTC venues — so near-term slippage risk remains elevated until liquidity rebuilds.

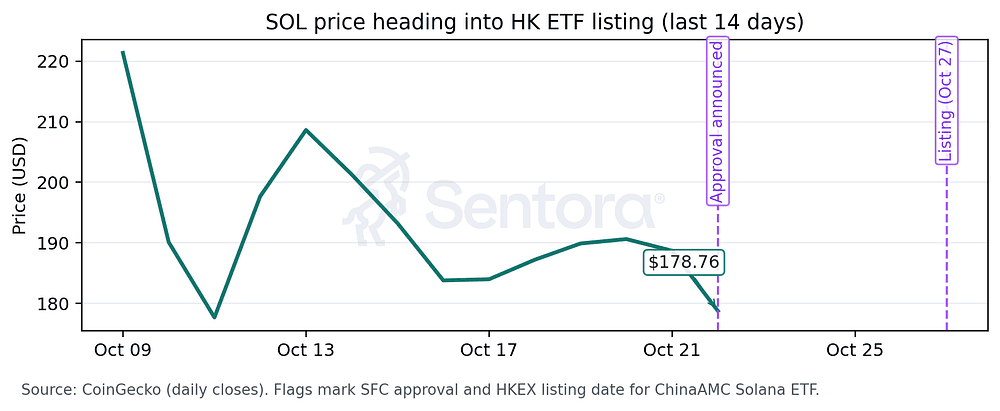

2) Policy & institutions: Hong Kong approves the first Solana spot ETF

SOL Price Around Hong Kong ETF Approval

Hong Kong’s SFC approved ChinaAMC’s Solana ETF (03460), set to list on Oct 27 with HKD/RMB/USD counters. It’s the city’s third spot crypto ETF after BTC/ETH and the first SOL spot vehicle globally — a notable unlock for institutional SOL exposure in APAC.

Why it matters: After a fortnight of risk-off, a new, regulated on-ramp for SOL arrives right as perp activity migrates on-chain. Watch secondary-market liquidity and primary creations in week one for a read on real demand.

3) DeFi crossover: Aave ↔ Maple and an AAVE buyback push

Aave x Maple

Aave will onboard Maple’s institutional yield assets (starting with syrupUSDT/USDC) across Plasma and Core markets, introducing a new class of collateral sourced from Maple’s credit pools. The goal: stabilize borrow demand and deepen liquidity with institutional capital.

AAVE buyback proposal

An ARFC live on Aave governance proposes enshrining a $50M/year program, executed weekly ($250k–$1.75M), funded by protocol revenue. It would formalize and extend the 2025 buyback pilot into a permanent Aavenomics pillar.

Why it matters:

Yield-bearing stables convert idle balances into yield, concentrating demand and reducing the stop-start pattern in stablecoin borrowing.

A programmatic buyback tightens the link between fee generation and tokenholder value — expect governance and revenue disclosures to be price-sensitive catalysts.

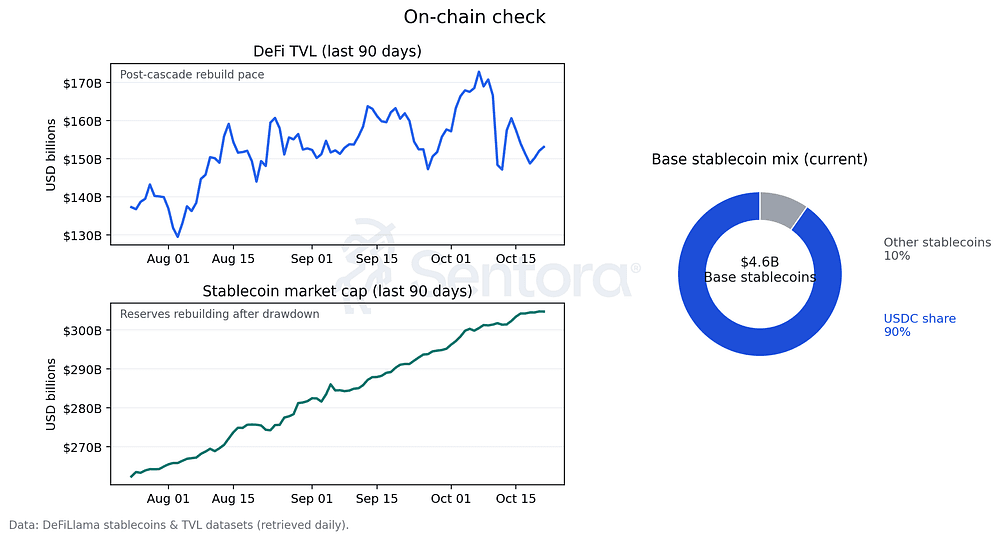

4) On-chain check: TVL, fees, stablecoins

On-Chain Check: DeFi TVL & Stablecoin Market Cap (90D) + Base Stablecoin Mix (Current)

TVL sits near $131B after the drawdown; rotation into safer collateral and RWAs continues to be a theme.

Stablecoins hit ~$308B cap, grinding higher even through volatility — key fuel for perps, basis trades, and cross-chain mobility. On Base, stablecoin cap holds ~$4.57B with USDC dominance >90%.

What to watch next week

Oct 27: ChinaAMC SOL ETF first trading day — creations/redemptions and day-one spreads.

Aave governance: community temperature on the $50M/year buyback ARFC; follow-on specs for execution and reporting.

ETF flows: Does Monday’s +$477M in US spot BTC ETFs mark an inflection back to multi-day net inflows?