TL;DR

Risk-off returned: U.S. spot BTC/ETH ETFs saw ~$0.8B combined outflows on Nov 4, led by Fidelity’s FBTC; SOL-focused funds bucked the trend with inflows.

Macro backdrop: The Fed cut 25 bps on Oct 29 (to 3.75%–4.00%) after the September cut; funding conditions remain in focus post-cut.

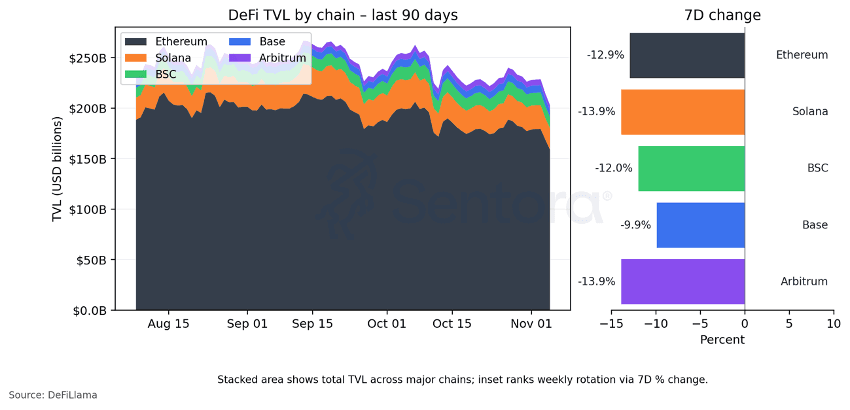

Market action: BTC briefly broke below $100k on Nov 4 before bouncing; DeFi TVL fell ~6–7% 24h at midweek, with most majors retracing.

Flows & structure: Solana ETFs in Hong Kong (launched Oct 27) continued to gather assets while U.S. BTC/ETH products bled.

On-chain & tech: Ethereum’s Fusaka upgrade is slated for Dec 3; Linea’s Exponent token-burn mechanics went live Nov 4.

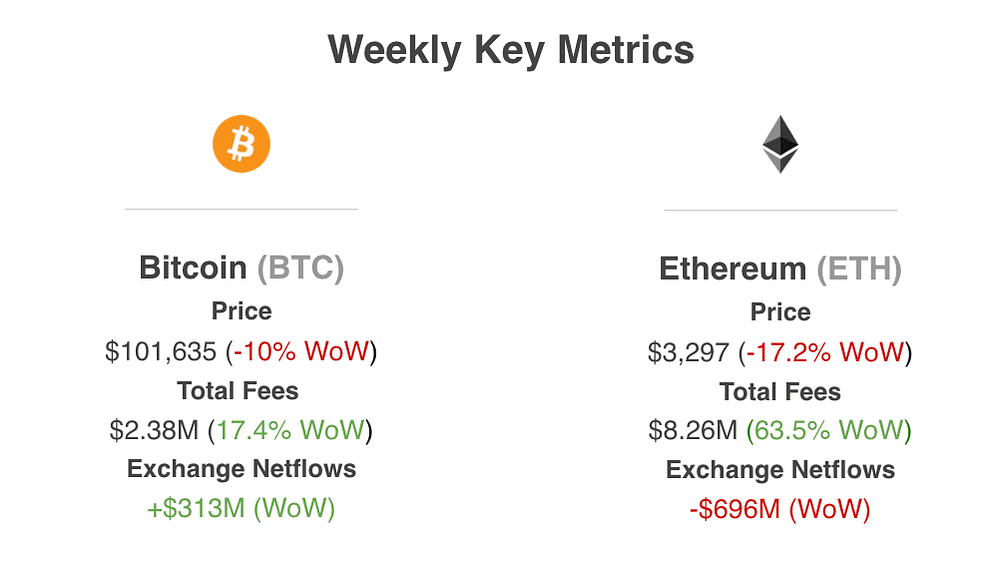

Weekly Key Metrics

Network Fees

· Bitcoin fees (~$2.38M, +17.4% w/w): A modest mempool fill after volatility — plus bursts of inscriptions/UTXO consolidations — pushed total fees up from a quiet base.

· Ethereum fees (~$8.26M, +63.5% w/w): Heavier L2 settlement batches and brief DEX/MEV flurries lifted L1 base fees sharply from last week’s lull.

Exchange netflows

· BTC exchange netflows (~+$313M inflows): More BTC moved onto exchanges for profit-taking, liquidity needs, and arb/collateral top-ups following price swings.

· ETH exchange netflows (~–$696M outflows): ETH kept leaving venues for staking, L2 bridging, and ETF/AP creations, pulling inventory into custody and reducing sellable float.

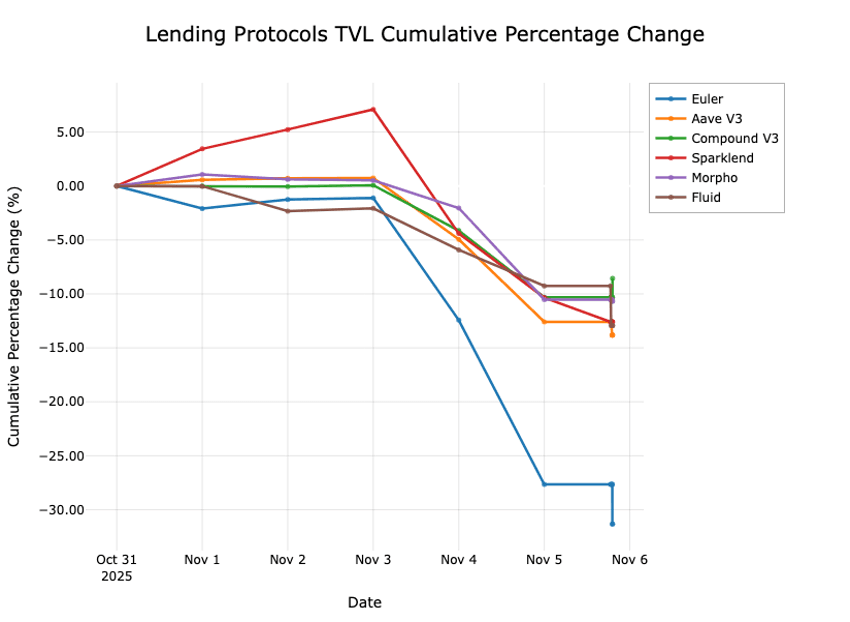

November DeFi liquidity crunch — catalysts and transmission

Cumulative percentage change of Lending Protocols TVL (Source: Defillama)

This week was characterized by a confluence of different DeFi Risk events.

Balancer exploit (~$128M): Precision-math bug on Balancer V2 eroded confidence in blue-chips; TVL plunged ~60% overnight and knock-on risks spread to forks (e.g., Beraswap/Beets), prompting emergency halts (incl. Berachain) and address freezes (Sonic). Impact is heaviest in ETH LST pools.

Stream Finance collapse (xUSD): Post-disclosure of ~$93M loss, withdrawals paused; xUSD depegged ~80% (to ~$0.17), seeding bad debt across lending markets that used xUSD as collateral and sparking broader DeFi risk-off.

Moonwell oracle malfunction: Chainlink pricing glitch for wrstETH enabled flash-loan abuse; >$1M drained on Base/Optimism — reminder that oracle surfaces remain a critical failure point even for “battle-tested” infra.

Elixir / deUSD squeeze: Concerns over Stream exposure led Gauntlet to pause several Compound Comets; deUSD/sdeUSD liquidity shrank and borrow rates spiked >20%+ across affected markets and Morpho vaults.

Leverage wipeouts rolling into spot DeFi: October’s large perp liquidations thinned order books; with the early-Nov drawdown, lending liquidations accelerated (Aave ~$100M in a day, near the Oct-10 peak).

User-level effects (why it mattered this week)

Higher slippage on DEXs: Liquidity retrenchment pushed wstETH/wETH swaps into higher price impact bands even at smaller trade sizes. Minor LST de-peg episodes appeared as users rotated to base assets.

Withdrawal freezes via utilization spikes: Ring-fenced vaults (e.g., certain Euler/Morpho markets) hit ~100% utilization temporarily — locking lenders until utilization normalized; several USDC markets showed transient 30–60%+ borrow rates. Most have eased since.

Macro & Liquidity

The FOMC followed up September’s “risk-management” cut with another 25 bps on Oct 29, taking the target to 3.75%–4.00% and signaling focus on labor-market softness. Regional Fed commentary this week reiterated that stance.

Treasury’s Quarterly Refunding materials (Nov 5) kept attention on term premium and balance-sheet dynamics — relevant for crypto via liquidity and risk appetite.

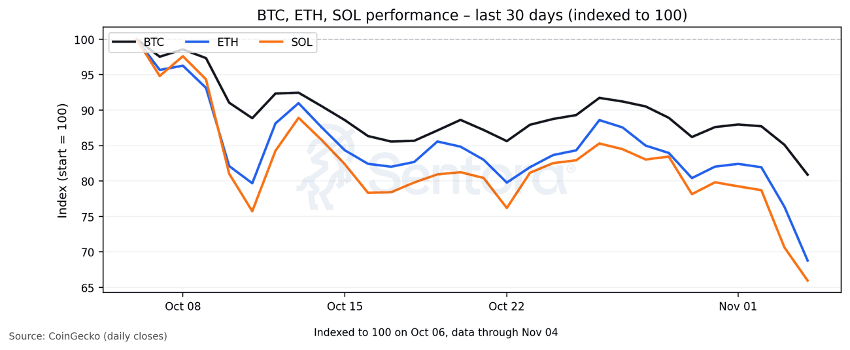

Price & Positioning

BTC dipped sub-$100k on Nov 4 amid broad crypto drawdowns before rebounding; intraday ranges remain wide.

ETH tracked lower alongside BTC; dispersion widened in L1s/L2s as beta unwound.

Dispersion widened in L1s/L2s as beta unwound, with DeFi-specific shocks (Balancer, xUSD) amplifying on-chain basis stress and widening slippage in LST pairs.

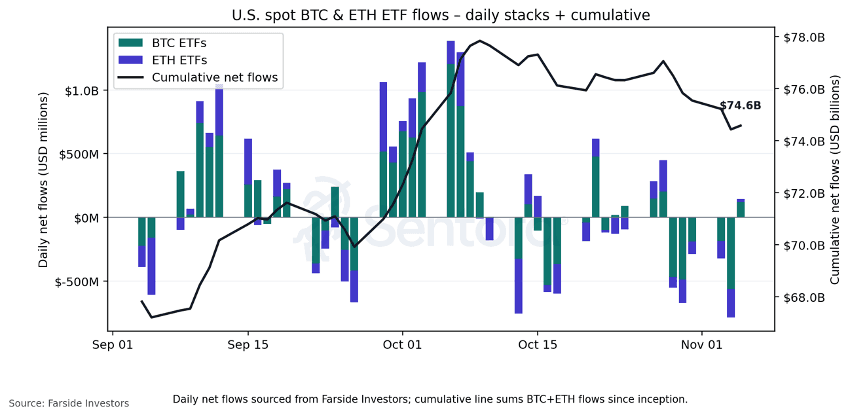

ETF & Fund Flows

Spot BTC ETFs (U.S.) logged -$529M net outflow on Tue, Nov 4, the fifth straight day of redemptions, bringing the cumulative five-day bleed to ~$1.9B.

Spot ETH ETFs (U.S.) saw −$219M outflows on Nov 4; BlackRock ETHA led the redemptions (−$111M).

Combined BTC+ETH outflow approached $0.8B on Nov 4, while SOL ETFs recorded net inflows—divergence that persisted through mid-week.

Context: October still finished strong for BTC ETFs (~$3.4B net inflows late month), underscoring how quickly flows can flip with macro.

Flow fragility coincided with a DeFi liquidity crunch, where protocol-level shocks tightened on-chain liquidity and likely fed into short-horizon risk-off across venues.

DeFi & On-Chain

TVL retraced: Headline DeFi TVL ~−6.5% over 24h at midweek; on a 7-day basis, Ethereum TVL −12%, Solana −11%, BSC −11% (price-led).

Institutional credit meets DeFi: Aave × Maple integration (Oct 21) continues to be a structural positive — bringing yield-bearing, institution-backed assets (e.g., syrupUSDT/USDC) into Aave markets. Near-term price impact on AAVE muted, but the pipeline matters for on-chain credit depth.

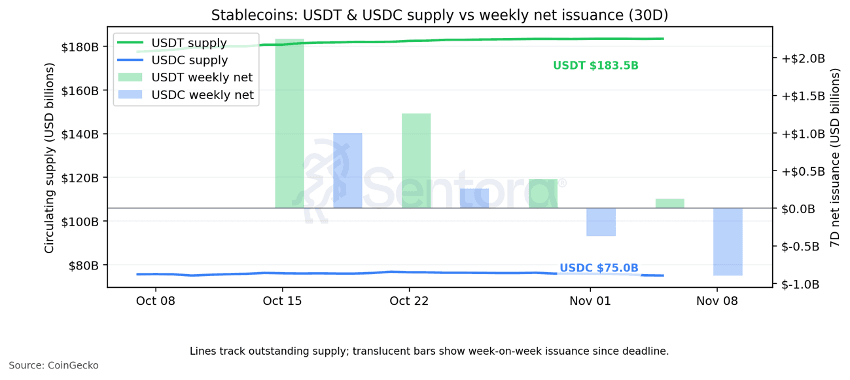

Stablecoin activity: Recent data highlight USDC’s higher velocity vs. USDT on Ethereum, a sign of changing payment/settlement patterns.

Derivatives & Microstructure

On-chain perps remain a bright spot: Hyperliquid saw strong engagement around its newer product sets (incl. equity perps), though liquidity fragmentation is a watch item.

HYPE (Hyperliquid’s token) rebounded 8–14% mid-week despite broad risk-off, reflecting derivatives-venue beta. Handle with caution, given the thin liquidity.

Knock-through to perps: As DEX liquidity thinned and borrowing costs jumped in pockets of DeFi, basis trades were harder to maintain; liquidation risk migrated from perps to spot-credit venues, then partially reversed as utilization normalized.

Protocol & Tech Updates

Ethereum: Core devs confirmed the “Fusaka” upgrade for Dec 3, keeping the year-end roadmap intact. Expect gas/throughput changes to drive renewed infra narratives if the date holds.

Linea: Exponent went live on Nov 4 — each tx now burns 20% in ETH + 80% in LINEA, introducing a dual-burn model to the L2’s tokenomics.

ETFs ex-U.S.: Hong Kong listed the first spot SOL ETF on Oct 27, broadening regulated access beyond BTC/ETH in Asia.

What To Watch Next

1. DeFi contagion map: Track remediation at Balancer/forks, Stream unwind paths, and oracle patch status; watch for secondary effects in LST liquidity and stable pools.

2. Utilization/borrow-rate normalization: Euler/Morpho/Compound vaults where utilization spiked — confirm sustained liquidity return and borrow rates drifting to baseline.

3. Liquidation overhang: Monitor large, potentially liquidatable loans that could pressure collateral prices on DEXs if unwound into thin liquidity.

4. Flows vs. pipes: Whether U.S. ETF outflows stabilize and whether stablecoin issuance re-accelerates — key for risk appetite into mid-November.

5. Macro catalysts: Same Fed/liquidity lens as prior section; any tightening in dollar liquidity would compound DeFi’s healing process.