What the market‑wide data shows

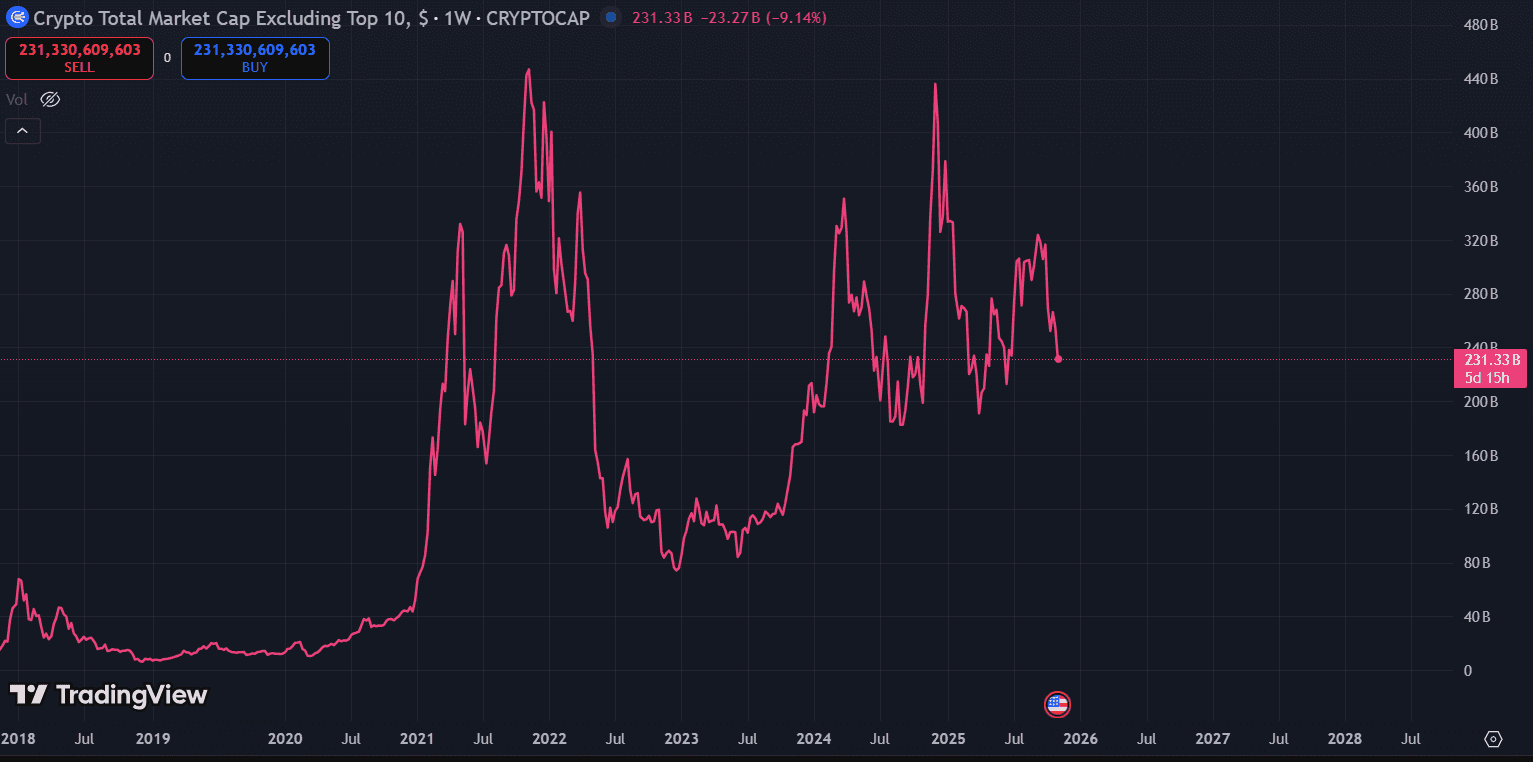

Altcoins have retraced sharply compared with prior peaks. The total altcoin market cap, excluding top 10 assets, is nearly 50 percent below the previous cycle’s highs. This move has played out alongside softer participation metrics and heavier rotation into Bitcoin.

Figure 1. Total crypto market cap ex top 10, weekly. 2018 to 2026. TradingView

In past cycles, sustained declines in market cap coincided with lower user intensity on chain and tighter macro risk environments. When liquidity tightens, marginal capital shifts to BTC first, leaving long‑tail assets more volatile on the way down and slower to recover.

Without a rebound in user and transaction breadth, altcoin beta tends to underperform and dispersion increases. That environment rewards selectivity over broad exposure.

Ethereum: activity has cooled after a long uptrend

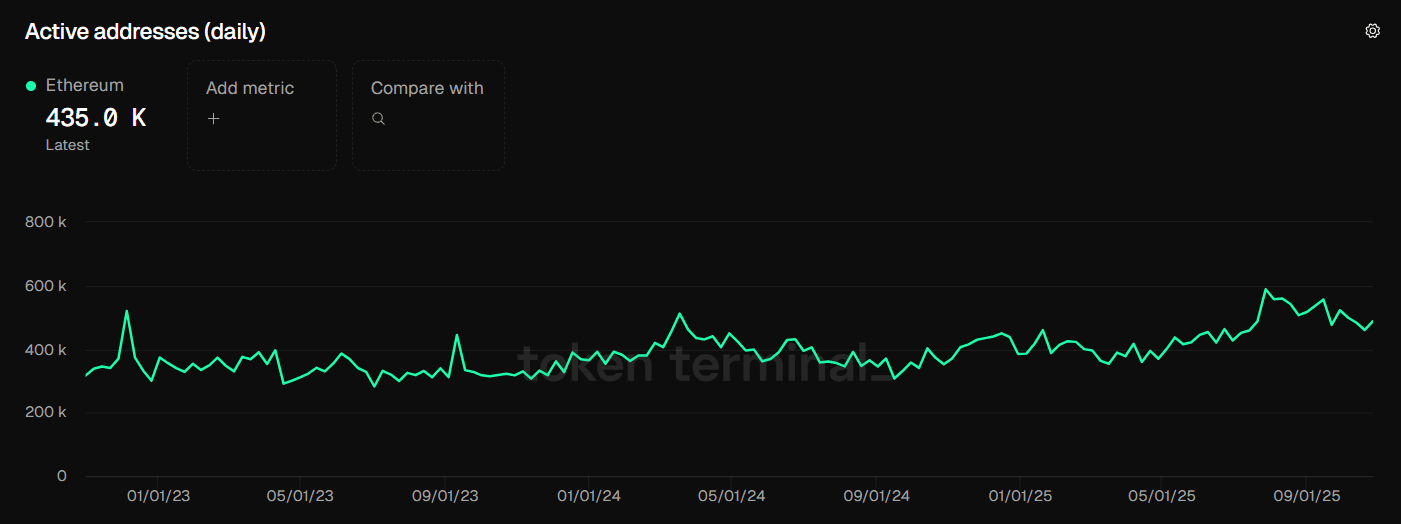

Ethereum activity provides a good indicator for broader altcoin trends, as it is the main hub for much of the altcoin space, alongside a few other major networks like Solana or Ethereum L2s like Base.

Daily active addresses on Ethereum fell roughly 17 percent from about 589 thousand in late July to about 488 thousand by late October. This decrease marks the first multi-month decrease after a longer-term uptrend, and it mirrors the soft patches observed during prior bear phases.

Figure 2. Ethereum daily active addresses. TokenTerminal

Fewer addresses interacting with contracts reduces fee pressure and the pace of new cohort formation. Builders still ship, but user acquisition becomes harder and incentives must work longer to achieve the same lift.

DeFi TVL: sliding, yet relatively resilient

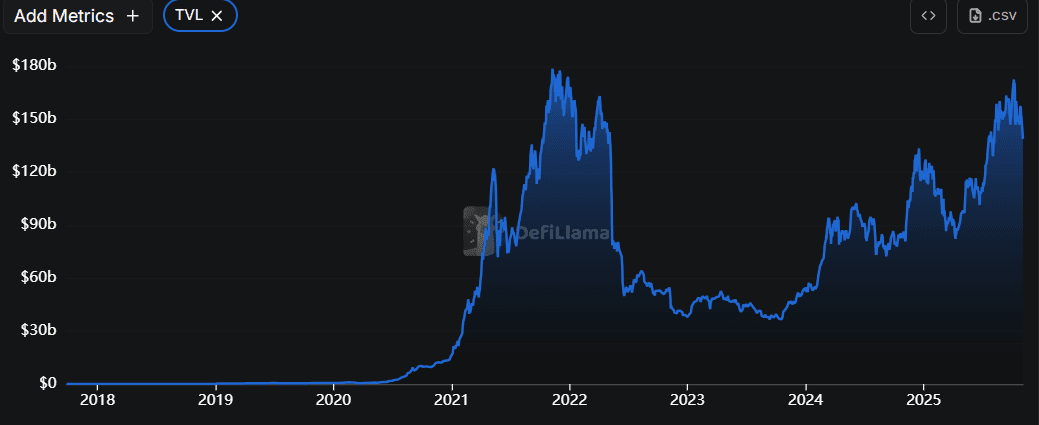

DeFi total value locked has started to trend down, although it remains comparatively firm versus other crypto activity metrics.

Figure 3. DeFi TVL since 2018. DeFiLlama

Institutional participation has been a stabilizer. Larger allocators use non‑custodial workflows and risk controls to maintain market‑neutral or collateral‑driven positions even as speculative activity fades. Composition also matters: TVL reflects asset prices and stablecoin flows, which can mask churn underneath the headline.

TVL alone is not a growth signal. Pair it with net new wallets, transaction counts, and lending/DEX activity to understand whether liquidity is productive or simply parked.

Solana: the out‑performer is cooling

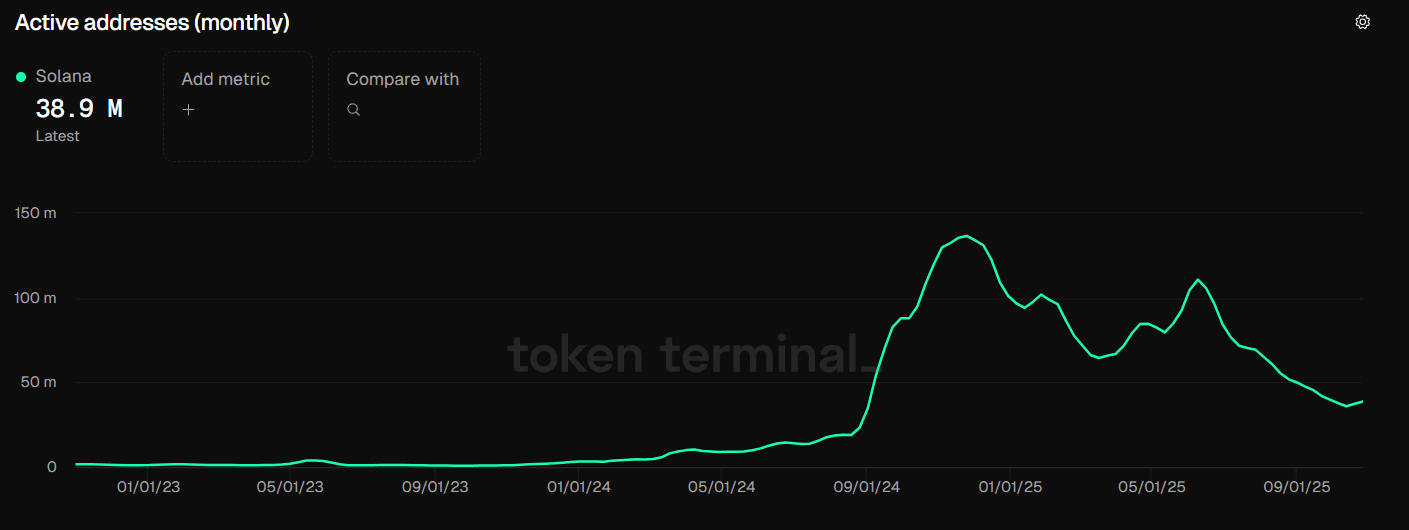

Solana out‑performed through much of the year, yet momentum eased. Monthly active addresses declined roughly 30 percent in Q3 2025 amid the broader slowdown.

Figure 4. Solana monthly active addresses. Token Terminal

High‑velocity segments such as memecoins and NFT trading have significantly implifiedflows on Solana. As those segments cool, address churn drops and activity concentrates in fewer power users.

While Solana has clearly entered a cooldown phase, the network has historically been incredibly efficient at attracting retail attention, and it would be the key network to watch for a potential reversal. Especially hype around new Solana projects could be a crucial indicator for renewed retail interest.

Memecoins: the sharpest drawdown

Memecoin market cap is down more than 60 percent from 2024 peaks, and on‑chain activity reflects the air‑pocket. For example, Dogecoin activity has slipped and active addresses for PEPE have fallen by about 85 percent. Hype‑to‑bust cycles have historically been abrupt as speculative cohorts exit at once.

Figure 5. Aggregate memecoin market cap since 2021. CoinMarketCap

Treat memecoins as momentum‑driven collateral for risk cycles, not as structural sources of user adoption. When liquidity returns, these tokens can rebound quickly, but breadth usually lags fundamentals‑led segments.

Are we already in an altcoin winter?

Short answer: Conditions rhyme with early winter. The data suggests we are six or more months into a slowdown. Historically, altcoin winters last 1 to 3 years, although micro‑rallies occur as new narratives introduce temporary demand.

What would change the call:

Persistent growth in new addresses and active addresses across multiple L1s and L2s.

Growth on retail-driven L1s like Solana or hype for new retail-focused Dapps.

Rising transaction counts with stable or improving fees, indicating organic usage

Higher DEX and CEX volumes can indicate increased demand, especially if this coincides with increasing TVL and altcoin prices.

A wave of new project launches that retain users beyond the first incentive epoch.

Until several of these conditions line up for multiple months, caution is warranted.

Bitcoin’s relative strength and the decoupling question

Bitcoin holding above $100,000has coincided with weaker breadth across altcoins. This decoupling is an indication of the new demand for Bitcoin coming from traditional finance. While this cohort has shown significant interest in Bitcoin, they are not as interested in altcoins.

This trend will fundamentally shift the relationship between bitcoin price movement and that of altcoins. Until retail shows interest in participating more broadly in the altcoin market, it is unlikely that altcoins will significantly outperform Bitcoin.

Bottom line

Evidence is stacking up that we are in the cooling phase of the cycle. Selectivity, risk controls, and disciplined monitoring matter more now than broad altcoin beta. If and when the data inflects, opportunities tend to appear first in altcoins with real utility and that are capable of driving real retail demand.